Business Expansion Loans NZ: Your 2026 Guide to Funding Growth

What if the biggest hurdle to your next big move isn’t your balance sheet, but a bank’s outdated rulebook? If you’ve spent weeks waiting for a callback or felt the sting of a “no” because your financials don’t fit a tidy little box, you aren’t alone. Many Kiwi owners find that securing business expansion loans nz feels like a full-time job in itself, especially with interest rates shifting and traditional lenders often tightening their grip.

It’s incredibly frustrating to have a clear vision for growth but feel stuck behind red tape and confusing talk about using your assets to back a loan. We understand that you need a partner who sees the potential in your numbers, not just the risks. This guide will show you exactly how to find your way through the 2026 lending landscape, from understanding the latest changes to lending rules to choosing between a mainstream bank and a fast-acting lender outside the big banks. You’ll learn how to structure your application to buy a new venture or scale your current one, giving you the confidence to secure the funding you deserve.

Key Takeaways

- Learn why borrowing to scale your operations is a strategic move that’s very different from just covering daily costs.

- Discover how to compare big banks and non-bank lenders to find a solution that actually fits your unique situation.

- Get a clear plan for preparing your financials to secure business expansion loans nz without getting stuck in bank red tape.

- Find out how to use term loans and other finance options to buy a competitor or move into a new market.

- See how having a veteran negotiator on your side can help you overcome hurdles and get your funding approved much faster.

What is a Business Expansion Loan and Why Does Your Strategy Matter?

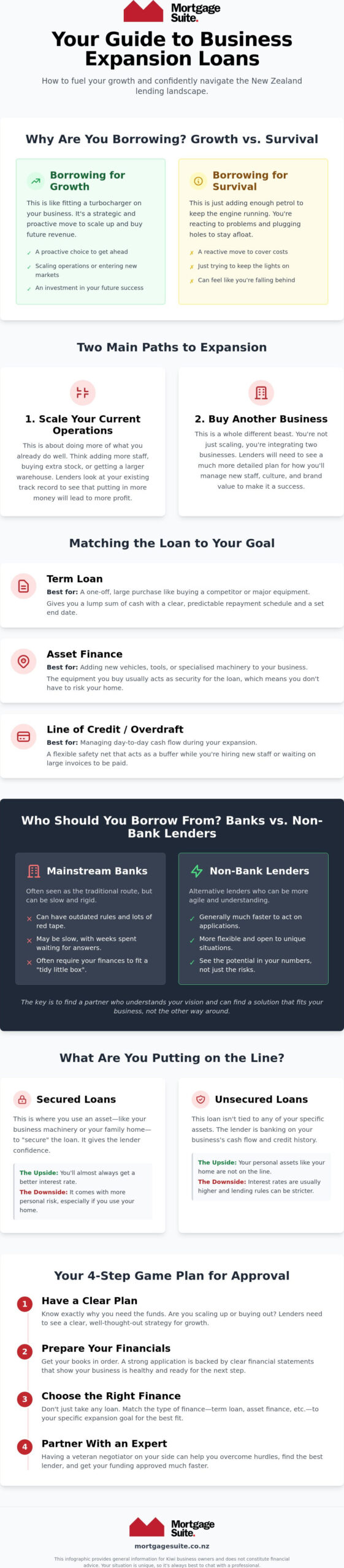

Think about your business like a car. Sometimes you need a bit of petrol just to keep the engine turning over, but an expansion loan is more like fitting a turbocharger. At its core, a business loan designed for growth is a specific type of funding used to scale your operations, enter new markets, or even buy out a competitor. It’s a tool that helps you move past the “ceiling” many Kiwi business owners hit when they have plenty of customers but simply don’t have the staff, space, or equipment to serve them all.

Taking on debt for growth is fundamentally different from borrowing just to stay afloat. When you borrow for survival, you’re often plugging holes. When you look into business expansion loans nz, you’re actually buying future revenue. It’s a proactive choice rather than a reactive one. However, the specific way you plan to grow will dictate exactly what kind of finance you need. A plan to hire five new sales reps in Auckland requires a different financial structure than a plan to buy a rival firm in Christchurch.

Expanding Your Current Operations vs. Buying a New Business

Scaling up your existing setup usually involves gradual steps. You might need extra stock to meet seasonal demand or a larger warehouse to centralise your logistics. Lenders look at your track record here; they want to see that your current model works and that more capital will simply mean more profit. It’s about doing more of what you’re already good at.

Buying a business is a different beast entirely. You aren’t just scaling; you’re integrating. You have to consider existing staff, different cultures, and the actual value of the brand you’re taking over. Because there are more moving parts, a lender will want to see a much more detailed plan for how the two pieces will fit together without the wheels falling off. The “how” of your acquisition is just as important as the “how much”.

The Emotional Side of Growing Your Business

Let’s be honest: expansion is stressful. It often feels like you’re “betting the farm” on your own ability to succeed. This “betting on yourself” can keep you up at night, especially when you start thinking about the responsibility you have toward your team. It’s natural to feel a bit of anxiety when the numbers get bigger.

Having a steady hand in your corner makes a massive difference. Professional advice helps shift your mindset from the anxiety of “owing money” to the excitement of investing in your future. When you have a clear path and a solid negotiator on your side, that weight on your shoulders starts to feel a lot lighter. It’s about turning that nervous energy into the fuel you need to take your business to the next level with the right business expansion loans nz.

Choosing the Right Finance: Different Loans for Different Growth Goals

Finding the right fit for your expansion isn’t just about the dollar amount. It’s about how that money flows in and out of your business. You might need a lump sum for a big purchase, or perhaps a safety net for those months when you’re waiting for new contracts to pay out. For many, business expansion loans nz come in the form of a term loan. This is the go-to for buying a competitor or investing in heavy equipment because it gives you a clear end date and a set repayment schedule.

Asset finance is particularly useful because the equipment itself usually serves as the backup for the lender. This means you don’t have to lean as heavily on your personal home equity to get the tools you need. If you’re a tradie looking to add three more vans to your fleet or a manufacturer needing a specialised machine, this keeps your other credit lines open for daily operations. If you’re worried about cash flow while you hire new staff, a flexible credit line or an overdraft can act as a buffer. While you’re weighing these up, don’t forget to look into financial assistance for small business owners to see if there are any grants or incentives that could complement your loan.

Secured vs. Unsecured: What Are You Putting on the Line?

Lenders often ask for “security”, which is just a way of asking what you’ll use to back the loan if things don’t go to plan. You can use business assets like machinery, or you might use personal property like your home. Using your home often unlocks the best rates for business expansion loans nz, but it comes with more personal risk. Unsecured loans don’t tie up your assets, but they usually have higher interest rates and stricter rules because the lender has less protection. It’s a trade-off between lower costs and the level of risk you’re comfortable carrying.

Fixed vs. Floating Rates for Business Growth

Fixed rates offer the peace of mind of knowing exactly what your repayments will be for the next few years. This is a huge help when you’re trying to manage a tight budget during a growth phase. Floating rates move with the market. They offer more flexibility, allowing you to make extra payments whenever you have a bumper month. For a deeper dive into how these rate structures work, our guide on mortgage rates nz explains the mechanics in plain English. Often, the best move is a mix of both, and getting a professional opinion from Mortgage Suite Ltd can help you strike that balance.

Bank vs. Non-Bank Lenders: Finding the Best Fit for Your Expansion

Most Kiwi business owners head straight to their local branch when they need a boost. It’s the natural first step. However, the big banks often have very rigid boxes that you need to fit into. If your profit and loss statement looks a bit different because you’ve been reinvesting every cent, or if you’ve only been trading for eighteen months, a traditional bank might see you as too risky. This is where the wider world of business expansion loans nz becomes very interesting.

There is a whole group of lenders outside the main street branches that look at things differently. These are often called 2nd tier or alternative lenders. They aren’t necessarily better or worse than a bank; they just have different rules. While a bank might focus purely on your past three years of tax returns, an alternative lender might look more closely at your current contracts and future potential. They often fill the gap when mainstream banks pull back, providing a steady hand when you need it most.

When the Bank Says No: Common Hurdles for NZ SMEs

It’s a common story. You have a great business, but the bank says no because your financials aren’t “clean” enough. Maybe you’re self-employed and haven’t hit that magic two year mark yet. Or perhaps you work in an industry that the bank has flagged as high risk. It can feel like a dead end. This is exactly where Krish Krishna’s twenty years of banking experience comes into play. He knows how bank managers think because he used to be one. He can look at your situation and spot the workaround that a standard bank computer might miss.

The Advantage of Alternative Lending

One of the biggest wins with alternative options is speed. Traditional banks can take anywhere from two to four weeks just to give you an initial answer. In the fast moving world of business, that’s an eternity. Many non-bank lenders can provide a decision and funding much faster, sometimes within a few days. This allows you to jump on an opportunity before a competitor does.

These lenders are also far more open to tailored terms. They can often build a repayment schedule that matches your new revenue stream, giving you breathing room while your expansion starts to pay off. As specialists in 2nd tier lender New Zealand solutions, we help you tell your story to the right people. It’s about finding a lender that sees the person and the potential, not just the paperwork. Securing business expansion loans nz doesn’t have to be a battle if you’re looking in the right places.

How to Get Your Business Loan Approved: A Step-by-Step Guide

Getting a green light for your funding isn’t just a matter of luck or having a massive bank balance. It’s about being prepared and presenting your case in a way that makes sense to a credit manager. If you want to secure business expansion loans nz, you need to show that you aren’t just dreaming big; you’re planning smart. Here is a clear path to getting your application over the line.

- Step 1: Get your house in order. Lenders will want to see your most recent profit and loss statements. They need to know your current business is healthy enough to support the extra debt.

- Step 2: Build your growth plan. This is where you explain exactly how the extra capital will generate more revenue. If you’re buying a new machine, how much more can you produce? If you’re hiring staff, how many more clients can they handle?

- Step 3: Identify your security. We have discussed using assets or property already. Decide early on what you’re willing to put forward and what you’d prefer to keep separate.

- Step 4: Package it professionally. This is where working with a specialist makes a world of difference. We know what certain lenders love to see and what makes them nervous.

The “Growth Plan”: What Lenders Actually Want to See

A basic business plan won’t cut it when you’re looking for significant funding. Lenders want an expansion roadmap. This means proving your systems and team are ready for the extra weight. If your sales double overnight, can your current office manager handle the admin? Do you have the software to track the new stock? You also need to be honest about the “dip”. Most expansions cost money before they make money, so your cash flow forecasts must show you have enough of a buffer to survive that initial phase.

Navigating the Sale and Purchase Agreement

If you’re using a business loan to buy a business nz, things get a bit more technical. You’ll have a Sale and Purchase Agreement that needs to be carefully aligned with your finance offer. It’s vital to have your lawyer and your broker talking to each other from the very start. This prevents any nasty surprises on settlement day. If your growth involves building a new warehouse or showroom, you might also want to look into property development loans nz to handle the construction side of things. Ready to get started? Talk to us today to begin packaging your application for success.

Partnering with Mortgage Suite Ltd to Secure Your Business Future

Business growth is rarely a straight line. It’s often filled with unexpected turns and decisions that can feel quite heavy when you’re making them on your own. This is where we come in. At Mortgage Suite Ltd, we don’t just see ourselves as a bridge to a loan; we see ourselves as your partner in growth. Having a veteran negotiator in your corner means you aren’t just one of thousands in a bank’s queue. You have someone who understands the nuances of business expansion loans nz and knows exactly how to present your vision to the people holding the purse strings.

Krish Krishna brings over two decades of deep industry experience to the table. Because he spent years working inside the banking system, he knows the internal language and the specific hurdles that often trip up even the best applications. Mortgage Suite Ltd works for you, not the bank. This insider knowledge is a powerful tool when you’re trying to secure funding for a complex commercial project or a quick business acquisition. We take a personal, conversational approach to finance. We believe that if you can’t explain a loan in plain English, it’s probably not the right one for you. Our goal is to remove the obstacles so you can focus on what you do best.

Why a Broker is Better Than Going Direct

Walking into your own bank only gives you one set of options. Working with a broker gives you access to a huge range of lenders across New Zealand, many of whom don’t deal directly with the public. This includes those 2nd tier lenders we discussed earlier who are often more flexible and faster to act. We do the legwork, the phone calls, and the paperwork while you stay focused on running your business. It saves you time, but it also provides long-term peace of mind. We’re here for the journey, helping you move from your first home loan through to major commercial expansions and property development projects.

Ready to Take the Next Step?

If you’re feeling a bit stuck or just want to see what’s possible, reach out for a no-obligation chat about your goals. No question is too simple, and no expansion goal is too big. We’ve seen almost every scenario imaginable over twenty years in the industry, and we know how to find the path forward when others see a dead end. Whether you’re just starting to look at business expansion loans nz or you have a sale and purchase agreement sitting on your desk, we’re here to help you navigate the process with confidence. Let’s talk about your business expansion today and get your growth plans moving.

Take the Next Step Toward Your Business Goals

Scaling up is one of the most exciting phases of your journey, but it shouldn’t be the most stressful. We’ve explored how the right strategy dictates your funding, why 2nd tier lenders offer the flexibility you need, and how to package an application that gets results. Whether you’re moving into a larger centre or buying out a competitor, securing business expansion loans nz is about finding a lender that sees your potential, not just your paperwork.

With over 20 years of banking expertise, we specialise in navigating the alternative lending market to find solutions when the big banks say no. You’ll receive personalised, jargon-free advice that puts your goals first, ensuring you have a steady hand guiding you through every complex financial decision. We handle the heavy lifting so you can stay focused on leading your team and serving your customers.

Talk to Mortgage Suite Ltd about your business growth today. Your next big move is within reach, and we’re ready to help you take it with total confidence.

Frequently Asked Questions

Can I get a business loan to buy a business in NZ without a deposit?

You usually need some form of equity or a cash deposit to buy a business in New Zealand. While “no deposit” loans are very rare, you can often use the equity in your home or other property to cover the deposit amount. This allows you to secure the funding you need without having to find a large pile of cash first.

How long does it typically take to get a business expansion loan approved?

Approval times vary depending on which lender you choose. A traditional bank might take anywhere from two to four weeks to process your application and give you a final answer. If you are in a rush, lenders outside the big banks can often provide a decision within a few days, which is vital for securing business expansion loans nz before a competitor moves in.

What is the difference between a business loan and a commercial mortgage?

The main difference is what the money is used for and what backs the debt. A business loan is generally for growth activities like hiring staff, buying stock, or marketing. A commercial mortgage is specifically for purchasing the physical property where your business operates. In that case, the land and building serve as the backup for the lender.

Do I have to use my home as security for a business growth loan?

No, you don’t always have to use your family home to back the loan. You can often use business assets like machinery, vehicles, or even the value of your unpaid invoices. However, using a home often unlocks the lowest possible interest rates because it represents less risk for the lender. Options that don’t require your home as backup exist but usually come with higher costs.

What happens if my business financials aren’t “perfect” according to the bank?

If the big banks say no because your financials don’t fit their rigid boxes, you still have options. Specialist lenders look past the standard paperwork to see the potential in your business. They focus on your future prospects and current contracts rather than just your past tax returns. This is where having an experienced negotiator from Mortgage Suite Ltd helps you tell the right story to the right people.

How much can I actually borrow for a business expansion in New Zealand?

The amount you can borrow depends on your business’s ability to pay back the loan comfortably. Lenders look at your yearly turnover and your net profit to decide your financial capacity. When applying for business expansion loans nz, they will also consider the extra income your growth plan is expected to generate once the new funding is in place.

Is it better to get a fixed or floating interest rate for my business loan?

It depends on whether you value certainty or flexibility more. A fixed rate gives you the peace of mind of knowing exactly what your repayments are each month, which helps with budgeting. A floating rate moves with the market and offers the flexibility to pay the loan off faster without any penalties. Many business owners choose to split their loan to get a bit of both.

Can I get a loan to buy out my business partner?

Yes, buying out a business partner is a very common reason for seeking finance in New Zealand. Lenders treat this much like a standard business purchase. They will look at the health of the company and ensure that you, as the remaining owner, have the skills and the financial capacity to manage the debt and the operations on your own.