Bridging Finance NZ: A Simple Guide to Buying Before You Sell in 2026

You’ve just walked through an open home and found the perfect place, but your heart sinks because your current house isn’t even listed yet. It’s a gut-wrenching feeling to think you might lose your dream home simply because the timing doesn’t line up. You want to move forward, but the fear of being stuck with two mortgages or getting a “no” from the bank keeps you stuck in place.

We understand that the gap between buying and selling is where most of the stress lives. This is where bridging finance nz becomes your most valuable tool, allowing you to grab that new property now while you sort out the sale of your old one. It’s about taking control of the process rather than letting the calendar dictate your future.

In this guide, we’ll walk you through how bridging works in the 2026 market, including the total costs you can expect and the equity you’ll need to get started. You’ll learn the difference between open and closed bridges and how to find a lender that sees the full picture of your finances, ensuring a smooth transition into your next chapter.

Key Takeaways

- Solve the “chicken and egg” problem of buying a new home before you have sold your current one.

- Discover how bridging finance nz acts as a temporary link to cover your purchase price while you balance your total debt.

- Learn why becoming a “cash buyer” gives you a massive advantage when negotiating with sellers in the 2026 market.

- Understand the equity levels you will need and how to navigate the strict rules many banks have around these loans.

- Find out how a professional partner can simplify the application and help you move into your dream home without the stress.

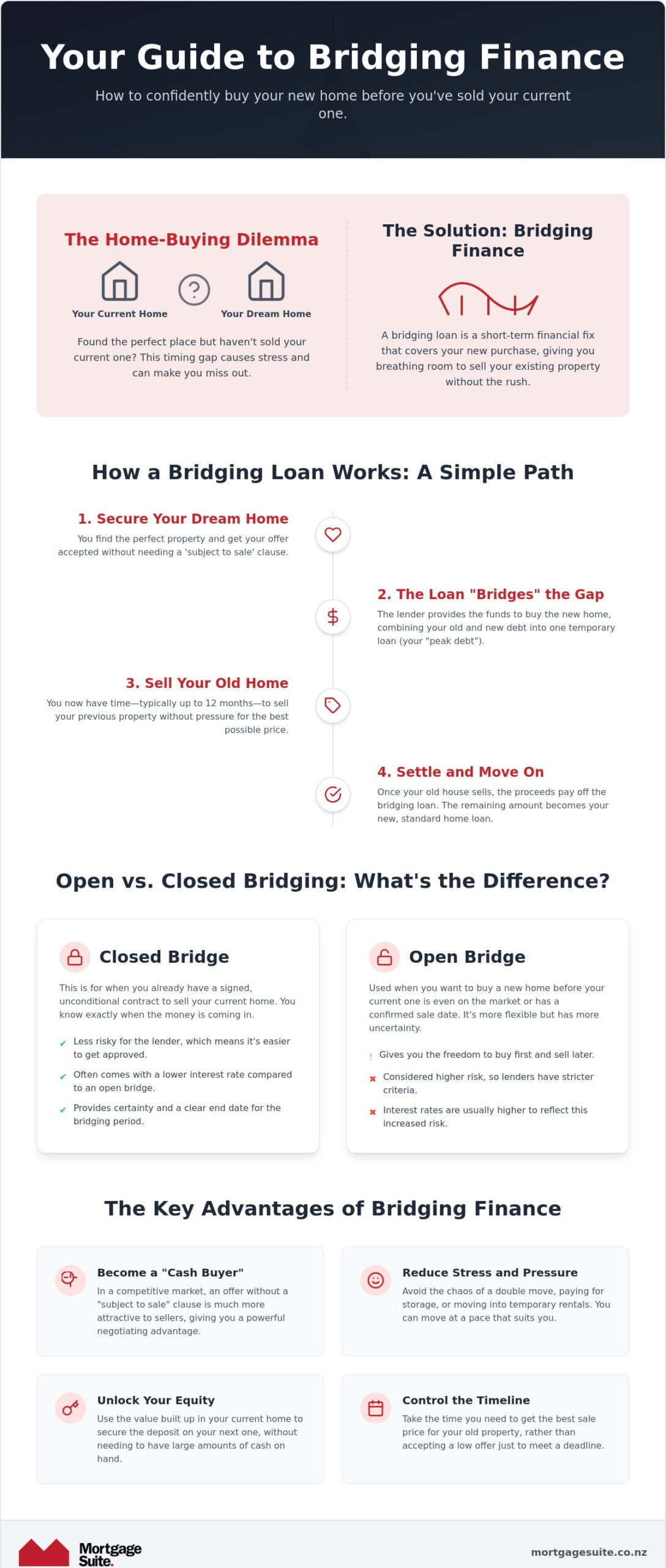

What is Bridging Finance and Why Might You Need It?

Buying and selling a home at the same time is often like a high-stakes game of musical chairs. You find the perfect spot, but the music hasn’t stopped on your current house yet. This is the classic “chicken and egg” dilemma. Do you sell first and risk having nowhere to live, or buy first and risk being stuck with two houses? It’s a stressful position to be in, but it’s one that many Kiwis face every day.

Bridging finance is the solution that fills this gap. If you’re wondering what is a bridge loan?, it’s essentially a short-term financial fix. It lets you purchase a new property before you’ve received the money from selling your existing one. When looking at bridging finance nz, think of it as a temporary safety net. It gives you the breathing room to transition between homes without the frantic rush of trying to match up settlement dates to the exact minute.

In the 2026 property market, timing has become even more important. While buyer demand is picking up, the high number of listings means that selling your own place can sometimes take longer than you’d like. You don’t want to lose your dream home just because your current sale is taking a few extra weeks to cross the finish line. Having bridging finance nz ready to go means you can act with confidence the moment you see the right property.

The Problem Bridging Finance Solves

One of the biggest headaches is the double move. Without a bridge, you often have to sell, move into a temporary rental, pay for storage, and then move again once you finally buy. This is expensive, time-consuming, and exhausting for the whole family. Bridging removes that middle step entirely.

- Competitive Edge: In a multi-offer situation, a “subject to sale” offer is often the first one a seller ignores. Bridging makes you a cash buyer, which is far more attractive.

- Reduced Pressure: You can take your time to pack and move properly, rather than trying to do everything in a single, chaotic weekend.

- Security: You won’t find yourself without a roof over your head if your purchase takes longer than your sale.

Who is This Type of Loan For?

This isn’t just an emergency measure. It’s a strategic tool used by many different types of buyers to get ahead. We often see it used by:

- Growing Families: When you’ve outgrown your current space, you need to move fast when a bigger house in the right school zone hits the market.

- Downsizers: If you’re looking for a smaller, easier lifestyle, you might want to secure your new apartment before listing the family home.

- Investors: If a prime opportunity pops up, you might need to pivot your portfolio quickly without waiting for a traditional settlement.

- Equity-Rich Homeowners: If you’ve been in your home for years, you likely have plenty of value built up but might not have the spare cash for a new deposit.

How Bridging Loans Work in New Zealand

Understanding how a bridge loan actually functions doesn’t need to be a headache. In simple terms, it is a short-term arrangement where the lender provides the money to buy your new home while you still own your current one. Instead of waiting for the cash from your sale to arrive, you use the value already sitting in your house to secure the funds you need right now. This type of bridging finance nz typically lasts for up to 12 months, which gives you a realistic window to find the right buyer and get your sale over the line.

During the time you own both properties, your lender looks at your finances as one big picture. They combine what you owe on your current mortgage with the new amount you are borrowing to buy the next house. This is your total combined debt. Because this is only a temporary setup, most lenders let you pay just the interest on the bridging part of the loan. This keeps your weekly or fortnightly payments much lower while you are between houses. When deciding if a bridge loan is right for you, looking at how these interest payments fit into your budget is a great place to start.

Once your old house is sold and the money comes in, that cash goes straight toward paying off the bridging loan. Any debt that is left over simply becomes your new standard mortgage on the house you’ve moved into. It is a very tidy way to handle a move without needing to have all your cash ready on day one. If you want to see how the numbers might work for your specific move, you can get a clear picture of your options here.

Closed vs Open Bridging

The process usually falls into two categories: closed or open. A closed bridge is the most straightforward because you already have a signed, final sale contract on your current home with a set date for the money to arrive. Banks feel very safe with this because they know exactly when the loan will be paid back. An open bridge is for when your home is on the market but hasn’t sold yet. This is a bit more flexible but usually comes with stricter rules because the lender wants to be sure you can manage the debt if the sale takes a little longer than planned.

Calculating Your Total Combined Debt

To work out if you can afford the move, lenders calculate your total combined debt by adding your current mortgage to the purchase price of the new place. Because they are lending you a significant amount at once, they need to be certain about what both properties are actually worth. You will likely need a professional valuer to visit and provide an up-to-date report. This ensures there is enough of a safety margin in your home’s value to protect everyone if market prices shift before you manage to sell.

The Pros and Cons of Bridging Your Property Gap

Choosing to use bridging finance nz is a bit like buying a front-row ticket to a show. You get the best view and the most convenience, but there is a premium to pay for that privilege. For many homeowners in 2026, the trade-off is worth it because it removes the massive pressure of having to sell before you can even dream of making an offer on a new place. It turns you into a much stronger buyer in a market where sellers value certainty and speed above all else.

While the convenience is obvious, it is a strategic financial move that requires a clear head. You are essentially betting on the value of your current home to cover the gap. If the market is moving quickly, this is a brilliant way to stay ahead. However, if things slow down, you need to be prepared for the costs of holding two properties at once. It is about balancing the emotional relief of securing your dream home with the practical reality of managing a larger, temporary debt.

Why Homeowners Choose to Bridge

The most immediate benefit is your standing in the eyes of a seller. When you make an offer that isn’t conditional on selling your own home, you’re viewed as a cash buyer. This often allows you to negotiate a better price or beat out other buyers who are still waiting for their own sales to go through. In a market where the national median house price is around $786,977, having that extra negotiation power can save you thousands on your purchase price.

- Family Stability: Your kids don’t have to change schools twice or live out of boxes in a temporary flat while you wait for a settlement.

- Market Timing: If you find a bargain or a rare property, you can strike immediately rather than watching it sell to someone else.

- Reduced Moving Costs: You avoid the “double move,” which means no expensive storage units or paying removalists twice in six months.

Risks to Keep in Mind

The main risk is the cost of time. While your bridge is in place, interest is usually calculated daily and added to your total debt. If your home takes longer to sell than expected, these holding costs can eat into the profit you were counting on from your sale. It is vital to understand your rights under NZ consumer protection laws for borrowers, which ensure that lenders are acting responsibly and that you aren’t being pushed into a situation you can’t manage financially.

You also need to consider what happens if your home sells for less than you hoped. If you have already committed to a high purchase price on the new house, a lower sale price on the old one means you will end up with a larger long-term mortgage. This could affect the mortgage rates nz lenders offer you later, especially if your loan-to-value ratio is higher than originally planned. Having a realistic sale price and a solid backup plan is essential for any successful bridge.

Is Bridging Finance Right for Your Situation?

Deciding if bridging finance nz is the right move for you comes down to how much extra value you have in your current home. Lenders usually want to see an equity safety net of at least 20% of the new property’s purchase price. This acts as a cushion to protect everyone if market conditions change. While the big banks can be quite hesitant about open bridging, it’s often because they want to see a rock-solid “Plan B.” You need to be honest about what you’ll do if your home doesn’t sell within your expected timeframe, whether that involves adjusting your price or looking at alternative ways to manage the debt.

Mainstream banks often have very strict rules that don’t always account for the reality of a changing market. They might look at your income and decide you can’t technically afford two mortgages, even though the situation is only temporary. This is where many homeowners get stuck, but it’s important to remember that the bank’s criteria aren’t the only ones out there. Assessing your situation requires looking beyond the standard “no” and finding a path that recognises the value in your property and your long-term goals. Some homeowners also use this period of reassessment to explore whether a construction loan NZ might be a better fit if they’d prefer to build their next home rather than buy an existing one.

When the Bank Says No: 2nd Tier Options

If your main bank has said no, it doesn’t mean you’ve reached a dead end. A 2nd tier lender New Zealand can often provide the flexibility that larger institutions lack. These lenders focus more on the value of your assets and your plan to pay back the loan rather than just a standard income test. While the rates might be a little higher, this option is a practical way to get the deal done when the timing is tight and you don’t want to lose your dream home simply because of a bank’s rigid checklist.

Bridging for Investors and Developers

For property experts, bridging is a strategic choice rather than just a way to move house. It is frequently used to secure residential investment property loans NZ, allowing you to jump on a great deal without waiting for another sale to settle. It also plays a huge role in property development loans NZ, helping you keep your projects moving forward by using your existing equity to fund the next stage of growth. Landowners looking to unlock the value of their sections will find that understanding subdivision finance NZ is equally important when planning how to fund and sequence a land project alongside other property moves. If you’re ready to see if this path fits your goals, chat with our team about your situation here to find a solution that works for you.

Getting Your Bridging Finance Sorted with Mortgage Suite Ltd

Sorting out bridging finance nz isn’t something you should have to figure out on your own. While the concept of a “tideover” loan is simple, the actual application involves a lot of moving parts that need to be managed carefully. You need a partner who has seen every market cycle and knows exactly how to present your case to a lender. We take the weight off your shoulders at Mortgage Suite Ltd by acting as your advocate, negotiator, and guide through the entire process.

Our role is to bridge the gap between the rigid requirements of institutional banking and your personal needs as a homeowner. We don’t just fill out forms. We look at your total financial picture to find the most cost-effective path forward. Whether that means negotiating a better rate with your current bank or looking at alternative paths, our goal is to make sure you aren’t paying a cent more than necessary. We also handle the constant back and forth between your lawyer and the lender, ensuring that everyone is on the same page for your settlement dates.

The Mortgage Suite Ltd Approach

At the heart of our service is Krish Krishna’s 20 plus years of deep banking experience. Having spent two decades inside the system, Krish knows exactly how lenders think and what they need to see to say “yes” to an application. We pride ourselves on giving jargon-free advice that puts your family’s security first. At Mortgage Suite Ltd, we speak your language, not “bank-speak,” so you always feel in control of your decisions. It’s about building a partnership where you feel supported rather than just processed like another number in a queue.

Your Next Steps to a New Home

If you have found a house you love and need to move quickly, the best thing you can do is get organised early. Having a plan in place before you sign a contract gives you a massive advantage when you start negotiating. Here is how we get started together at Mortgage Suite Ltd:

- Gather Your Documents: We will need your current mortgage statements and recent property appraisals for both your current home and the one you want to buy.

- Run the Numbers: We’ll have a conversational chat to look at your equity and work out exactly what your total debt and repayments will look like.

- Get Pre-Approved: We aim to get you a pre-approval as fast as possible so you can bid at auction or make an offer with total confidence.

Moving house is a big milestone. It should be an exciting time, not a source of constant anxiety. By letting us handle the complexities of your bridging finance nz, you can focus on the fun part: planning your life in your new home and getting settled into your new community.

Ready to Secure Your New Home with Confidence?

Navigating the gap between your current property and your next one doesn’t have to be a source of anxiety. As we have explored, bridging finance nz acts as a vital tool to help you act quickly when the right opportunity appears, removing the pressure of perfectly timed settlement dates. Whether you are a growing family or a seasoned investor, having a clear strategy ensures you don’t miss out on your dream home while waiting for a sale. If your next move involves building rather than buying, exploring a construction loan NZ alongside your bridging strategy could open up even more options for your 2026 property plans.

Our team provides nationwide service across New Zealand, bringing over 20 years of banking and brokerage expertise to every client. We are specialists in 2nd tier and alternative lending, meaning we can often find a path forward even when mainstream banks are hesitant. We are committed to making the process straightforward and jargon-free, so you can focus on the excitement of your move.

Talk to Krish about your bridging options today and let us help you map out a seamless transition. You deserve a steady hand to guide you through the numbers and into your new front door.

Frequently Asked Questions

How long does a bridging loan typically last in NZ?

A bridging loan in New Zealand is a short term solution that usually lasts for a maximum of 12 months. This timeframe is designed to give you plenty of breathing room to list, market, and sell your current property without feeling rushed. Most homeowners find they can settle their sale within three to six months, at which point the bridging portion of the debt is paid off in full.

Can I get bridging finance if I haven’t sold my house yet?

Yes, you can definitely secure bridging finance nz before your current house is sold. This is what the industry calls an “open bridge.” While it requires a bit more paperwork than a “closed bridge” where a sale is already unconditional, it is a very common way for Kiwis to lock in a new home. You will just need to show the lender a clear plan for your sale and have enough equity to cover the risk.

Do I need a large deposit for a bridging loan?

You don’t necessarily need a large cash deposit because the equity in your current home acts as the security for the loan. Lenders look at the combined value of both properties rather than a pile of cash in your savings account. If you have built up enough value in your current home over the years, you can often borrow the full purchase price of the new property without needing any extra cash upfront.

Are bridging loan interest rates higher than normal mortgages?

Interest rates for bridging are generally higher than standard long term mortgage rates. Lenders typically charge their standard floating or variable rate plus a premium, which is commonly between 1% and 2% per year. Because these loans are only intended to last for a few months, most people see the extra interest as a fair trade for the ability to move into their new home sooner.

What happens if my house sells for less than the peak debt?

If your house sells for less than you hoped, the leftover debt simply stays as part of the mortgage on your new home. This means you will end up with a larger long term loan than you might have first calculated. It is a good idea to be conservative with your sale price expectations from the start so you don’t have any stressful surprises when the final bank statements arrive.

Can I use KiwiSaver funds for bridging finance?

Generally, you cannot use KiwiSaver funds for bridging finance because those withdrawals are mostly reserved for first home buyers. Since bridging is specifically for people who already own a property, you won’t be able to tap into your KiwiSaver to cover the gap. Instead, you will need to rely on the equity you have built up in your current home to act as your deposit and security.

How much equity do I need to qualify for bridging?

To qualify for bridging finance nz, most lenders will want to see that you have at least 20% usable equity in your existing property. This means your total borrowing across both the old and new houses shouldn’t exceed 80% of their combined market value. Having this 20% buffer protects both you and the lender if house prices shift while you are waiting for your sale to settle.

Is it better to sell my house before I start looking for a new one?

Selling first gives you total certainty about your budget, but it can also leave you rushed to find a new place or forced into a rental. Looking first and using a bridge gives you the freedom to wait for the perfect home to appear. It is a strategic choice that depends on how much equity you have and how confident you feel about the current market demand for your property.