Non-Conforming Home Loans in New Zealand: A 2026 Guide for When the Bank Says No

What if a “no” from your bank wasn’t a dead end, but actually a signpost pointing you toward a more tailored way to buy your home? It’s incredibly disheartening to feel like you’ve failed just because you don’t fit a specific box, especially when you’ve worked hard to build a successful business or establish yourself as a contractor. You’re certainly not alone in feeling frustrated by complex lending rules that seem designed to keep you out of the market. The reality is that mainstream banks often overlook capable borrowers, which is why non-conforming home loans New Zealand have become such a vital tool for Kiwis in 2026.

In this guide, you’ll discover how these flexible loans provide a legitimate pathway to homeownership for those with non-standard income or unique financial backgrounds. We’ll show you how to move past the stress of rejection and build a clear plan to secure a property now, with a view to refinancing later as your situation evolves. You will gain the confidence to stop waiting on the sidelines and start your journey toward owning your own home today.

Key Takeaways

- Understand that “non-conforming” simply means your situation doesn’t fit a standard bank’s checklist, and these loans are fully regulated and safe options.

- See how non-conforming home loans New Zealand provide a vital path forward for self-employed Kiwis or those with minor credit issues.

- Learn how to use a “bridge strategy” to buy your home now and plan for a move back to a mainstream lender in a few years.

- Get the facts on interest rates and fees so you can weigh the cost of the loan against the long-term benefit of getting onto the property ladder.

- Discover how working with a specialist gives you access to lenders who don’t work directly with the public, opening doors that often seem closed.

What exactly is a non-conforming home loan in New Zealand?

Think of the major banks like a high-end tailor who only makes one size of suit. If you happen to be a bit taller or broader than their standard template, you’re out of luck. Mainstream lenders like ANZ or ASB have very rigid checklists. If you miss a single tick, even for something small, they often can’t help you. This is why non-conforming home loans New Zealand have become a vital alternative for many Kiwis whose lives don’t fit a standard spreadsheet.

Essentially, “non-conforming” is just a term for a mortgage that sits outside the traditional lending rules. If you are asking, What is a non-conforming loan?, it’s a financial tool designed for people who are actually great borrowers but have non-standard circumstances. In 2026, the “big four” banks have tightened their belts even further. With debt-to-income ratios capped at 6 and a more cautious approach to self-employed income, more people are finding themselves looking for these alternative options.

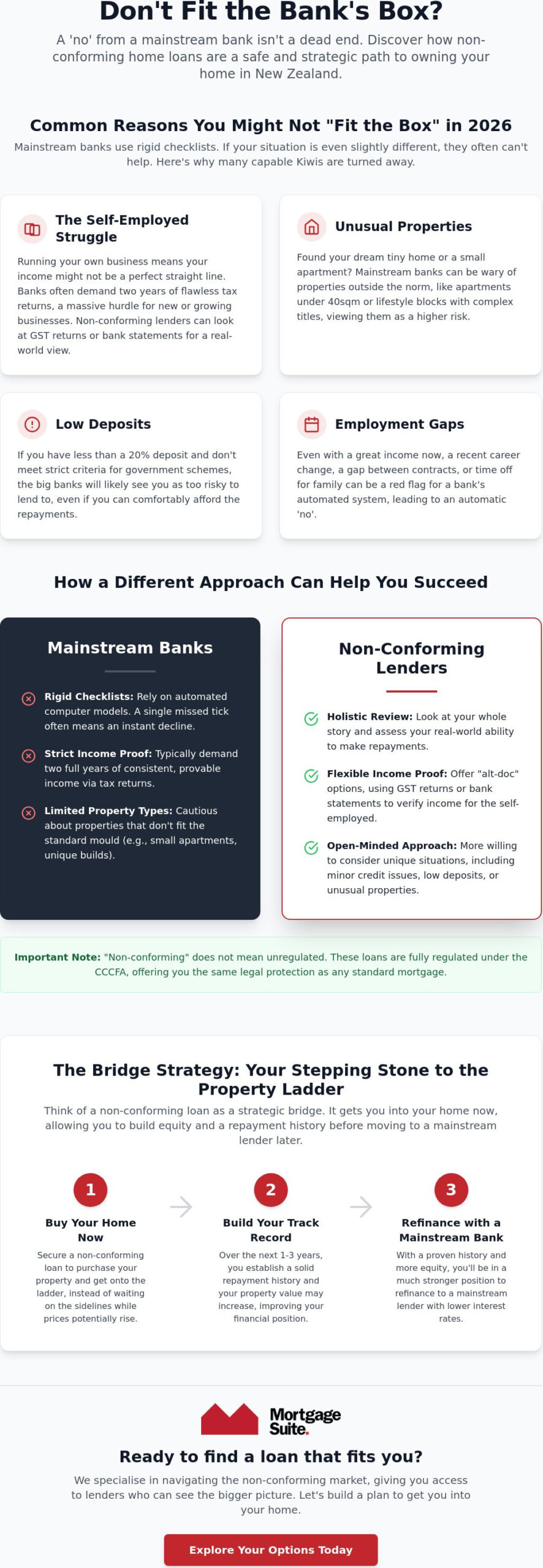

It’s important to understand that these aren’t “shadowy” or unregulated products. They are perfectly legal and must comply with the Credit Contracts and Consumer Finance Act (CCCFA). You get the same level of legal protection as you would with any other mortgage. The main difference is that these lenders are willing to look at your whole story, not just the last three months of your bank statements.

The difference between “Non-Bank” and “Non-Conforming”

Many people use these terms interchangeably, but they mean different things. A “non-bank” is the type of institution, it’s a lender that isn’t a traditional registered bank. “Non-conforming” describes the type of loan criteria being used. Non-conforming loans are flexible financial solutions designed for people whose income or credit history doesn’t match the rigid templates used by traditional banks. You might even find that a non-bank lender is the best fit even if you have a perfect credit score, simply because they can be more creative with how they structure your debt.

Who are the 2nd tier lenders in NZ?

In the New Zealand market, 2nd tier lender New Zealand options include building societies, credit unions, and specialist finance companies. They are often funded by wholesale investment markets rather than customer deposits, which gives them the freedom to be more flexible with their approvals. While they have more room to say “yes,” they are still committed to responsible lending. They want to ensure you can comfortably manage your repayments, making non-conforming home loans New Zealand a safe and strategic way to enter the property market when the big banks won’t budge.

Common reasons you might not “fit the box” in 2026

It feels personal when a bank says no. You’ve worked hard, saved your deposit, and found a place you love, only to be told you don’t meet a specific requirement. Often, a rejection isn’t about your ability to pay back a loan. It’s usually because your life doesn’t align with the rigid computer models the big banks use. Since the introduction of tighter lending rules, many Kiwis have been declined for things as small as their personal spending habits or the type of house they want to buy. This is where non-conforming home loans New Zealand provide a much-needed alternative.

There are several common reasons why a mainstream bank might turn you away in 2026:

- Unusual Properties: Banks are often wary of tiny homes, apartments smaller than 40sqm, or lifestyle blocks with complex titles.

- Low Deposits: If you have less than a 20% deposit and don’t qualify for specific government grants, the “big four” might see you as too high a risk.

- Employment Gaps: Even if you’re earning well now, a recent career change or a few months between jobs can trigger a “no” from traditional lenders.

The self-employed struggle

If you run your own business, you know that profit isn’t always a straight line. Banks usually demand two full years of perfect tax returns to prove your income. This requirement is a massive hurdle for new business owners or those who have recently scaled up. Many 2nd tier lenders offer “alt-doc” options instead. This means they can look at your GST returns or recent bank statements to get a real-world picture of what you can afford. If you’re a contractor or freelancer, your income is valid, and we can help you find a lender who understands your business model.

Credit history: It’s not always a deal-breaker

A forgotten power bill from three years ago or a past default shouldn’t end your home-buying dreams forever. Mainstream banks tend to see any credit “blip” as a major red flag. In contrast, 2nd tier lenders are often willing to listen to the story behind the numbers. They look at why a default happened and what you’ve done since then to stay on track. Many non-conforming home loans New Zealand are actually designed to help you repair your credit over time, acting as a bridge until you’re ready to switch back to a standard bank. It’s about looking at your future potential, not just your past mistakes.

Mainstream Banks vs. Non-Conforming Lenders: A fair comparison

When you compare mainstream banks to alternative lenders, it’s a bit like comparing a mass-market retail chain to a specialist consultant. The big banks have the lowest rates, but they also have the least flexibility. If you don’t fit their specific mould, the low rate doesn’t actually help you because you can’t get the loan. This is where non-conforming home loans New Zealand come into play. They fill the gap for people who have the income and the drive to own a home but fall outside the standard banking criteria.

Let’s look at the numbers. In June 2026, mainstream bank fixed rates are sitting around 4.65% to 4.79%. In contrast, rates for non-conforming home loans New Zealand are higher because they are risk-based. You should also expect establishment fees to be more significant than what you’d find at a big bank. While the upfront cost is higher, the value lies in getting an approval when everyone else has said no. These lenders look at the common sense of a deal rather than just following a rigid computer algorithm.

Speed is another area where alternative lenders often shine. When you’re trying to secure a property at auction, you don’t have weeks to wait for a bank’s head office to review your file. Because 2nd tier lenders have shorter chains of command, they can often provide a firm answer in a fraction of the time. This agility allows you to bid with confidence, knowing your finance is already sorted and you won’t miss out on the right property.

Understanding the “Risk Premium”

Lenders charge a higher rate because they are taking a chance on a borrower that a big bank won’t touch. We call this a risk premium. While the interest is higher, it’s often a better financial move than waiting three years to save a larger deposit. If house prices rise during that time, the cost of waiting can easily exceed the extra interest you’d pay now. Many of these loans also allow you to step down to a lower rate once you’ve proven your reliability over a year or two.

Flexibility in lending criteria

Alternative lenders look at your situation with a human eye. For instance, they might be more generous with their Loan-to-Value Ratio (LVR), allowing you to borrow more against the property’s value than a traditional bank would. They also look at your income differently, often counting more of your overtime, commissions, or bonuses. You can learn more about these differences in our non-bank lenders NZ guide. If you have a smaller deposit, you might also want to check if you qualify for the First Home Loan scheme, which helps people who don’t fit the standard 20% deposit box.

The Bridge Strategy: Using a non-conforming loan as a stepping stone

Too many people view these mortgages as a final destination or a “last resort.” In reality, they are a powerful tool to get you across the gap between where you are now and where the bank wants you to be. This is what we call the Bridge Strategy. It’s a deliberate 2-to-3-year plan designed to get you into the property market today, rather than sitting on the sidelines for years while house prices potentially climb. By choosing non-conforming home loans New Zealand, you aren’t just getting a mortgage; you’re buying time to fix the very things that caused the bank to say no in the first place.

While you are on this bridge, your home is hopefully growing in value. Every repayment you make reduces your debt, and every month that passes helps “clean up” your financial profile. This is the time to perfect your tax returns if you’re self-employed or ensure your credit history is spotless. The goal is simple: stay with an alternative lender for a few years, build your equity, and then refinance back to a mainstream bank for those lower rates once you finally “conform” to their rules.

Step 1: Get in the door

The biggest mistake many Kiwis make is waiting for the “perfect” time to buy. They wait for interest rates to drop or for their deposit to hit exactly 20%. History shows us that time in the market almost always beats timing the market in New Zealand. By securing the property you want today, you start building equity immediately. A non-conforming loan is often a temporary solution to a long-term goal, giving you the leverage to act when the right house appears.

Step 2: Prove your reliability

Once you have the keys, the real work begins. This stage is all about demonstrating to future lenders that you are a low-risk borrower. You need to make every single repayment on time, without exception. This builds a “bank-ready” history that is far more convincing than any spreadsheet or letter of explanation. If you’re just starting out, our guide on home loans for first home buyers New Zealand can help you map out these early steps. We keep a close eye on your progress and can tell you exactly when your profile is strong enough to make the move back to a mainstream lender. If you’re ready to start building your own bridge, talk to our team about your options today.

How Mortgage Suite navigates the non-conforming market for you

Getting a “no” from a bank can feel like a personal rejection, but at Mortgage Suite Ltd, we see it as the start of a more tailored conversation. With Krish Krishna’s 20 plus years of banking experience, we know exactly how the “other side” thinks. We understand the hidden levers that mainstream lenders pull and, more importantly, we know how to present your case to the lenders who are actually willing to listen. Securing non-conforming home loans New Zealand requires more than just filling out a form; it requires a dedicated advocate who can translate your financial life into a compelling story.

We have established deep relationships with 2nd tier lender New Zealand options that simply don’t deal directly with the public. These institutions rely on trusted brokers to bring them quality borrowers who just happen to have non-standard situations. Because we’ve spent decades in the industry, our reputation carries weight. When we tell a lender that a client is reliable despite a past credit blip or a complex business structure, they listen. We handle all the paperwork and the tough conversations, removing the stress so you can focus on moving into your new home.

Tailored solutions, not “cookie-cutter” loans

Every person who walks through our door has a unique story. We don’t believe in one-size-fits-all mortgages. We take the time to sit down and truly listen to your situation before we even think about suggesting a lender. This personal connection is what sets us apart from the automated systems at the big banks. By specialising in loans that don’t fit the standard box, we can identify opportunities that others might miss. Whether you’re a new business owner or a contractor, we ensure your non-conforming home loans New Zealand are as unique as your circumstances.

Your partner for the long haul

Our job doesn’t end when you get your home loan. We are your partners for the entire journey. As we discussed earlier regarding the exit strategy, the goal is often to move back to a mainstream bank eventually. Mortgage Suite Ltd stays in touch and helps you plan that transition, ensuring you’re always on the best possible path. You’ll get friendly, jargon-free advice that treats you like a priority, not just another number in a database. Ready for a fair go? Get in touch with Mortgage Suite Ltd today.

Take the next step toward your new home

A bank rejection doesn’t have to be the end of your property dreams. As we’ve explored, non-conforming home loans New Zealand serve as a strategic bridge, allowing you to secure a property now while you work toward a mainstream mortgage. By focusing on building equity and proving your reliability, you can turn a temporary setback into a long-term win.

At Mortgage Suite Ltd, our team brings over 20 years of banking and brokerage experience to your corner. We specialise in alternative lending and act as your dedicated advocate, ensuring your story is heard by lenders who value common sense over rigid checklists. We don’t just process applications; we build partnerships focused on your success.

Book a conversational chat with Krish to explore your options and see how we can help you move forward with confidence. You deserve a fair go at owning your own home, and we’re here to help you make it happen.

Frequently Asked Questions

Are non-conforming home loans safe in New Zealand?

Yes, these loans are perfectly safe and must comply with the Credit Contracts and Consumer Finance Act (CCCFA) just like any big bank mortgage. This means you have the same legal protections and rights as any other borrower in New Zealand. These lenders are professional financial institutions that are simply more flexible with their rules than the household names you see on the high street.

How much higher are the interest rates for non-conforming loans?

Rates are typically higher than mainstream bank offers because the lender is taking on a situation that the big banks won’t touch. While a major bank might offer a rate under 5% in 2026, alternative lenders often range between 10% and 14.5% depending on your specific profile and risk level. It’s best to view this extra cost as a temporary fee for getting into the property market now rather than waiting years.

Can I get a non-conforming loan if I am self-employed with only one year of accounts?

Yes, you can often secure a loan with just one year of accounts by using alternative documentation like bank statements or GST returns. Mainstream banks usually demand two full years of perfect tax returns, but 2nd tier lenders specialise in helping new business owners who are already turning a good profit. This flexibility allows you to buy your home now rather than waiting for another financial year to pass.

What is the minimum deposit for a non-conforming home loan?

Most alternative lenders look for a deposit of at least 20%, though some may consider 10% depending on the property type and your overall income. Because these lenders aren’t always bound by the same strict speed limits as the big banks, they have more room to move on deposit requirements. We can look at your specific savings and income to see which lender’s rules fit your current situation.

How long does it take to get approval for a 2nd tier loan?

Approval for 2nd tier loans is often much faster than the big banks, sometimes taking only two to three working days once all your paperwork is submitted. These lenders have smaller teams and less red tape, which makes them an excellent option if you need to move quickly for an auction or a short settlement. Having your bank statements and ID ready to go is the best way to speed up the process even further.

Can I move back to a big bank later if I start with a non-conforming loan?

Yes, moving back to a mainstream bank is the ultimate goal for most people who start with non-conforming home loans New Zealand. Once you have built up some equity and established a clean repayment history over two or three years, your profile becomes much more attractive to traditional lenders. We specialise in helping you plan this transition so you can eventually secure those lower mainstream rates when you are ready.

What happens if I have a default on my credit record?

A credit default isn’t an automatic “no” with alternative lenders, as they are more interested in the story behind the issue than just the score itself. They will want to see that the debt has been settled and that you’ve been reliable with your other payments since that time. We help you explain these past blips to the lender so they can see your current financial strength and future potential.

Do I need a mortgage broker to access non-conforming lenders?

Yes, many 2nd tier and specialist lenders in New Zealand do not deal directly with the general public and only accept applications through accredited mortgage brokers. Working with a broker also ensures your application is presented in the best possible light to the right people. We know which lenders are currently active and which ones are most likely to say “yes” to your specific needs and financial background.