Self-Employed Home Loan NZ: The 2026 Guide to Getting Approved

Imagine sitting across from a bank manager, presenting a thriving business you have built from the ground up, only to be told your “paper income” isn’t enough to buy a house. It is incredibly disheartening when mainstream lenders ignore your legitimate business add-backs or penalise you for the very expenses your accountant organised to reduce your tax bill. If you are searching for a self employed home loan nz, you have likely realised that traditional banks often view your entrepreneurial drive as a risk. They see inconsistent income “bursts” and mountains of paperwork, while we see a dedicated professional who deserves a steady hand to guide them through the finance process.

This 2026 guide provides the clear path to pre-approval you need, even with the Official Cash Rate at 2.25% and debt-to-income ratios capped at six times your earnings. You will learn exactly how to bypass rigid bank criteria by exploring non-bank lenders who offer flexible “alt-doc” solutions using GST returns or business bank statements. We will detail how to secure competitive interest rates and navigate the latest LVR restrictions, ensuring your business structure is properly understood so you can move forward with confidence.

Key Takeaways

- Understand how lenders apply “safety margins” to your income and how to navigate the 2026 Debt-to-Income (DTI) restrictions.

- Discover the documentation hierarchy and why alternative “Alt-Doc” methods like GST returns might be the key to proving your true earning power.

- Learn why 2nd Tier lenders are a strategic choice for a self employed home loan nz rather than a last resort when mainstream banks decline your application.

- Master a simple “pre-audit” process to organise your business drawings and personal expenses for maximum lender appeal.

- Explore how professional advocacy and veteran negotiation can translate your complex business structure into a clear path for approval.

The Reality of Self-Employed Home Loans in NZ for 2026

For many business owners, the dream of home ownership feels like it is being held hostage by a spreadsheet. Getting a self employed home loan nz in 2026 requires more than just a profitable business; it requires a deep understanding of how lenders interpret your financial health. While an employee with a standard salary provides a predictable data point for a bank, your income is often viewed through a lens of skepticism. Mainstream banks are currently operating with a conservative risk appetite, and they often struggle to reconcile the fluctuations of a growing business with their rigid lending criteria.

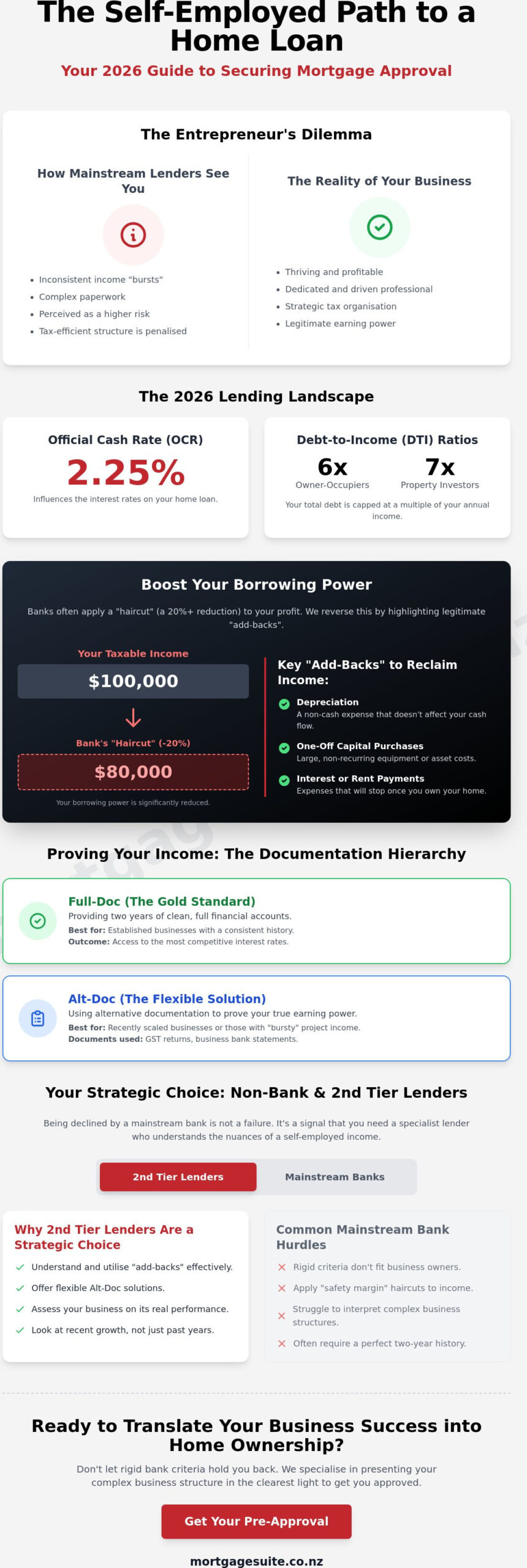

The lending environment in mid-2026 is heavily influenced by the Debt-to-Income (DTI) restrictions that became a permanent fixture in recent years. For owner-occupiers, the limit is generally six times your gross annual income, while investors are capped at seven times. When defining self-employment for a loan application, the bank does not just look at your turnover. They look at your drawings, your net profit, and your ability to service debt when the Official Cash Rate (OCR) is at 2.25%. If your income arrives in “bursts” rather than a steady drip, a traditional bank might simply put you in the “too hard” basket. However, being declined by a major bank is rarely the end of the road; it is often just the signal that you need a more sophisticated lending partner.

Understanding the Bank “Haircut” on Your Income

Banks are notoriously cautious with business owners. Even if you have had a record-breaking financial year, lenders will often apply a “haircut” or a safety margin to your reported income. This typically involves shading your gross profit by 20% or more to account for potential business volatility. This creates a frustrating paradox: your accountant works hard to organise your finances and minimise your taxable profit, but this very strategy can slash your borrowing power when you apply for a self employed home loan nz.

To overcome this, we focus on “add-backs.” These are legitimate business expenses that don’t actually impact your ability to pay a mortgage, such as:

- One-off capital purchases or equipment upgrades.

- Non-cash expenses like depreciation.

- Excessive home office claims or personal expenses run through the business.

- Rent or interest payments that will cease once you buy your own property.

Regulatory Changes and DTI Ratios in 2026

The 2026 regulatory framework treats business debt and personal debt with equal scrutiny. Under the current Credit Contracts and Consumer Finance Act (CCCFA) requirements, lenders must be certain that your business debt—such as vehicle finance or an overdraft—does not compromise your home loan repayments. If your business carries significant debt, it can quickly eat into your DTI allowance, making it harder to reach the 80% LVR threshold required for standard owner-occupier loans. We work with you to clean up your debt profile, ensuring your personal and business liabilities are structured to maximise your approval chances without sacrificing your business’s cash flow.

Proving Your Income: Documentation That Actually Works

Securing a self employed home loan nz requires a strategic approach to your paperwork. While an employee simply hands over three months of payslips, your application must build a narrative of stability and growth. Many business owners find that their IRD Summary of Earnings tells a story of tax efficiency rather than true mortgage affordability. To bridge this gap, we look beyond the basic tax return to find the documents that reflect your business’s actual momentum.

The hierarchy of proof has shifted significantly in 2026. Traditional “Low-Doc” loans, which once required minimal evidence, have largely been replaced by “Alt-Doc” (alternative documentation) solutions. This is a direct result of the Credit Contracts and Consumer Finance Act (CCCFA), which mandates a robust assessment of affordability. If you have two years of clean financial accounts, you’ll likely qualify for “Full-Doc” rates. However, if your business has recently scaled or you have “bursty” income from project-based contracts, Alt-Doc allows us to use more recent data, such as GST returns, to prove you can comfortably service the debt.

The Essential Self-Employed Paperwork Checklist

Lenders want to see that your business is a reliable vehicle for income. Before submitting an application, ensure you have the following documents organised:

- Financial Statements: Full Profit & Loss and Balance Sheets for the last two financial years.

- Bank Statements: Six months of personal and business statements. Lenders look for regular drawings that match your stated income.

- Tax Verification: Your most recent personal and business tax assessments, along with proof that all IRD obligations are being met.

- Add-back Schedule: A clear list of non-cash or one-off expenses that shouldn’t count against your borrowing power.

If your business income is seasonal, we frame your application by showing a 12-month average rather than focusing on a quiet month. This context is vital for preventing a “decline” based on a temporary dip in cash flow. If you are unsure which documents best represent your current position, exploring tailored home loan options can help clarify your strategy before you approach a lender.

Alt-Doc Solutions for Newer Businesses

For those who have been trading for 12 to 18 months, or whose most recent tax return doesn’t reflect a recent surge in turnover, Alt-Doc is a game changer. Instead of waiting for the next financial year to end, some specialist lenders will accept an accountant’s declaration of your earnings or use your last six months of GST returns to verify your current capacity. This approach focuses on where your business is today, not where it was two years ago, providing a vital pathway for self employed home loan nz applicants who are currently in a high-growth phase.

Navigating Non-Bank and 2nd Tier Lending Solutions

Many business owners view 2nd tier lenders with a sense of hesitation, fearing they are only for those with significant financial trouble. This is a misconception that often prevents entrepreneurs from securing a self employed home loan nz when they are perfectly capable of servicing a mortgage. In the current 2026 market, non-bank lenders like Avanti Finance or Pepper Money act as sophisticated specialists. They fill the gap left by mainstream banks that rely on rigid automated systems. While a bank might see a complex trust structure or a single year of trading as a red flag, a 2nd tier lender employs human underwriters who look at the bigger picture.

The primary trade-off involves cost. Non-bank “Near Prime” rates typically start around 6.35% to 7.35%, which is higher than the special rates offered by ANZ or Westpac. You should also expect higher establishment fees, often ranging between $2,000 and $5,000. However, for a business owner, the value lies in the approval probability. These lenders aren’t bound by the Reserve Bank’s strict Debt-to-Income (DTI) thresholds in the same way as registered banks. This flexibility allows us to secure a self employed home loan nz for clients who have the cash flow but don’t fit the traditional “box.”

When to Choose a Non-Bank Lender

Choosing a non-bank option is often the most strategic move if your business has undergone a recent transition. If you have moved from a sole trader to a company structure, or if a one-off capital investment skewed your net profit last year, traditional bank software will likely trigger an automatic decline. Specialist lenders are far more accommodating of short trading histories, sometimes considering applications with as little as 6 to 12 months of data if you have a strong industry background. They specialise in “Alt-Doc” solutions, allowing us to use recent GST returns to prove your current earning capacity rather than relying on outdated tax returns.

The Long-Term Strategy: Refinancing Back to a Bank

We often treat a 2nd tier loan as a temporary bridge rather than a forever home for your mortgage. By securing a loan now and maintaining a clean repayment history for 12 to 24 months, you “prime” yourself for a future bank application. This period allows your business to mature on paper and demonstrates your reliability as a borrower. Understanding how to qualify for a home loan in NZ involves planning this exit strategy from the start. Once your financial statements show two years of solid growth, we can assist you in refinancing back to a mainstream bank at a lower interest rate, having already secured the property you wanted.

A Step-by-Step Guide to Polishing Your Mortgage Application

Successful lending outcomes are rarely the result of luck. They are the product of a disciplined staging process that begins months before you even attend an open home. When you apply for a self employed home loan nz, the bank isn’t just looking for profitability; they are searching for evidence of financial discipline. Think of your application like a house you are preparing for sale. You need to declutter the noise, fix the small leaks in your spending, and highlight the structural strengths of your business.

The first step is a rigorous pre-audit. Scour your business accounts for personal expenses that might look like high living costs to a lender. Second, ensure your drawings are regular. A bank prefers to see $1,500 transferred every week rather than a $20,000 lump sum once a quarter. Third, slash your credit limits. In the 2026 DTI environment, an unused $10,000 credit card or an active Buy Now, Pay Later (BNPL) account can reduce your borrowing power by tens of thousands of dollars. Finally, prepare a formal business commentary and engage a specialist who understands the nuances of business structures.

Framing Your Business Narrative

Lenders hate mystery. If your profit dipped recently because you invested in a new fleet of vehicles or a high-end server array, you must tell them. A written explanation transforms a “loss” on paper into a strategic investment in future growth. Highlight recurring revenue models or long-term contracts that prove your income isn’t just a series of lucky breaks. If you are a contractor in a niche field like IT or engineering, including a professional CV helps the underwriter understand your employability if your current contract ends. This narrative provides the context that raw numbers often lack.

Cleaning Up Your Personal Financial Conduct

You must adhere to the “three-month rule” of flawless account behaviour. Under the CCCFA, any unarranged overdraft or missed payment on a utility bill is a massive red flag. Banks interpret these as a lack of financial control, regardless of how much money is sitting in your business account. You also need a clear “deposit story.” Be ready to prove exactly where your savings came from to satisfy Anti-Money Laundering (AML) requirements. If your deposit includes a gift from family or a business dividend, document the paper trail early. To ensure your application is truly bank-ready, you can apply for a home loan assessment to identify any potential hurdles before they become problems.

Why Mortgage Suite is Your Best Advocate for Approval

When you work for yourself, you don’t just need a loan; you need a dedicated negotiator who understands the intricacies of your business. Securing a self employed home loan nz is often a battle of interpretation. It’s about how your depreciation is viewed, how your “bursty” income is averaged, and how your future potential is weighed against historical tax returns. We provide the steady hand and the institutional knowledge required to bridge the gap between your entrepreneurial success and the rigid requirements of a bank’s credit department.

Our reach extends beyond the big four banks. We provide access to a comprehensive range of 2nd tier and alternative capital, allowing us to find solutions even when traditional lenders have said no. Our partnership approach includes:

- Access to residential investment property loans and business finance.

- Strategic planning to move from 2nd tier loans back to mainstream banks.

- Proactive management of commercial and property development loans.

- Expert structuring for first-home buyers with non-standard income.

The Advantage of a Seasoned Negotiator

Krish Krishna brings over 20 years of banking experience to your side of the table. This isn’t about simply submitting a form; it’s about expert negotiation. Krish uses his deep understanding of credit policy to challenge rejections and present your financial story in a way that resonates with underwriters. We specialise in structuring complex deals that mainstream banks often overlook, ensuring your business structure is viewed as a strength rather than a liability. You aren’t just another file to us; you are a partner whose success is our priority.

We understand that as a business owner, your time is your most valuable asset. By utilising our veteran expertise, you gain an advocate who knows exactly which “add-backs” to fight for and which lenders have the highest risk appetite for your specific industry. This high-standard service is designed to remove obstacles and create a seamless bridge to your property goals.

Ready to Get Moving?

We simplify the process so you can stay focused on running your business. Instead of you spending hours chasing paperwork and deciphering banking jargon, we handle the heavy lifting. The first steps involve a consultative conversation where we identify your needs and outline a clear path to pre-approval. There is no need to feel overwhelmed by the volume of paperwork when you have a veteran expert managing the details. Enquire about your self-employed home loan today and take the first step toward a successful approval.

Your Path to Home Ownership Starts Here

Securing a self employed home loan nz in 2026 doesn’t have to be a source of constant anxiety. While the DTI restrictions and rigid bank criteria create hurdles, they are far from insurmountable when you have the right documentation and a strategic narrative. Whether you are using Alt-Doc solutions to prove your recent momentum or utilising a 2nd tier lender as a tactical stepping stone, the goal remains the same: securing a home that reflects your hard work.

At Mortgage Suite, we leverage over two decades of banking and lending expertise to ensure your business structure is understood, not just processed. We specialise in 2nd tier loans that mainstream banks often decline, providing a tailored, NZ-wide service for business owners and contractors alike. You have built your business with passion and discipline; we are here to apply that same dedication to your mortgage approval.

If you are ready to move past the frustration of bank rejections, book a consultation with our self-employed lending specialists today. Let us turn your complex financial profile into a clear path forward. Your entrepreneurial journey deserves a partner who values your vision as much as you do.

Frequently Asked Questions

Can I get a home loan if I’ve only been self-employed for one year?

Yes, you can secure a home loan with only one year of trading, though you will likely need to look beyond the major banks. While traditional lenders typically require two years of financial statements, many specialist lenders offer “Alt-Doc” solutions for those with 12 months of history. These lenders focus on your recent GST returns and industry background to assess your current earning capacity properly.

How much deposit do I need as a self-employed borrower in NZ?

Most self-employed borrowers need a 20% deposit for an owner-occupied property or 30% for an investment. If you are a first-home buyer, you may qualify for the Kāinga Ora First Home Loan, which allows for a deposit as low as 5%. Having a larger deposit often helps offset the perceived risk of variable income and can lead to more competitive interest rates from mainstream lenders.

Will my interest rate be higher because I work for myself?

Your interest rate won’t necessarily be higher if you meet the standard lending criteria of a mainstream bank. However, if you require a specialist or 2nd tier lender due to a short trading history or complex accounts, you should expect a margin above standard bank rates. These “Near Prime” rates often start from 6.35% and serve as a strategic bridge until you can refinance to a major bank.

What are “add-backs” and how do they help my mortgage application?

Add-backs are legitimate business expenses that we “add back” to your net profit to demonstrate your true mortgage repayment capacity. Common examples include depreciation, one-off equipment purchases, or interest on loans that will be repaid. By identifying these non-cash or non-recurring costs, we can significantly increase the income figure used for your self employed home loan nz application and improve your approval chances.

Can I use my KiwiSaver for a deposit if I am self-employed?

Yes, you can certainly use your KiwiSaver for a deposit, provided you have been a member for at least three years and are purchasing your first home. Being self-employed does not change your eligibility for a first-home withdrawal. It is essential to request your withdrawal pack early to ensure the funds are ready for settlement, especially if your business income fluctuates and documentation takes longer to organise.

What happens if my latest tax return shows a low profit due to expenses?

If your latest tax return shows a low profit due to high business expenses, we can often use alternative documentation to prove your actual income. Specialist lenders may look at your last six months of GST returns or bank statements to see your current cash flow. This approach helps bypass the “paper loss” created by tax-minimisation strategies, allowing your true earning power to be recognised by the lender.

Do I need a clean credit history to get a self-employed home loan?

You don’t necessarily need a perfect credit history to get approved for a self employed home loan nz. While mainstream banks are very strict about missed payments or defaults, 2nd tier lenders are more flexible and will often listen to the story behind a credit impairment. A clean record for the last 12 months is usually sufficient to access a wide range of alternative lending options that banks often overlook.

How do DTI ratios affect my ability to borrow for a home?

Debt-to-Income (DTI) ratios limit your total borrowing to a multiple of your gross annual income, typically set at six times for owner-occupiers. For business owners, this means your personal and business debts are weighed against your verified drawings and profit. If your DTI is too high for a major bank, we can often find non-bank solutions that aren’t bound by these specific Reserve Bank restrictions in 2026.