Investment Property Mortgage Calculator NZ: How to Calculate Repayments for Your 2026 Portfolio

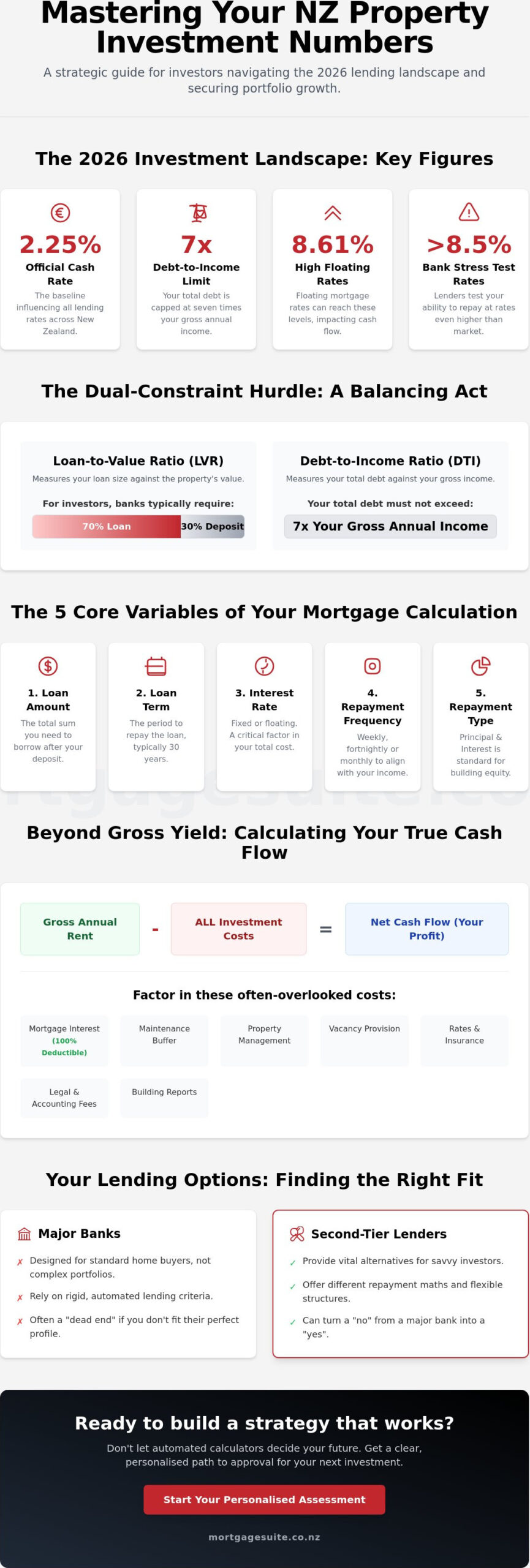

What if your next property investment approval didn’t depend on a bank’s rigid checklist, but on your ability to master the numbers before you even apply? With the Official Cash Rate sitting at 2.25% and DTI limits of seven times your gross income now firmly in place, using an investment property mortgage calculator nz is no longer just about checking repayments. It is about understanding how your total debt profile fits within the Reserve Bank’s 2026 framework to ensure your portfolio remains viable.

We understand the frustration of finding a perfect property only to be met with confusion over 2nd tier lending rates or the complexities of the current dual-constraint system. It is natural to feel a bit of pressure when trying to organise your cash flow while floating rates sit as high as 8.61%. This guide promises to clear that fog, providing you with a clear understanding of your monthly costs and a path to approval even if mainstream lenders hesitate. We will preview the latest LVR restrictions, explain the impact of 100% interest deductibility, and give you the confidence to execute a property strategy that works for your specific financial goals.

Key Takeaways

- Identify the five core variables, including interest rates and repayment frequency, to accurately forecast your portfolio’s monthly cash flow.

- Master the dual-constraint system of LVR and DTI limits by using an investment property mortgage calculator nz to determine your true borrowing capacity in the 2026 market.

- Learn why calculating for investment requires a focus on yield and serviceability rather than just simple home loan affordability.

- Discover how 2nd tier loans provide a vital alternative for investors who find themselves outside the strict lending criteria of the major banks.

- Follow our step-by-step template to account for often-overlooked costs like legal fees and building reports when establishing your total loan requirement.

Table of Contents

-

Navigating the Numbers: Why You Need an Investment Property Mortgage Calculator in NZ

-

Understanding the Variables: What Actually Goes Into Your Repayment Calculation?

-

The LVR and DTI Hurdle: Calculating Your Real Borrowing Power

-

A Step-by-Step Template to Forecast Your Investment Cash Flow

-

Beyond the Calculator: How Tailored Financing Secures Your Portfolio

Navigating the Numbers: Why You Need an Investment Property Mortgage Calculator in NZ

Successful property investment in New Zealand starts long before you visit an open home. It begins at your desk, crunching numbers to ensure a deal actually stacks up in the current 2026 economic environment. While many people use a basic tool to see what they can borrow, a dedicated investment property mortgage calculator nz serves a much more strategic purpose. It acts as your first line of defence against over-leveraging. It is about moving beyond "can I afford this?" to "does this asset work for me?"

In 2026, the landscape has shifted. With the Official Cash Rate at 2.25%, banks are looking closer than ever at your total debt-to-income (DTI) ratio. Calculating your repayments isn’t just about finding a monthly figure; it is about stress testing your strategy against potential interest rate hikes. If you can’t show a clear path to serviceability when banks apply their "test" rates, which often exceed 8.5%, your application will likely end up in the declined pile. Accurate preparation ensures you present a professional, viable case to lenders from the outset.

The Difference Between Yield and Cash Flow

Gross yield is a helpful starting point, but it’s often a vanity metric that can lead investors astray. It simply measures the annual rent against the purchase price. To build a sustainable portfolio, you must focus on net cash flow. This is where your mortgage repayment is just one piece of the puzzle. You need to account for the fact that 100% of your interest is now deductible, which significantly aids your bottom line compared to previous years. However, savvy investors also calculate a "buffer" for maintenance, property management, and potential vacancies. Understanding how mortgage calculators work helps you see how these variables interact with your loan principal to create a true picture of your weekly outgoings.

Why ‘Big Bank’ Calculators Often Fall Short

Most mainstream banking tools are designed for the average home buyer with a standard salary and a perfect credit score. They rarely account for the complexities of an investment portfolio, such as the nuances of 2nd tier lending or the specific 70% LVR requirements for investors. If your situation doesn’t fit the rigid "Big Four" criteria, their automated algorithms might suggest you’re at a dead end. We believe in personalised advocacy over automated results. 2nd tier lenders often offer different repayment maths that can turn a "no" into a "yes," provided you have organised your figures correctly using an investment property mortgage calculator nz that reflects the real-world market.

Understanding the Variables: What Actually Goes Into Your Repayment Calculation?

Calculating repayments isn’t a guessing game; it’s a precise exercise in financial forecasting. To get a reliable result from an investment property mortgage calculator nz, you must look beyond the sticker price of the house. There are five core variables that dictate your success: the loan amount, the loan term, the interest rate, the payment frequency, and the repayment type. Your deposit size is the first hurdle. While the Reserve Bank generally requires a 30% deposit for investors, having a larger equity stake can often unlock more competitive interest rate tiers. If you find the big banks are being too restrictive with their terms, exploring residential investment property loans can provide the tailored approach you need to keep your portfolio growing.

Local investors have the choice of weekly, fortnightly, or monthly instalments. Matching your repayment frequency to your rental income cycle can make your cash flow much easier to organise. Principal and Interest is the standard method for building equity over a 30-year term. However, the type of debt you choose significantly shifts the math. For example, a 30-year term is standard, but some 2nd tier lenders might offer different structures that suit a short-term development or a rapid equity-build strategy.

Fixed vs. Floating Rates: Which Number Should You Use?

Choosing an interest rate for your calculation requires a balanced view of the 2026 market. Fixed rate mortgage options currently range from approximately 4.65% for a one-year term to 5.86% for three years, providing the budget certainty many investors crave. Floating rates, while averaging around 6.15%, offer the flexibility to make extra payments without penalty. When using an investment property mortgage calculator nz, don’t just use today’s advertised specials. It’s wise to use a "test rate" of around 8.5% to ensure your portfolio remains robust even if the Reserve Bank raises the OCR again.

The Interest-Only Strategy for Investors

Interest-only repayments remain a popular choice for Kiwi investors looking to maximise tax efficiency. With 100% interest deductibility fully restored as of April 2025, this strategy helps keep immediate outgoings low while you focus on capital growth or paying down your non-deductible home loan. While this improves your short-term cash flow, it’s vital to calculate the "cliff"; the moment your interest-only period ends and your repayments jump to include principal. Planning for this transition ensures you aren’t caught off guard by a sudden increase in your weekly commitments.

The LVR and DTI Hurdle: Calculating Your Real Borrowing Power

Having a healthy deposit is only half the battle in the 2026 lending environment. While earlier sections focused on the mechanics of repayments, you must also clear the dual hurdles of Loan-to-Value Ratio (LVR) and Debt-to-Income (DTI) restrictions. Currently, the Reserve Bank requires most investors to provide a 30% deposit, meaning your LVR cannot exceed 70%. However, even with a massive pile of cash, your "real" borrowing power is now firmly capped by DTI limits. For most mainstream banks, your total debt cannot exceed seven times your gross annual income. This creates a hard ceiling that an investment property mortgage calculator nz can help you identify before you spend money on building reports or valuations.

Many investors feel the sting of "rental shading" during the application process. Banks rarely count 100% of your projected rental income when calculating serviceability. Instead, they typically recognise only 75% to 80% of the rent to account for costs like rates, insurance, and property management. If you have plenty of equity but the bank says your income is too low, this shading is often the culprit. It’s a common point of frustration, but understanding these internal bank formulas allows you to adjust your strategy and look for properties with higher yields that can offset the income gap. To fully understand how the 6x and 7x thresholds affect your specific situation, our detailed guide on the debt to income ratio NZ rules and what they mean for your 2026 mortgage breaks down the exact maths lenders use.

Unlocking Equity in Your Existing Portfolio

You don’t always need cash in the bank to fund your next move. Usable equity is the secret weapon for growing a portfolio, calculated as the difference between your current mortgage and 80% of your property’s value. For those who have seen significant capital gains since they first secured home loans for first home buyers New Zealand, this equity can often cover the entire 30% deposit for an investment. It’s a methodical way to leverage your existing assets without draining your personal savings, provided you maintain a steady hand on your total debt levels.

When the Mainstream Banks Say No

If your DTI ratio sits slightly above the "Big Four" threshold of seven, it doesn’t mean your investment journey is over. 2nd tier lenders often provide a vital alternative, as they can be more flexible with complex income structures or higher debt levels. When you use an investment property mortgage calculator nz to model these scenarios, you should account for slightly higher interest rates, often 0.5% to 1.5% above standard bank rates. This is where professional advocacy becomes essential. We specialise in finding the bridge between a rigid bank "no" and a structured approval that keeps your 2026 portfolio on track.

A Step-by-Step Template to Forecast Your Investment Cash Flow

While an investment property mortgage calculator nz provides a quick answer, knowing the manual steps behind the math gives you true control over your strategy. It allows you to spot a bad deal before you ever talk to a bank. Follow this template to organise your forecast for any 2026 acquisition.

-

Step 1: Determine the total entry cost. Start with the purchase price and add an allowance for legal fees, building inspections, and valuations. These often total between $3,000 and $6,000 depending on the property’s complexity.

-

Step 2: Establish your loan requirement. Subtract your cash deposit or the usable equity you’ve unlocked from your home. This leaves you with the core debt figure.

-

Step 3: Select your structure. Decide if you’ll use an interest-only period to maximise immediate cash flow or start with principal and interest to build equity from day one.

-

Step 4: Use realistic rates. Don’t just use the lowest rate on the market. Apply a standard 2026 fixed rate, such as the 5.19% two-year average, to keep your figures grounded in reality.

-

Step 5: Run the serviceability check. Calculate your monthly repayment and compare it against 80% of your projected gross rent. If the rent doesn’t cover the mortgage at this "shaded" level, you’ll need to contribute from your personal income.

If these steps feel overwhelming or the numbers aren’t quite stacking up, we can help you find a path forward. Our team specialises in securing residential investment property loans that align with your long-term wealth goals.

The ‘Stress Test’ Calculation

Bank managers don’t look at what you can pay today; they look at what you can pay if the market shifts. You should do the same. Recalculate your repayments with an interest rate that is 1% or 2% higher than current offers. This "worst-case" figure is the most vital number in your entire spreadsheet because it defines your safety margin. A robust investment plan should survive a 2% interest rate hike without requiring external capital. If your portfolio can’t weather that storm, it might be time to reconsider the purchase price or your deposit size. Understanding the difference between fixed rate mortgage vs floating rate options is essential when stress testing your portfolio against potential rate movements.

Accounting for the ‘Hidden’ Costs

Many novice investors make the mistake of thinking the mortgage is their only expense. In reality, rates, insurance, and property management fees usually consume about 20% of your gross rental income. These are the "forgotten" costs that can turn a cash-flow positive property into a monthly liability. When you’re using an investment property mortgage calculator nz, always deduct these outgoings from your rental income before comparing it to your loan repayments. Remember that "set and forget" is a myth in property investment. Staying on top of these shifting costs ensures your portfolio remains a source of wealth rather than a source of stress.

Beyond the Calculator: How Tailored Financing Secures Your Portfolio

While an investment property mortgage calculator nz provides the essential coordinates for your journey, it cannot navigate the roadblocks that often appear during a bank’s assessment process. Think of the calculator as your map; it shows you the destination, but a seasoned advocate acts as your guide through the terrain. At Mortgage Suite Ltd, we specialise in residential investment property loans that don’t always fit the rigid, automated criteria of the "Big Four" banks. We understand that your financial story is more than just a credit score or a debt-to-income ratio.

Securing a "fair go" from lenders in 2026 requires more than just submitting an application. It involves presenting a case that highlights the strength of your strategy. For many investors, 2nd tier lending serves as a strategic bridge. It allows you to secure a property and build equity today, rather than waiting for mainstream banks to ease their restrictions. This proactive approach turns a potential "no" into a structured path toward long-term wealth, ensuring you don’t miss out on opportunities while waiting for the perfect market conditions.

The Power of a Specialised Advocate

Krish Krishna brings over two decades of banking experience to your corner, ensuring your application is seen by human eyes rather than just an algorithm. There is a profound difference between a "computer says no" interaction at a local branch and a solution brokered through deep institutional knowledge. When your finances are non-standard or your portfolio is complex, personal connection and a reputation for integrity matter. We act as your dedicated negotiator, removing obstacles and finding the bridge between institutional requirements and your personal goals. Our experience allows us to anticipate lender objections before they arise, saving you time and reducing the stress of the approval process.

Next Steps: From Calculation to Pre-Approval

To move from a theoretical calculation to a formal pre-approval, you’ll need to organise your documentation. This typically includes recent payslips, bank statements, and rental appraisals for your existing or prospective properties. Having these ready allows for a much smoother transition from the research phase to the acquisition phase. We also recommend a "health check" on your current portfolio equity to ensure you are leveraging your assets as efficiently as possible. When you’re ready to turn your data into a concrete offer, organise a consultation with Mortgage Suite Ltd to find the right loan for your next investment. We are here to ensure your 2026 strategy is built on a foundation of professional certainty and personalised care.

Mastering Your Path to Property Success

Mastering the numbers is the first step toward building a resilient property portfolio. By now, you understand that an investment property mortgage calculator nz is a powerful starting point for assessing yield and cash flow. However, clearing the high bars of DTI limits and LVR restrictions requires more than just a digital tool. It demands a strategic approach that accounts for 2026 market realities and the nuances of non-bank lending. Success in this environment comes from preparing for the transition of interest-only periods and ensuring your strategy can weather potential interest rate shifts with a calculated safety margin.

With over 20 years of banking and brokerage experience, Mortgage Suite Ltd provides the seasoned advocacy needed to turn complex financial scenarios into approvals. We specialise in 2nd tier and non-bank lending, offering a nationwide service for all New Zealand investors who want a steady hand in a fluctuating market. You don’t have to navigate these hurdles alone. Secure your investment future with a tailored mortgage strategy from Mortgage Suite Ltd. We are ready to help you move beyond the spreadsheet and into your next successful acquisition with absolute confidence.

Frequently Asked Questions

How much deposit do I need for an investment property in NZ in 2026?

You generally need a 30% deposit for an existing residential investment property in 2026. This requirement aligns with the Reserve Bank’s LVR restrictions, which limit most investor lending to a 70% threshold. If you are purchasing a new build, you may be able to secure a loan with as little as a 20% deposit. Using an investment property mortgage calculator nz helps you determine the exact amount of cash or equity required to meet these criteria.

Can I use my KiwiSaver to buy an investment property?

No, you cannot withdraw KiwiSaver funds to purchase a property intended solely for investment. KiwiSaver withdrawals are strictly reserved for buying your first home to live in, or for cases of significant financial hardship. However, once you have used KiwiSaver to secure your first home, the equity you build in that property can eventually be leveraged to fund a deposit for a future investment property.

What is a ‘good’ DTI ratio for a property investor?

A healthy DTI ratio for an investor is typically considered to be below six. As of mid-2024, the Reserve Bank implemented a formal DTI cap of seven for most investor lending. If your total debt exceeds seven times your gross annual income, mainstream banks will likely decline your application. Maintaining a lower ratio ensures your portfolio remains resilient and gives you more flexibility when interest rates fluctuate.

Are interest rates higher for investment properties than for my own home?

No Interest rates are generally the same. For investors up to 6 investment properties, you can obtain the rate as normal housing rates. For investors with more than 6 properties, some lenders will view you as commercial investors and may apply a slightly higer rate.

What happens if my investment property is vacant for a month?

If your property is vacant, you must be able to cover the full mortgage repayment from your other income sources. This is why banks "shade" your rental income, often only counting 80% of the projected rent in their serviceability tests. We always recommend keeping a cash buffer equivalent to at least four weeks of rent to manage these inevitable vacancy periods without putting undue stress on your personal finances.

Should I choose a 2nd tier lender if my bank declines my application?

Choosing a 2nd tier lender is a very effective strategy if a mainstream bank declines your application due to rigid DTI or LVR rules. These lenders often provide a vital bridge for investors with complex income structures or those who sit just outside the "Big Four" criteria. While the interest rates may be slightly higher, the flexibility they offer can be the difference between growing your portfolio or stalling your investment journey.

How do I calculate the equity in my current home?

To calculate your usable equity, take 80% of your home’s current market value and subtract your remaining mortgage balance. For example, if your home is worth $1,000,000 and your mortgage is $500,000, your usable equity is $300,000. This is calculated as $800,000 minus $500,000. This figure represents the maximum amount you can potentially borrow against to fund a deposit for a new investment property without needing extra cash.

Is interest-only always better for rental properties?

Interest-only is not always the best choice; it depends on your specific financial goals. Many investors prefer interest-only to maximise tax deductibility and keep monthly outgoings low, which is excellent for immediate cash flow. However, Principal and Interest repayments are better if your goal is to build equity and pay off the debt over a 30-year term. It’s about balancing your immediate flexibility against your long-term debt reduction strategy.