Pre-approvals for Home Buyers

Walking into a Sunday open home without a pre-approval is like trying to win an auction with your hands tied behind your back. You find the perfect place, but the fear of missing out hangs over you because you aren’t completely sure the bank will back your offer. Between confusing jargon and the Debt-to-Income (DTI) limits of six times your income for owner-occupiers, the process of obtaining pre-approvals can feel like a massive hurdle. You might worry your deposit isn’t quite enough or that a small credit blip will stop you in your tracks.

We know you want more than just a letter; you want the confidence to shop in a price range that is realistic for your future. This article will show you exactly how to secure a mortgage pre-approval so you can house hunt with confidence and make offers that win. Mortgage Suite Ltd will walk you through the steps to get a clear “yes” from a lender, explain why these approvals typically last for 60 to 90 days, and show you how to feel like a serious buyer that real estate agents want to work with.

Key Takeaways

- Understand why a pre-approval is your most powerful tool for being taken seriously by real estate agents and sellers in a competitive market.

- Learn the practical steps for obtaining pre-approvals, including how to organise your deposit and the paperwork lenders actually want to see.

- Discover how alternative lenders can offer a path forward if your financial situation doesn’t fit the standard bank criteria.

- Find out how to get the final “thumbs up” from your lender before you bid at an auction so you can sign a contract with total peace of mind.

- See how expert guidance can take the stress out of the process by handling the heavy lifting and negotiations with banks on your behalf.

What is a Mortgage Pre-Approval and Why Does it Matter?

If you have spent any time scrolling through property listings, you have probably seen the term pre-approval pop up. Essentially, it is a lender’s way of giving you a green light for a specific loan amount before you actually find the house you want to buy. This approval in principle means a bank or lender has looked at your finances and agreed to lend you a certain sum, provided the property you eventually pick meets their standards. Understanding What is a mortgage pre-approval? is the first step toward moving from a casual observer to a serious contender in the market.

The process of obtaining pre-approvals is about more than just paperwork; it is about strategy. When you are obtaining pre-approvals, you are building a bridge between your savings and your new front door. Having this sorted early offers several distinct advantages:

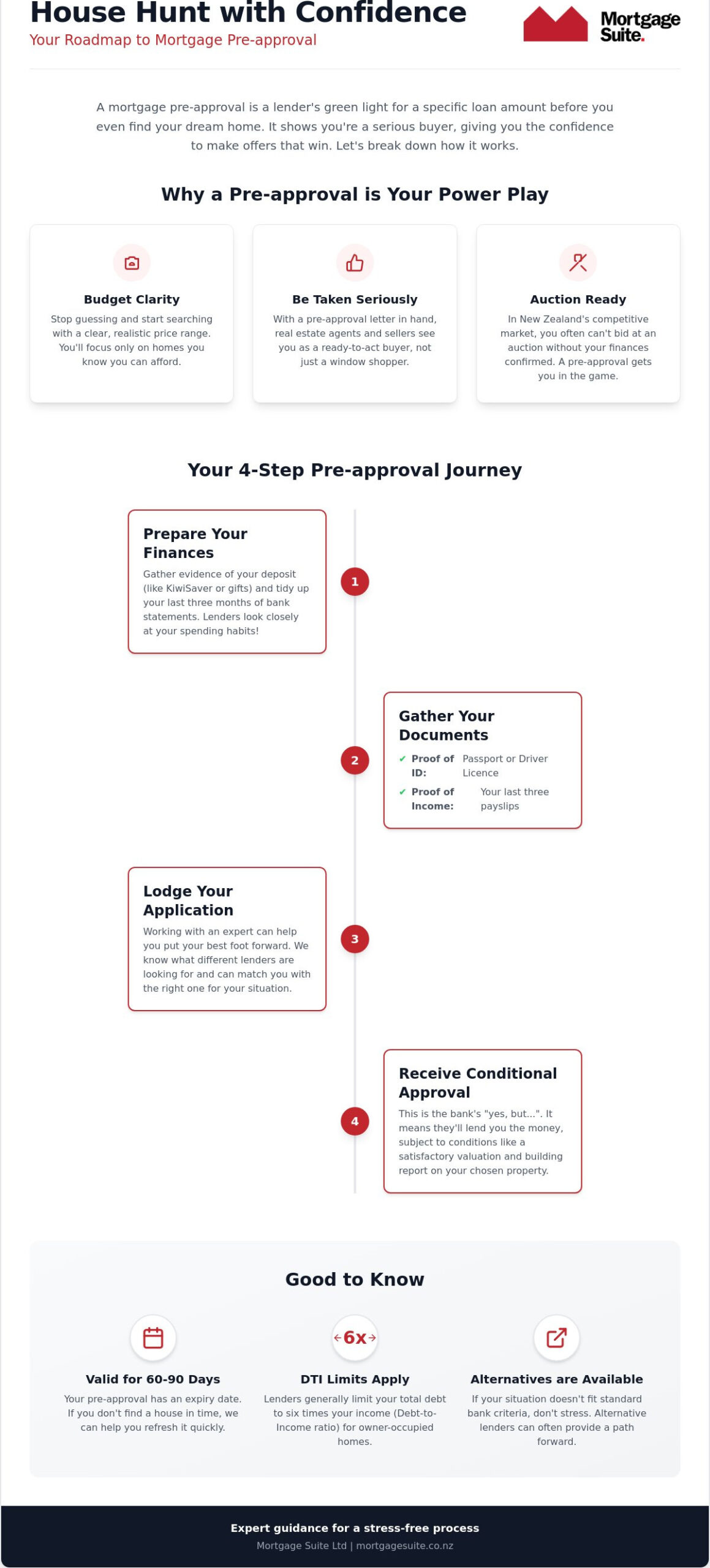

- Budget Clarity: You stop wasting time on million-dollar homes if your limit is $800,000. It keeps your search focused and realistic.

- Agent Credibility: Real estate agents take you far more seriously when you have a letter from a lender. It shows you are ready to act.

- Auction Readiness: As we mentioned, auctions are a common way to sell in New Zealand. You usually cannot bid without having your finance already confirmed.

Think of it as a tool that levels the playing field. It removes the guesswork and allows you to walk into an open home knowing exactly what you can offer. This confidence is infectious; it makes sellers more likely to consider your bid over someone who still needs to talk to their bank.

The Difference Between Conditional and Unconditional Approval

It’s a common mistake to think a pre-approval is a blank cheque for any property you fancy. Most of the time, the bank gives you a conditional approval. This means they are happy to lend to you, but they still need to sign off on the specific house. Common conditions might include a registered valuation to ensure the price is fair, or a clean building report to check for structural issues. Conditional approval is the starting point of your journey, not the finish line.

How Long Does a Pre-Approval Last?

Standard validity is usually 60 to 90 days in the current NZ market. While we touched on this briefly, it’s important to understand why this window exists. Lenders need to ensure your financial situation hasn’t shifted significantly, especially with fluctuating interest rates. If your pre-approval expires before you find a home, Mortgage Suite Ltd can often refresh your application without starting from scratch. This usually involves providing updated payslips to confirm your income is still steady, allowing you to keep hunting without a long delay.

A Step-by-Step Guide to Obtaining Pre-Approvals in NZ

Getting your ducks in a row before you visit an open home is easily the smartest move you can make. The process of obtaining pre-approvals is a bit like preparing for a high-stakes job interview; you want to present the best possible version of your financial life to the lender. It starts with your deposit. Whether you are using KiwiSaver, a First Home Grant, or gifted funds from family, you will need clear, documented evidence of where that money is sitting and how it was built up.

Lenders do not just look at what you earn; they look closely at how you spend. When you are in the middle of obtaining pre-approvals, expect the bank to go through your last three months of bank statements with a fine-tooth comb. They are looking for your true expenses, which includes everything from your gym membership and Netflix subscription to how often you are hitting the local cafe. Cleaning up your discretionary spending a few months before you apply can make a massive difference to your borrowing power. If you are feeling overwhelmed by the paperwork, Mortgage Suite Ltd can help you navigate the home loan process from start to finish.

Once your numbers look tidy, it is time to submit your application. While you could walk into your local branch, working with an expert who knows the current lending criteria across multiple banks often yields a better result. We can help coordinate the application to ensure you are putting your best foot forward with the right lender for your specific situation.

The Essential Document Checklist for 2026

To keep things moving quickly, it is a good idea to have these items ready in a digital folder:

- Proof of identity: A current NZ Passport or NZ Driver Licence.

- Proof of income: Your last three payslips or full financial accounts if you are self-employed.

- Deposit evidence: A KiwiSaver summary or bank statements showing your genuine savings.

- Debt summary: Statements for credit cards, car loans, or any Buy Now Pay Later accounts.

Understanding the Lending Rules

Two main rules will largely dictate your success: your deposit-to-loan ratio and your borrowing limits based on income. The first is simply the size of your deposit compared to the house price. While a 20 per cent deposit is the standard “gold pass” for most banks, schemes like the First Home Loan only require 5 per cent. The second rule limits how much you can borrow based on your gross annual salary. As of July 2026, most people buying a home to live in are capped at a limit of six times their annual income. This means if your household earns $150,000, your total debt generally cannot exceed $900,000. These rules are strict at big banks, but some alternative lenders have more flexibility, which is why having conditional pre-approved finance is so vital before you start bidding.

When the Bank Says No: Obtaining Pre-Approvals via 2nd Tier Lenders

It is a sinking feeling when your own bank, the place where you have kept your savings for years, says no to your home loan application. Perhaps you are self-employed and your income fluctuates, or maybe your deposit is just shy of the standard requirements we discussed earlier. Whatever the reason, a “no” from a big bank does not have to be the end of your home-buying journey. For many Kiwis, obtaining pre-approvals through alternative or non-bank lenders is the key that finally opens the door.

These lenders often look at the bigger picture rather than just ticking boxes on a rigid checklist. While the mainstream banks are currently bound by very strict borrowing limits based on your income, alternative lenders frequently have more room to move. They specialise in finances that do not fit the usual boxes, providing a vital lifeline for people with unique money situations. The process of obtaining pre-approvals in this space is often faster because these lenders are designed to handle complexity and individual circumstances without the red tape.

Working with an alternative lender does not mean you are on your own. It simply means you are using a different path to reach the same goal. Mortgage Suite Ltd specialises in these situations, acting as a steady hand to guide you through the options that the big banks simply will not talk about.

Why Consider a Non-Bank Lender?

Choosing a non-bank lender is about finding a partner that understands your specific situation. They often have much more practical rules for self-employed home loans, looking at your business’s potential rather than just your latest tax returns. They can also be more lenient if you have a minor credit issue from the past or a slightly smaller deposit. If you are struggling to save the full amount, we can also check your eligibility for the First Home Loan scheme, which only requires a 5 per cent deposit. While interest rates might differ slightly from the big banks, these lenders provide a clear path to homeownership right now.

How a Broker Navigates Alternative Options

This is where experience really counts. Krish Krishna uses over 20 years of banking expertise to “pitch” your financial story to the right people. We do not just send off an application; we build a case for why you are a reliable borrower. We help you navigate the various 2nd tier lender New Zealand options to find a fit that makes sense for your long-term goals. Mortgage Suite Ltd ensures there are no surprises in the fine print and that you feel completely supported as you move toward a “yes”. We act as the bridge between the rigid world of institutional banking and your personal need to secure a home.

Using Your Pre-Approval: Auctions and Making Offers

Once you have finished the hard work of obtaining pre-approvals, it is tempting to think the finish line is in sight. You have your budget sorted and your letter in hand, but it is vital to remember that a pre-approval is not a blank cheque for any property on the market. While the lender has said “yes” to you as a borrower based on your income and savings, they still need to sign off on the specific house you want to buy. The bank needs to be certain that the property is a safe investment for the money they are lending you.

If you are looking at a private sale or a deadline sale, you still have a bit of a safety net. The effort you put into obtaining pre-approvals pays off here because it allows you to act quickly, but we still recommend making your offer “subject to finance.” This gives your lender a few days to review the specific house buying contract and confirm they are happy with the property’s condition and location. It also protects you if the bank has concerns about the house that weren’t obvious at the open home. If you are ready to start making moves on a property, talk to our team at Mortgage Suite Ltd to ensure your offer strategy is solid.

One common hurdle you might see in your pre-approval letter is a requirement for a “Registered Valuation.” This is where a professional valuer gives an independent opinion on what the house is actually worth. Lenders often ask for this if you have a smaller deposit or if the house is being sold at auction. If the valuation comes back lower than what you have offered, it can affect your deposit-to-loan ratio and potentially reduce the amount the bank is willing to lend. Sorting this early with the help of Mortgage Suite Ltd prevents a lot of stress on settlement day.

The Auction Strategy

Auctions are a different beast entirely because they are usually unconditional. When the hammer falls, the contract is final; there is no backing out to check your money. This means you must do all your homework before you even step into the auction room. First, ensure your pre-approval is still valid. Next, get your lawyer to check the ownership records and the house buying contract for any red flags. Finally, you must send the property details to your lender to get a specific “thumbs up” for that address. Without this, you are taking a massive financial risk.

Conditions You Might See on Your Letter

Your pre-approval letter will likely come with a list of tasks to complete before the money is released. These are requirements that must be met to turn that conditional offer into a firm one. Common conditions include:

- Building Report: A professional check to ensure the house is structurally sound and free from moisture or weather-tightness issues.

- Meth Test: Some lenders require this to ensure the property has not been contaminated by past illegal activity.

- House Insurance: You must have a certificate showing the house is fully insured from the day you take possession.

- KiwiSaver Withdrawal: Proof that your KiwiSaver first home withdrawal has been approved and the funds are ready to be paid to your lawyer.

How Mortgage Suite Simplifies the Pre-Approval Process

Let’s face it, the administrative side of buying a home is nobody’s idea of a fun weekend. At Mortgage Suite, we see our role as taking that weight off your shoulders. The process of obtaining pre-approvals shouldn’t involve you drowning in spreadsheets or staying up late trying to decode bank emails. We handle the heavy lifting with the lenders, acting as your dedicated advocate from the first phone call to the final sign-off.

Because we work across the whole market, we aren’t limited to just one bank’s set of rules. We look at mainstream options and alternative lenders side by side to see which one actually fits your life. Whether you are a first-home buyer trying to break into the market or a seasoned investor looking to grow a portfolio, we make sure you are positioned as a serious buyer in the eyes of the people holding the keys. Our goal is to ensure you walk into every open home with the confidence that your finance is ready to go.

Sometimes, the answer isn’t a “yes” right away. If you aren’t quite ready for obtaining pre-approvals yet, we don’t just send you on your way. We provide a clear, personalised plan to help you get there. This might mean looking at your spending habits or finding ways to tidy up your debts so that when you do apply, the lender sees exactly what they want to see. We believe in being a steady hand in a fluctuating market, helping you navigate every obstacle until you reach your goal.

Expertise You Can Trust

With over two decades of experience in the banking world, Krish Krishna knows how the system works from the inside out. This isn’t just about filling in forms; it’s about negotiation and having a seasoned expert in your corner. We understand how current mortgage rates NZ wide are shifting and how those changes impact your specific borrowing power. Most importantly, we talk like real people. We avoid the confusing jargon that makes the finance world feel inaccessible, focusing instead on clear, honest advice that helps you make better decisions.

Your Next Steps to Home Ownership

Getting started is easier than you might think. We usually begin with a simple, relaxed chat to understand what you are trying to achieve and what your timeline looks like. From there, we will help you gather the right information to build a successful application. We believe in partnership over transactions, meaning we are with you for the long haul, from the initial pre-approval through to the day you get your keys.

Ready to start? Get in touch with Mortgage Suite today and let’s get your home-buying journey moving with confidence.

Step Into the Property Market with Confidence

The journey to your new front door starts long before the first auction hammer falls. We have explored how obtaining pre-approvals gives you a clear budget and makes you a serious contender in the eyes of real estate agents. Whether you are navigating the strict DTI rules of the big banks or looking for the flexibility of a 2nd tier lender, having an expert in your corner ensures you don’t miss out on the perfect home just because the finance wasn’t ready.

Mortgage Suite brings over 20 years of banking experience to your side. We specialise in complex loans and alternative lending, offering a national service across New Zealand that prioritises your success. We handle the heavy lifting so you can focus on finding a place to call home. You deserve a partner who understands the nuances of the market and acts as your dedicated advocate.

Ready to take the first step? Book a free consultation with Mortgage Suite to start your pre-approval today. You don’t have to navigate this process alone; we are here to guide you toward a clear “yes” and help you move in sooner.

Frequently Asked Questions

How long does it take to get a mortgage pre-approval in NZ?

It usually takes between two and five working days to get an answer, depending on how busy the lender is. If your situation is a bit more complex, like being self-employed, it might take a little longer for the bank to work through your details. Having all your paperwork organised and ready to go from the start is the best way to speed up the process.

Does obtaining a pre-approval cost anything?

Most lenders and brokers don’t charge a fee for the initial application. It’s a service designed to help you understand your budget before you start shopping. You might, however, need to pay for things like a registered valuation or a building report once you find a house you love, as these are often conditions the bank requires before they give the final sign-off on the loan.

Can I get a pre-approval with a 10% deposit?

Yes, you can certainly apply with a 10 per cent deposit. While many main banks prefer a 20 per cent deposit to avoid extra fees or higher interest margins, there are plenty of options for those with less. You might look into the First Home Loan scheme or alternative lenders who specialise in helping people with smaller deposits get onto the property ladder without the usual bank hurdles.

What happens if the bank declines my pre-approval application?

Getting a “no” from one bank doesn’t mean you can’t buy a house. It often just means your specific financial profile didn’t fit that particular lender’s current rules or DTI limits. We often help clients by looking at 2nd tier lenders who have more flexible criteria for income or deposit sizes, turning a decline from a main bank into a clear path forward for your home ownership goals.

Do I need a lawyer before I get pre-approved?

You don’t need a lawyer to start the application, but it’s a very good idea to have one picked out early. You’ll definitely need them to look over the Sale and Purchase Agreement or the auction terms before you commit to a property. Having your legal team ready to go means you can move quickly and safely when you find a house that fits your pre-approved budget.

Can I change lenders after I have been pre-approved?

You aren’t locked into a specific lender just because they gave you a pre-approval letter. If market conditions change or another bank offers a better deal, you can definitely switch before you finalise the loan. We help you compare different offers to make sure you’re getting the best terms for your long-term goals, ensuring you don’t feel stuck with the first “yes” you receive.

Does a pre-approval affect my credit score?

A formal application for obtaining pre-approvals usually involves a credit check, which can have a small, temporary impact on your credit score. This is why it’s a good idea to work with a broker who can identify the right lender first. This approach prevents you from applying at several different banks yourself and creating multiple hits on your record, which can look bad to future lenders.

Is a pre-approval guarantee that I will get the loan?

No, a pre-approval isn’t a 100 per cent guarantee that the money will be paid out. It is an “approval in principle,” meaning the final loan depends on the property meeting the bank’s standards and your financial situation staying the same. Obtaining pre-approvals is the best way to show you’re a serious buyer, but the bank always gets the final say on the specific house you choose.