Fixed Rate Mortgage vs Floating: Which is Right for You in 2026?

If you could lock in your financial peace of mind today, would you choose the long term security of a five year fix or the short term flexibility of a one year rate? It is a question that keeps many Kiwis awake at night, especially when you are deciding if a fixed rate mortgage is the right tool to shield your home from rising costs. You likely want a plan that lets you sleep easy, knowing your budget is protected from the whims of the market without being trapped in a structure that does not suit your family’s future.

We understand the stress that comes with bank rejections or the confusion of choosing between various terms while rates fluctuate. This guide will show you exactly how these loans work in the 2026 New Zealand market and help you find the best strategy to protect your wallet. We will explore how to organise your debt to lower your monthly repayments and why “splitting the difference” might be the smartest move for your lifestyle and your long term goals.

Key Takeaways

- Understand how a fixed rate mortgage provides repayment certainty, ensuring your budget stays steady regardless of what the Reserve Bank decides.

- Compare the high security of fixed terms against the flexibility of floating rates to decide which priority fits your current lifestyle.

- Discover the “sweet spot” for loan terms that balances the hope of lower future rates with the need for immediate financial protection.

- Learn how to use a split loan strategy to get the best of both worlds, keeping most of your debt safe while leaving room for extra repayments.

- Find out how an expert can help you access a wider range of lenders if the main banks are not a good fit for your situation.

What is a Fixed Rate Mortgage and How Does it Work?

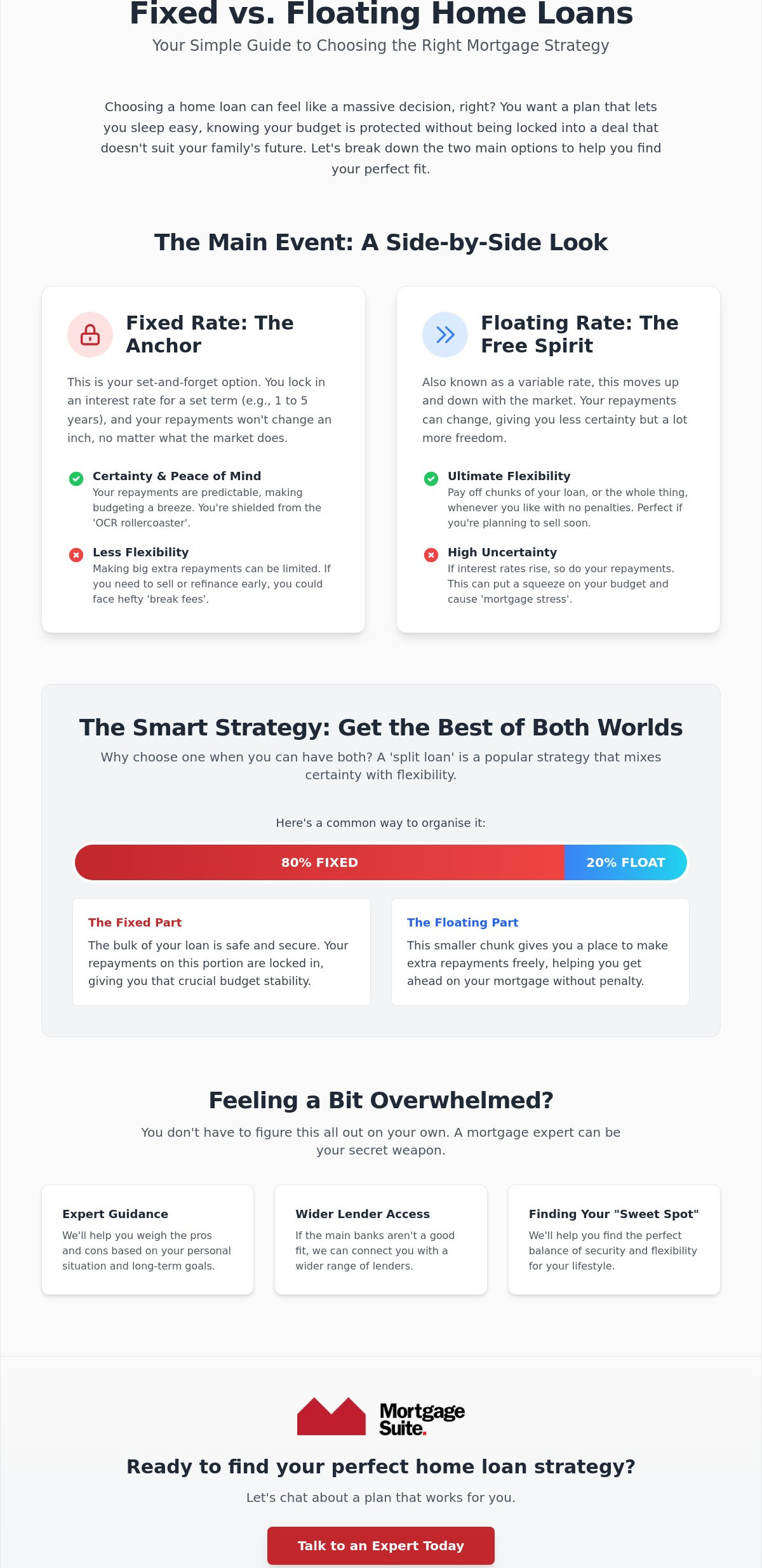

A fixed rate mortgage is a contract for financial certainty during market fluctuations. It is an agreement where you lock in your interest rate for a specific period, usually ranging from six months to five years. This agreement acts as a vital anchor for your finances, providing a sense of stability even when the wider economy feels a bit shaky. If you are looking for a formal deep dive into the history and mechanics of these loans, you can read more about What is a Fixed-Rate Mortgage? on Wikipedia. It is a straightforward way to ensure that your home loan remains manageable, no matter what happens in the global financial world.

When you choose to fix, your monthly repayments stay exactly the same for the duration of that term. It doesn’t matter if the Reserve Bank of New Zealand decides to hike the Official Cash Rate (OCR) or if global markets take a sudden turn; your bank cannot touch your rate until your fixed term expires. This creates a powerful shield against sudden cost-of-living spikes. It means you won’t be blindsided by a sudden increase in your mortgage bill just because interest rates rose while you were busy with work and family life. You can plan your household budget months or even years in advance with absolute confidence.

The difference between fixed and floating

Think of the difference like choosing between a set-menu meal and ordering a-la-carte. A fixed rate mortgage is your set menu; you know exactly what it costs before you sit down, and there are no surprises when the bill arrives. A floating (or variable) rate is like ordering a-la-carte. The price can change depending on the day’s market conditions. While floating rates offer the flexibility to make large extra payments or pay off the loan early without any penalties, they often come with a higher interest rate. Most people find that the lower interest rates typically offered by a fixed rate are worth the trade-off in flexibility.

Why Kiwis usually prefer to fix

Historically, New Zealanders have a strong preference for fixing their loans. Most of us value that budgeting security above all else. It is a practical way to avoid “mortgage stress” when interest rates are climbing. For many, especially those just starting out, understanding these options is just as important as knowing the home loan deposit requirements NZ lenders expect for first-time buyers. By locking in a rate, families can ensure their biggest monthly expense is predictable. This stability is often the difference between a comfortable lifestyle and a stressful one, especially during those early years of home ownership when every dollar counts.

Fixed vs Floating: A Side-by-Side Comparison

Deciding between a fixed or floating rate isn’t just a financial choice; it’s a lifestyle one. When you opt for a fixed rate mortgage, your “certainty factor” is at its peak. You can organise your monthly budget with total confidence, knowing your repayments won’t budge for years. On the flip side, floating rates offer very low certainty but high flexibility. If you’re the kind of person who values freedom over a strict plan, the differences between a fixed-rate and adjustable-rate mortgage (which is what we call floating rates here) are worth a closer look.

Cost is another big player in this decision. In the short term, fixed rates are usually cheaper than floating ones. Banks often offer these lower rates to entice you into a long-term commitment. However, this commitment comes with a catch called “break fees.” If you decide to sell your house or switch lenders before your fixed term ends, your bank might charge you a significant fee to cover their loss. It is a bit like breaking a mobile phone contract early. You need to be sure about your plans before you sign on the dotted line.

The Pros and Cons of Locking it In

The biggest pro is protection from the “OCR rollercoaster” we have seen throughout 2026. With a fixed rate, you’re safe in your own little bubble while the rest of the market reacts to every Reserve Bank announcement. The main con is that you’re stuck. If interest rates drop significantly, you can’t take advantage of those savings without paying those pesky break fees. It’s about weighing up that peace of mind against the potential to save if the market dips. If you’re feeling unsure about which path to take, chatting with a professional about home loans can help clarify your best move.

When Floating Actually Makes Sense

Floating isn’t for everyone, but it has its moments. It makes perfect sense if you’re planning to sell your property in the next few months. You stay nimble and avoid break fees entirely. It is also a brilliant option if you’re expecting a windfall, like a work bonus or an inheritance. Floating loans let you pay down as much debt as you want, whenever you want. For those who hate the idea of being “locked in” to a bank contract, that extra bit of freedom is often worth the slightly higher interest rate.

Choosing Your Term: Should You Fix for 1 Year or 5?

Picking the right term for your fixed rate mortgage is less about outsmarting the bank and more about understanding your own life. Banks spend millions trying to predict where rates will go, but their guesses are often as good as yours. Ultimately, the “best” term for you depends far more on your personal job security and future plans than on any spreadsheet from a bank economist. You need to decide how long you want that “peace of mind” window to stay open.

If you reckon interest rates are on a downward slide, a short-term fix of six months to one year might be your best bet. This keeps you on a short leash, allowing you to re-fix at a lower rate sooner if the market moves in your favour. However, if you crave stability, a medium-term fix of two to three years is often the “sweet spot” for many Kiwi families. It offers a solid block of time where you don’t have to worry about your repayments changing, usually at a more competitive price than the longer options.

For those who want to set their budget and forget about it, long-term fixes of four to five years provide the ultimate certainty. You might pay a small premium for this extra protection, but for some, the ability to ignore the news for half a decade is worth every cent. It is essentially an insurance policy against future rate hikes.

The 2026 Economic Outlook and Your Mortgage

Understanding the ocr meaning is crucial because it directly influences what the banks charge you. In 2026, we are seeing a shift in how banks price their terms. They are reacting to global signals that might make long-term rates look quite different compared to short-term ones. Don’t fall into the trap of trying to time the market perfectly. Instead, aim for a term that lets you live your life comfortably within your means without constantly checking the headlines.

Addressing the fear of missing out (FOMO)

It is easy to get a case of “rate envy” when you hear a mate bragging about their 5% rate while you are locked in at 6%. If rates drop after you have signed your fixed rate mortgage contract, don’t panic. You made a decision based on the protection you needed at the time. Focus on your own debt-to-income health rather than market gossip. A slightly higher rate with absolute certainty is often better for your mental health than a lower rate that leaves you constantly stressed about the next move.

The Split Loan Strategy: The Best of Both Worlds

Most people think they have to choose between a fixed or floating rate, but you don’t actually have to put all your eggs in one basket. A split loan strategy allows you to divide your debt into different portions. You can have the majority of your debt in a fixed rate mortgage for that essential budget security while keeping a smaller slice on a floating rate for flexibility. This approach is a brilliant way to manage the debt to income ratio NZ rules, as it keeps your core repayments predictable while giving you room to move.

One popular method is the 80/20 split. You lock in 80% of your loan to protect yourself from rate hikes and leave 20% floating. This 20% portion is your “flexibility zone” where you can make extra repayments without any penalties. Another smart move is the staggered fix. This involves splitting your loan into two fixed portions, for example, half for one year and half for three years. It ensures that you’re never faced with the prospect of your entire loan coming up for renewal at the same time during a period of high interest.

Hedging your bets

Staggering your fixed dates is all about reducing “sticker shock.” If interest rates have jumped significantly by the time your one year term ends, only half of your loan is affected by the higher cost. The other half remains safely tucked away at your original lower rate for another two years. This gives you a chance to re-evaluate your household budget every year and adjust your spending without your entire financial world being turned upside down at once. It is a methodical way to stay in control of your debt.

Using the floating portion for “Offsetting”

If you have some savings sitting in the bank, you can use them to “offset” the interest on the floating part of your loan. Essentially, the bank only charges you interest on the difference between your loan balance and your savings balance. This is a fair dinkum way to pay off your house years earlier because every dollar you save is effectively working to reduce your mortgage. You keep the safety of your fixed rate shield on the main loan while using your cash to chip away at the floating portion. If you want to see how this could work for your specific numbers, reach out to us for a chat about your home loan options.

How a Broker Helps You Navigate Fixed Rates in 2026

When you go straight to a bank, you’re only seeing one small slice of what’s actually available. Banks are in the business of selling their own products, which means they won’t tell you if a competitor down the road has a much better deal. A broker works differently. We scan the entire market to find the fixed rate mortgage that truly fits your life, not just the one a single bank wants to push this month. We handle the hard yakka of the negotiation process, dealing with the endless paperwork and the back-and-forth phone calls so you can focus on your move. Having a mentor like Krish Krishna on your side means you get years of industry experience and a steady hand to guide you. That personal connection and advocacy beat a faceless, automated banking app every single time.

Negotiating a mortgage isn’t just about the interest rate itself. It’s about the fine print, the flexibility for extra repayments, and even the cash-back offers that banks use to entice new customers. We know which levers to pull to get you a better result. We act as your bridge between the rigid world of institutional banking and your personal financial goals. You aren’t just another application number to us; you’re a partner whose success is our priority.

Beyond the “Big Four” Banks

Sometimes your financial profile is a bit unique. Perhaps you’re self-employed, have a fluctuating income, or maybe you’re just starting a new business venture. In these cases, the “Big Four” banks might be quick to say no because you don’t fit into their standard boxes. This is where 2nd tier lenders can be an absolute lifesaver. These lenders are often more flexible and willing to look at the bigger picture of your financial health. We specialise in finding funding for people who don’t fit the standard criteria. Don’t let a “no” from a mainstream bank stop your home-owning dreams. There is almost always a path forward if you know where to look.

Your Next Steps to Financial Freedom

Don’t wait until the last minute to think about your next move. We recommend reviewing your current rate at least 60 days before it expires. This window gives us enough time to scan the market, compare new fixed rate mortgage options, and lock in a rate before they potentially climb higher. A quick “Home Loan Check-in” is a great way to see if your current loan structure still matches your lifestyle and your goals for the coming year. It’s a simple step that could save you thousands in the long run. Let’s have a chat about your mortgage strategy today and make sure your home loan is working as hard as you do.

Secure Your Financial Future Today

Choosing between a fixed rate mortgage and a floating one doesn’t have to be a gamble. By now, you’ve seen how a well-structured split loan can offer both the safety of a fixed rate and the flexibility to pay down debt faster. Whether you are leaning towards a short term fix to see where the market goes or a long term anchor for your budget, the right choice always aligns with your personal life goals rather than just bank forecasts.

With over 20 years of banking and brokerage experience, we are here to ensure you never feel processed or ignored. We specialise in finding solutions through 2nd tier and alternative lending for those who don’t fit the standard bank mould, providing nationwide service for all Kiwis. Don’t leave your biggest financial decision to an automated app. Book a free consultation with Mortgage Suite Ltd today to build a mortgage structure that truly fits your lifestyle. You’ve got this, and we’re ready to help you every step of the way.

Frequently Asked Questions

Is it better to fix for 1 year or 2 years right now?

The better choice between a one year or two year term depends entirely on whether you value immediate flexibility or a longer period of budget certainty. If you believe interest rates will drop soon, a one year fix allows you to re-evaluate your options earlier. However, if you prefer to set your budget and forget about it, a two year term often provides a better balance of security and value without the stress of frequent renewals.

What happens when my fixed rate term ends?

When your fixed term expires, your loan will automatically roll onto the bank’s floating interest rate. This floating rate is usually higher than most fixed options, so it is important to organise a new fixed term at least 60 days before your current one ends. We can help you compare the latest market offers to ensure you don’t end up paying more than you should by default.

Can I pay extra on a fixed rate mortgage?

Most banks allow you to make a limited amount of extra repayments on your fixed rate mortgage each year without penalty. This is often capped at a certain percentage of the loan balance or a specific dollar amount, such as $10,000. If you plan to pay off a large chunk of your debt quickly, keeping a portion of your loan on a floating rate is usually a much more flexible strategy.

What are break fees and how are they calculated?

Break fees are charges you pay to the bank if you end your fixed contract before the agreed date. They are calculated based on how much interest rates have changed since you first locked in your fixed rate mortgage and the bank’s potential loss. If current market rates are lower than your fixed rate, the bank will likely charge you a fee to cover the difference for the remainder of your term.

Can I change from a fixed to a floating rate mid-term?

You can certainly change from a fixed to a floating rate before your term is up, but it usually comes with a cost. Because you are breaking a legal contract with the bank, they will likely charge you a break fee. It is always worth asking for a quote first so you can decide if the flexibility of a floating rate outweighs the immediate expense of the penalty.

How much deposit do I need for a fixed rate mortgage in NZ?

In New Zealand, most lenders prefer a 20% deposit for a standard home loan, though some first home buyer programs allow for as little as 10%. The amount you need can also depend on whether you are buying an existing home or building a new one. Having a larger deposit generally gives you access to better interest rates and more choices when it comes to selecting a lender.

Will mortgage rates go down in 2026?

Predicting exactly if rates will drop in 2026 is tricky, as it depends on inflation and the Reserve Bank’s Official Cash Rate decisions and what the OCR meaning is for your mortgage. While some global markets have seen rates stabilise, the local outlook is always subject to change based on the wider economy. We focus on building a mortgage structure that you can afford comfortably today, rather than relying on guesses about what might happen tomorrow.

What is the “reserve rate agreement” ANZ and others talk about?

A reserve rate agreement is essentially a rate lock that guarantees your interest rate for a specific period, usually up to 60 days, before your loan actually settles. This protects you from any sudden rate hikes that might occur while your property purchase is being finalised. It provides a vital layer of security, ensuring the repayments you budgeted for are the ones you actually end up with.