Borrowing Power Calculator NZ: How Much Can You Really Afford in 2026?

What if the number you see on a standard borrowing power calculator nz is actually underselling your potential to buy a home? It is completely normal to feel a bit anxious about your mortgage prospects right now, especially with the Reserve Bank’s Debt-to-Income (DTI) rules and the rising cost of living making every dollar feel smaller. You might even worry that a “no” from a big bank means your home-ownership dreams are on ice for good.

I understand how frustrating it is to feel like you are doing everything right but still coming up short. That is why this guide is designed to help you discover how to accurately estimate your mortgage potential and the practical steps you can take to boost your borrowing limit before you submit an application. We will explore how to navigate the current 2026 lending landscape, including the impact of the OCR sitting at 2.50 per cent and why looking beyond mainstream lenders might be the key to your success. By the end, you will have a clear path toward finding a loan that actually fits your unique financial situation and goals.

Key Takeaways

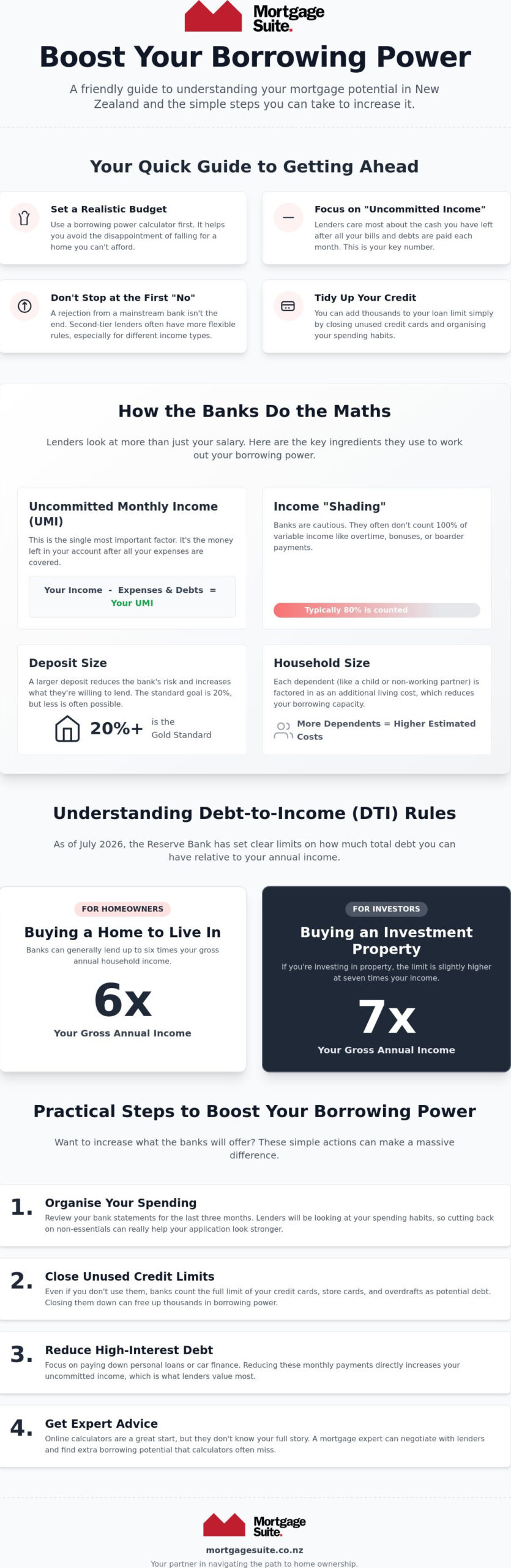

- Using a borrowing power calculator nz is the best way to set a realistic budget and avoid the heartbreak of falling in love with a home you cannot afford.

- Lenders focus heavily on your “uncommitted income,” which is the amount of cash you have left over every month after all your bills and debts are paid.

- A rejection from a mainstream bank does not mean your journey is over, as 2nd tier lenders often offer more flexible rules for different types of income.

- You can often increase your loan limit by thousands of dollars just by closing unused credit cards and organising your spending three months before you apply.

- While online tools provide a great starting point, a mortgage expert can often find extra borrowing potential through direct negotiation with lenders.

What is a Borrowing Power Calculator and Why Should You Use One?

A borrowing power calculator nz is essentially a digital health check for your finances. It takes a look at your income, your regular bills, and any debts you currently have to give you a rough idea of what a bank might be willing to lend you. Think of it as a helpful warm-up before you start the actual race of buying a home. Before you dive into the details, it helps to understand the basics of What is a mortgage and how these loans function as a long-term commitment. Using a tool like this early in the piece allows you to identify any spending habits that might look like red flags to a bank, such as high credit card limits or too many small “buy now, pay later” debts.

The main reason to use a calculator is to set a realistic budget for your property search. There is nothing more heartbreaking than falling in love with a beautiful home, only to find out later that your bank won’t even consider lending you that much. By getting an estimate first, you can narrow your search to houses you can actually afford. Fundamentally, your borrowing power is the balance between your gross income and your ability to service a loan comfortably. It is a measurement of how much breathing room you have in your budget after the mortgage is paid.

The Difference Between Borrowing Power and Affordability

It is vital to remember that there is a big difference between what a bank could give you and what you should take. Borrowing power is the maximum limit a lender sets based on their internal rules. Affordability, on the other hand, is about your daily life. Can you still afford a holiday, a new car, or even just the weekly grocery shop if you take that maximum loan? You should never aim for the absolute ceiling the calculator shows. Lenders also use interest rate “stress tests,” calculating your repayments at a much higher rate than the current market to ensure you can handle future changes without stress.

Why 2026 is a Unique Year for NZ Borrowers

This year has brought some specific challenges and opportunities for Kiwis. With the Official Cash Rate (OCR) sitting at 2.50 per cent as of July 2026, mortgage rates have shifted, directly impacting how much you can borrow. Before you start crunching numbers, take a look at the current Mortgage Rates NZ to see where the market stands. We are also seeing the full effect of Debt-to-Income (DTI) rules, which limit your total debt based on your yearly earnings. These changes mean the goalposts have shifted, making it more important than ever to have an accurate picture of your financial standing before you apply.

How the Math Works: The Key Factors Lenders Look At

Lenders don’t just look at your total salary and call it a day. They are far more interested in what we call “uncommitted income.” This is the actual cash you have left over once every single bill, grocery shop, and debt repayment is settled. When you play around with a borrowing power calculator nz, it tries to mirror this logic, but banks add their own layers of caution. For example, lenders often “shade” certain types of income, such as boarder payments or overtime, by typically counting only 80 per cent of the total to stay on the safe side. This buffer protects the bank if your extra shifts dry up or a flatmate decides to move out unexpectedly.

Your deposit size is another heavy hitter in the calculation, especially for first-home buyers. While a 20 per cent deposit is the standard goal, banks can still lend to those with less, though they will usually add a “low equity margin” to your interest rate to cover the extra risk. You also need to account for your household size and your deposit-to-loan ratios. Each dependent, whether it is a child or a non-working adult, is seen as an additional cost. This naturally reduces the amount of money the bank believes you have available to pay back a loan each month.

Understanding Income-to-Debt Limits

As of July 2026, the Reserve Bank has set firm boundaries that every borrower needs to understand. For people buying a home to live in, banks generally limit new lending to six times your gross annual income. If you are a residential investor, that limit shifts to seven times your income. This means even a high salary won’t help you borrow more if you are already carrying significant debt from car loans or personal finance. To get a better feel for how these numbers fit into the wider home buying and selling process, it is worth checking out government resources that break down the practical steps of the journey. If you are finding that the standard tools aren’t giving you the full picture, a professional review of your numbers can often reveal options you might have missed.

The Impact of “Hidden” Expenses

Small habits can have a surprisingly large impact on your final loan offer. Lenders now look closely at buy now, pay later schemes, often treating your total available limit as an active debt, even if you don’t owe a cent at the moment. Your regular subscriptions, from Netflix to your local gym, also get added to your living cost declaration. Being accurate and honest about these costs is essential. If a bank spots a pattern of high spending that contradicts your application, it can lead to a quick decline. Taking the time to tidy up these small leaks in your budget three months before you apply can significantly boost your standing in the eyes of a lender.

Why Different Lenders Give You Different Numbers

It is a common source of frustration for many Kiwis. You sit down at night, open a borrowing power calculator nz on one bank’s website, and get a number that feels great. Then, you try another, and the limit drops by fifty thousand dollars. This happens because every lender in New Zealand has its own internal “risk appetite.” They don’t all use the same math to decide what you can afford. Some might be more generous with how they view your bonuses, while others might be much stricter about your childcare costs. Each bank has its own set of rules that act like a filter for your application.

Using a neutral tool like the Sorted mortgage calculator is a fantastic way to get a baseline. It gives you a clear, unbiased look at what your repayments might look like without the slant of a specific bank’s policy. However, even a great tool cannot tell you which lender is currently looking to grow its mortgage book by being more flexible with its criteria. A broker can compare multiple calculators at once to find the most generous offer, ensuring you don’t miss out on a property just because one bank’s “cookie-cutter” rules didn’t fit your life.

Mainstream Banks vs. Non-Bank Lenders

Mainstream banks are designed for regular salary earners. If you have been in your job for years and have a tidy 20 per cent deposit, they are usually your first port of call. But life isn’t always that tidy. If you are self-employed, working as a contractor, or trying to buy with a smaller deposit, you might find the big banks are quite quick to say no. This is when looking at a 2nd Tier Lender New Zealand becomes essential. These non-bank lenders often provide alternative paths for people with unique financial profiles. We focus on bridging this gap, using our 20 years of banking experience to find the options that a standard bank tool simply cannot see.

The Role of Credit Scores in Your Calculation

Your credit score is essentially your financial reputation. While a calculator asks for your income and expenses, it often doesn’t account for your credit history until you actually apply. A poor score can “lock” you out of certain tiers of lending, even if you earn a high salary. Some lenders will decline an application over a single minor credit hiccup from years ago; others are more pragmatic and will look at why it happened and how you have managed your money since. It is a smart move to check your credit report before you get too deep into the house-hunting process. Knowing your score allows us to target the right lenders from the start, saving you from unnecessary declines.

How to Boost Your Borrowing Power Before You Apply

The number you get from a borrowing power calculator nz is just the starting line. You actually have a lot of control over that final figure. To get the best result, you should start organising your finances at least three months before you plan to buy. Banks usually want to see your last 90 days of bank statements, so this is your window to show them you are a reliable borrower. If you can prove that you are disciplined with your cash, lenders are much more likely to trust you with a larger loan.

Presenting “clean” bank statements is one of the most effective things you can do. It requires a bit of planning, but it is a simple fix. Follow these steps to tidy up your records:

- Cut back on the extras: You don’t need to live on bread and water, but reducing high-frequency spending like takeout or luxury subscriptions makes your living costs look much better on paper.

- Avoid unarranged overdrafts: Even a small dip into the red can signal to a lender that you aren’t quite on top of your cash flow.

- Clear your buy now, pay later services: Try to have all accounts for these services closed and cleared so they don’t appear as active credit limits.

- Label your transfers: If you are moving money to savings, label it clearly so the bank sees it as a positive habit rather than a mystery expense.

Managing Your Income-to-Debt Ratio

Many Kiwis fall into the “credit card trap” without realising it. Even if you have a zero balance, a $10,000 credit card limit can slash your borrowing power by a massive amount. The bank assumes the worst. They calculate your ability to pay based on the possibility that you might max out that card tomorrow. Closing unused cards or lowering the limits is one of the fastest ways to see a jump in your potential loan amount. Often, focusing on increasing your deposit is more effective than trying to squeeze out a small pay rise, as it lowers the bank’s risk and improves your overall position.

Proving Your Income for Complex Situations

Self-employed Kiwis often struggle with standard applications because their income can look less predictable to a bank’s computer. You will generally need to show stability through at least two years of financial accounts, but we can help you present these in the best light. If you are a first-time buyer, you might also consider using rental income from a flatmate or boarder to tip the scales. This extra cash can be added to your ability to pay back the loan, which makes a significant difference to the final offer. For more specific tips on getting started, check out our Home Loans for First Home Buyers guide. If you want to know exactly how much these changes will help your specific case, you can request a professional review of your finances to see where you stand.

Moving Beyond the Tool: Why a Mortgage Broker is Essential

While a borrowing power calculator nz provides a useful snapshot, it is essentially a static tool. It cannot account for the fact that the lending market moves every single week. Banks change their internal policies, interest rates fluctuate, and new rules from the Reserve Bank can shift your potential loan limit overnight. This is where having a seasoned advocate like Krish Krishna makes the difference. With over 20 years of banking experience, we don’t just look at the numbers; we look at the story behind them. We know which lenders are currently open to negotiation and how to present your case to get exceptions that a computer program would simply ignore. Having a veteran industry expert on your side means you have someone who has seen every possible scenario and knows exactly how to navigate the hurdles.

Beyond just finding the maximum amount, we help you decide on the right structure for your loan. Choosing between fixed and floating rates is not just about the lowest number today. It is about your long-term goals and your comfort with risk. If you plan to pay off your debt quickly or if you need the stability of knowing exactly what your bills will be for the next few years, the right structure is vital. We act as your dedicated negotiator, bridging the gap between the rigid world of big banks and your personal needs as a borrower. This hands-on approach ensures that you aren’t just another file in a system, but a priority.

Personalised Strategy vs. Online Estimates

If an online tool gives you a “no,” it is not necessarily the end of the road. Online estimates are often based on the most conservative settings and “cookie-cutter” rules that don’t account for your unique situation. We take a different approach by tailoring your application to highlight your specific financial strengths, whether that is a solid career path or a history of disciplined saving. We also conduct a professional “stress test” of your budget. This gives you genuine peace of mind, knowing that you can comfortably afford your home even if life throws a curveball or interest rates rise in the future.

Your Next Steps to Home Ownership

Moving from an estimate to a real-world offer is a straightforward process when you have the right support. To get started, gather your last three months of bank statements and your most recent payslips. These documents tell the story of your financial health and are the first things any lender will want to see. Once you have those ready, reach out for a no-obligation chat. We can look at your real-world options and help you find a lender that fits your specific financial profile. Ready to see your true borrowing power? Contact Mortgage Suite today.

Take the Next Step Toward Your New Home

A borrowing power calculator nz is a fantastic first step, but it only tells part of the story. Your true potential depends on how you present your finances and which lender you choose to partner with. Whether you are a first-home buyer navigating the 2026 market or an investor looking for more flexible 2nd tier options, the right strategy can turn a “no” into a “yes.”

You don’t have to figure this out on your own. With over 20 years of banking and brokerage experience, we specialise in finding the “hidden” potential that standard tools often miss. We provide personalised advocacy for first-home buyers and expert guidance for those who don’t fit the standard bank criteria. If you are ready to move beyond estimates and get a real-world plan, book a free consultation with Krish to find your true borrowing power. Your home-ownership goals are within reach, and we are here to help you navigate every hurdle with confidence.

Frequently Asked Questions

How much can I borrow for a home loan in NZ?

You can generally borrow between five to six times your gross annual income, though this depends on your specific debts and expenses. A borrowing power calculator nz will give you a rough estimate, but lenders also apply “stress tests” using interest rates higher than the current market. These tests ensure you can still manage repayments if rates rise, which is why your final offer might be lower than your gross income suggests.

Does a student loan affect my borrowing power?

Yes, your student loan definitely has an impact because it reduces your take-home pay every fortnight. Lenders look at your “net” income to see what is left for mortgage repayments, so the 12 per cent deduction for student loan repayments lowers your servicing capacity. Clearing this debt before you apply can often boost the amount a bank is willing to lend you.

Can I use my KiwiSaver as part of my deposit calculation?

You certainly can use your KiwiSaver savings as part of your deposit, provided you have been a member for at least three years. This extra cash increases your total deposit, which improves your Loan-to-Value Ratio (LVR). A larger deposit often makes you a more attractive borrower to the banks and can sometimes help you avoid the extra costs associated with low-equity loans.

What is the current DTI limit for NZ mortgages in 2026?

As of July 2026, the Reserve Bank has set the Debt-to-Income (DTI) limit at six times your gross income for owner-occupiers. For residential investors, the limit is slightly higher at seven times your income. Banks are allowed to do a small amount of lending above these levels, but most applicants will need to stay within these boundaries to get their loan approved.

How do credit card limits affect my borrowing power?

Lenders look at the total credit limit on your cards, even if you never use them and the balance is zero. They assume you could spend that entire limit tomorrow, so they factor the potential repayments into your monthly costs. Closing down unused cards or reducing your limits to a couple of thousand dollars is a quick way to see your borrowing potential jump.

Can I still borrow if I am self-employed or have a “2nd tier” profile?

Absolutely, you can still borrow if you are self-employed or don’t fit the standard bank profile. While mainstream banks might be hesitant, 2nd tier lenders specialise in looking at the bigger picture for business owners and those with unique income types. We focus on finding these alternative paths to ensure you aren’t locked out of the market just because your paperwork looks a bit different.

How often should I re-run a borrowing power calculator?

It is a good idea to re-run a borrowing power calculator nz whenever your financial situation changes or interest rates shift. If you get a pay rise, pay off a car loan, or if the Reserve Bank changes the OCR, your borrowing limit will move. Keeping an eye on these numbers helps you stay realistic about which properties you should be looking at during your search.

Will a small deposit of 5% or 10% reduce how much I can borrow?

Having a smaller deposit of 5 or 10 per cent usually means you can borrow less than someone with a full 20 per cent deposit. This is because banks have strict “speed limits” on how many low-deposit loans they can give out. You will also likely face a “low equity margin,” which is an extra interest cost that reduces the total amount you can comfortably service.