Interest Only Investment Property Loan NZ: A Strategic Guide for 2026

What if the smartest way to build your wealth wasn’t actually paying off your debt as fast as possible? Most people think an interest only investment property loan nz is just a temporary fix to keep your head above water, but in 2026, it’s actually a clever strategy to help you grow your portfolio faster. You’ve probably noticed that even with the latest tax rules that let you claim back interest, low rental returns can make it really tough to cover both the loan repayments and the interest every month. It’s discouraging when your big plans are held back by banks with strict rules that don’t seem to care about your personal goals.

We understand that frustration, and we’re here to show you a better path forward by using interest-only periods to free up your cash for your next move. This guide will walk you through how to boost your monthly cash flow, make the most of current tax rules, and create a solid plan for securing your second or third property. You’ll discover how to look beyond the big banks and build a long-term strategy that actually works in today’s New Zealand market. By the time you’ve finished reading, you’ll have a clear, simple roadmap to grow your portfolio and your wealth with total confidence.

Key Takeaways

- See how switching to interest-only payments can immediately improve your monthly cash flow, giving you more room to manage costs or save for your next move.

- Explore how an interest only investment property loan nz works with the latest tax changes to help you keep more of your rental income.

- Learn the truth about “payment shock” and how to use smart refinancing to extend your interest-only periods safely.

- Discover why looking beyond the big banks can give you the flexibility needed to grow a larger property portfolio.

- Follow our simple two-step process to audit your current equity and map out a clear path toward your financial goals.

What is an interest only investment property loan in the NZ market?

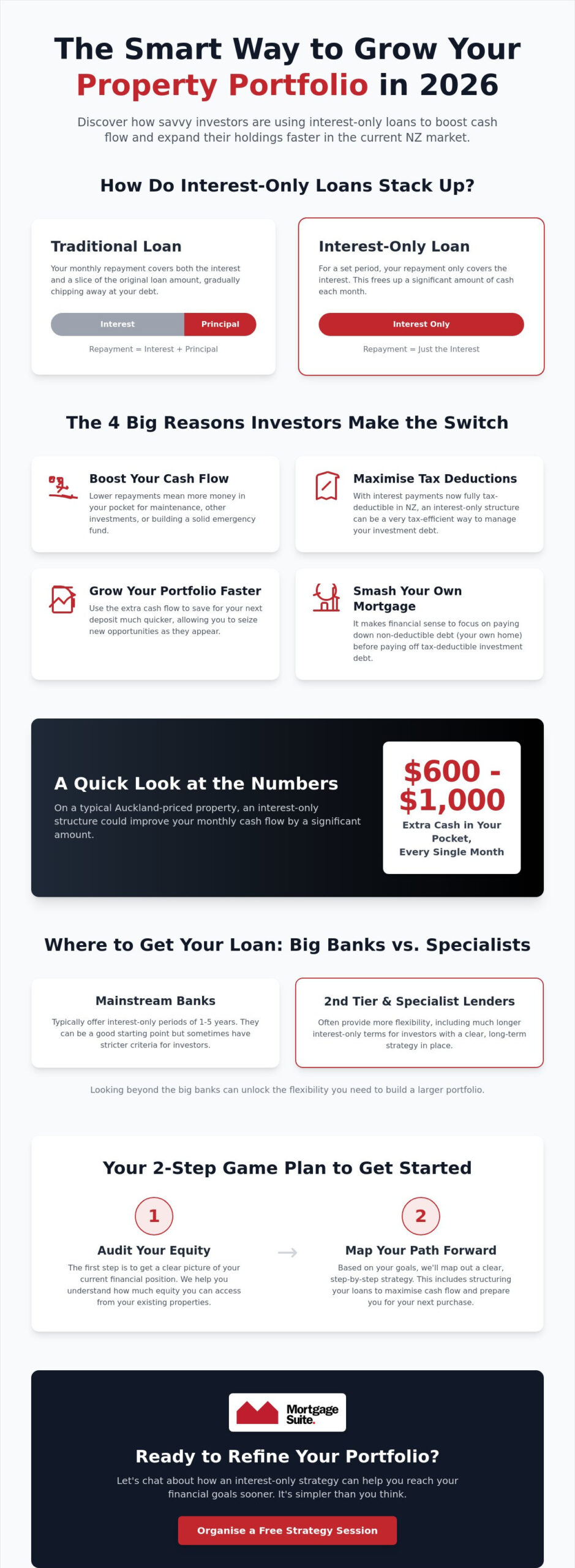

At its heart, an interest-only loan is a setup where your regular repayments only cover the interest charges on the money you’ve borrowed. You aren’t actually chipping away at the original loan amount during this time. It’s a bit like paying “rent” to the bank for the use of their money while you wait for the property to grow in value or for your rental income to increase. Choosing an interest only investment property loan nz is a deliberate choice for many people who want to keep their monthly outgoings as low as possible.

In the 2026 New Zealand market, this approach has become a go-to strategy for those looking to build a portfolio. With the full restoration of interest tax claims that started back in 2025, the financial landscape for landlords has shifted. Investors are moving away from traditional repayment structures to better manage their rental returns. While the amount you owe stays the same, the extra cash in your pocket provides a safety net or a springboard for your next purchase. Most big banks offer these periods for one to five years, though some specialist lenders are now providing much longer terms if you have the right strategy in place. For a comprehensive overview of how residential investment property loans NZ work in today’s lending environment, our 2026 investor’s reference guide covers the full landscape in detail.

The difference between traditional loans and interest-only

The main difference is how your money is used each month. With a standard loan, your payment is split between the interest and a small portion that reduces your debt. With an interest-only loan, you skip that debt reduction part entirely. On a standard Auckland-priced property, this can be a real game changer for your bank balance. Based on current 2026 interest rates, your monthly repayments could be $600 to $1,000 lower than they would be on a traditional loan. It’s important to remember that this isn’t about avoiding your debt forever. It’s a strategic cash-flow management tool rather than a permanent debt state.

Why 2026 is the year of “Refining” your portfolio

We’ve seen plenty of change lately. With the Official Cash Rate sitting at 2.25% as of late 2025, mortgage rates have stabilised, but they still require careful management to stay profitable. Using interest-only periods allows you to stay in the game even during high-interest cycles without feeling the squeeze on your lifestyle. This year is all about refining investment property NZ portfolios. By structuring your debt more intelligently, you can ensure your existing properties aren’t just sitting there, but are actually working to fund your next move. This interest only investment property loan nz strategy ensures you have the cash ready to jump on new opportunities as they come up.

The top 4 reasons NZ investors choose interest-only loans

Deciding how to pay back your bank is a huge part of your financial strategy. For many, an interest only investment property loan nz isn’t just about making life easier today; it’s a smart way to build wealth much faster. There are four big reasons why this works so well in the current market. First, it keeps your monthly cash flow high. By not paying down the original loan amount, you keep more money in your pocket to cover maintenance, unexpected repairs, or to build a healthy emergency buffer. Second, it’s very tax-efficient. Since you can now claim back 100% of your interest, keeping that loan amount steady can actually help you when it’s time to talk to your accountant.

Growing your portfolio is often a race against time and how much cash you have available. This brings us to the third reason: helping you grow. You can save the extra cash you aren’t giving to the bank to reach your next deposit goal much quicker. Finally, it lets you focus on your personal debt. It makes very little sense to pay off a tax-friendly investment loan while you still have a mortgage on your own family home. Pausing the repayments on your rental debt lets you smash your own home loan first, which is a much more effective way to use your income.

Boosting your actual return

The logic here is quite simple: when your outgoings are lower, your actual return on the money you’ve put into the property goes up. In a market where rental income can be tight, this structure often makes the difference between a property that pays for itself and one that costs you money every week. It also means you aren’t tying up your cash in a low-interest debt when you could be using that money to invest elsewhere for a better result.

The “Home First” strategy

We often talk to clients who feel a bit guilty about not paying off their investment debt, but the “Home First” strategy is a total game changer. Your family home loan isn’t tax-deductible, so it should always be the first thing you try to get rid of. By using the extra cash from your interest-only period, you can make significant extra payments on your own home mortgage. If you’re currently using home equity for investment NZ, this ensures you’re clearing your most expensive debt first while your rental property potentially grows in value. If you want to see how these numbers look for your own situation, our team would love to help you check your lending options and find a plan that puts your home first.

Is an interest-only loan risky? Addressing the big objections

It’s natural to feel a bit of hesitation when considering an interest only investment property loan nz. We often hear the same concern from clients: “What happens when the five-year term is up?” The fear of a “payment shock” — where your repayments suddenly jump because you’re forced onto a principal and interest structure — is a common worry. However, for most proactive investors, this is more of a myth than a reality. You aren’t simply at the mercy of the clock; you’re in the driver’s seat of a strategic financial plan. Most investors don’t wait for the term to end; they’re already looking at their next move well before the deadline hits.

In New Zealand, wealth is traditionally built through capital gains rather than the slow grind of debt reduction. By choosing not to pay down the principal, you’re making a deliberate choice to prioritise your cash flow today. This allows you to hold your property through market cycles, like the current stabilisation phase we’re seeing in 2026. If the property value increases while your debt stays the same, your equity still grows. It’s about understanding that an interest-only period is a tool for a specific phase of your investment journey, not a permanent state of debt.

Managing the “End of Term” transition

When your interest-only period approaches its end, you generally have three paths: refinance with a new lender to start a fresh interest-only term, extend the current arrangement with your existing bank, or transition into principal and interest repayments if your cash flow allows it. This is where having an expert broker becomes vital. We recommend starting these conversations at least six months before your term expires. This gives us enough time to negotiate with lenders or look at second-tier options if the mainstream banks have become too rigid. Every property in your portfolio needs a clear exit strategy or a plan for this transition to ensure you’re never caught off guard.

The impact of DTI and LVR restrictions

The lending environment has changed significantly with the Reserve Bank of NZ’s latest rules. While the 70% LVR restriction for investors is a known factor, the Debt-to-Income (DTI) restrictions introduced in 2026 have added a new layer of assessment. These rules can sometimes limit your ability to simply “roll over” an interest-only loan if your total debt levels are high relative to your earnings. As of 2026, DTI limits have forced non-bank lenders to scrutinise interest-only applications through a much tighter lens, focusing heavily on a borrower’s total debt across their entire portfolio rather than just the individual property’s yield. Structuring your loans correctly from the start is the best way to ensure you remain flexible as regulations evolve. Our guide to residential investment property loans NZ explains exactly how to navigate these DTI and LVR rules when structuring your next application.

Mainstream banks vs. 2nd tier lenders: Where to get your IO loan

Most investors start their journey with one of the big four banks, but many eventually run into what we call “bank fatigue”. It’s a common hurdle where mainstream lenders often cap an interest only investment property loan nz at a total of five years. Once you hit that limit, the bank will typically insist you switch to principal and interest repayments. For a growing portfolio, this sudden increase in monthly outgoings can be a massive blow to your strategy. This is exactly why we look for “hidden” lenders that the big banks don’t want you to know about, ensuring your plans aren’t cut short by rigid internal policies.

You might notice that interest rates at non-bank lenders are sometimes a fraction higher than the “special” rates advertised by the big banks. However, it’s vital to look at the bigger picture of your cash flow. A slightly higher interest rate on an interest-only basis often results in much lower monthly payments than a lower rate on a principal and interest basis. We help you crunch these numbers to see which option actually keeps more money in your pocket each month. It’s about finding the right balance between the cost of the money and the flexibility it gives you to keep moving forward.

When to look beyond the “Big Four”

If your bank has recently declined your application due to high DTI levels or what they call “unserviceable” debt, it’s time to look elsewhere. Non-bank lenders are often much more accommodating for self-employed borrowers or those with complex income structures. Many of our clients also choose a “split banking” strategy to keep their personal home and their investments with different lenders. This protects your family home from being tied up in the same security net as your rentals. You can learn more about these options in our guide to non-bank investment property loans NZ.

The flexibility of 2nd tier loan structures

The real advantage of 2nd tier lenders is their investor-friendly mindset. While a retail bank might have a strict five-year limit, some non-banks are willing to offer longer interest-only periods, sometimes even for the life of the loan in specific cases. This flexibility is a game changer for anyone focused on long-term wealth rather than just paying down debt. With over 20 years of banking experience, Krish Krishna knows exactly how to pitch your case to these lenders to get the best possible outcome. If you feel like your bank is holding you back, contact us today to explore a lending structure that actually fits your goals.

How to set up your interest-only strategy with Mortgage Suite

Setting up an interest only investment property loan nz requires more than just filling out a form; it demands a clear, long-term vision. We’ve refined a four-step process that takes the guesswork out of your lending. It begins with Step 1: The Portfolio Audit. We take a look at your current equity and debt structure to see if your money is working as hard as it should be. Many investors have “lazy” equity sitting in their homes that could be better utilised. Step 2 is all about Defining the Goal. We need to know if your priority is boosting your weekly cash flow or if you’re trying to stockpile a deposit for a new build by the end of 2026.

Once we have your roadmap, we move to Step 3: The Lender Match. This is where our deep institutional knowledge comes into play. We don’t just look at the big banks like ANZ or Westpac; we also scan the second-tier market to find a lender whose criteria match your specific profile. Step 4 is The Application. We handle the heavy lifting, the phone calls, and the complex negotiations on your behalf. Our goal is to remove the obstacles that often stand between an investor and their next property, ensuring the process is as smooth as possible. We make sure the bank understands your strategy so they see you as a professional investor rather than just another borrower.

Why a specialist broker makes the difference

Having a dedicated negotiator in your corner is a massive advantage in today’s shifting market. We understand the nuances of the non-bank landscape and how to present your case to get a “yes” when others might say “no”. We take great pride in helping first-home buyers transition into the world of property investment, guiding them through that first crucial purchase. Because Mortgage Suite serves clients nationally across NZ, we can help you organise your finance regardless of where you are located. You get the benefit of our 20 plus years of experience, combined with a personal touch that the big banks often lack.

Your next steps for 2026

If you’re ready to refine your strategy, the best place to start is with a no-obligation chat. We can review your current interest rates and see if there is a more efficient way to structure your repayments. It is also worth checking our latest guide on equity release home loan NZ to see how you can unlock the value in your existing home to fund your next move. We aren’t just here for a single transaction; we’re here to be your partners in long-term wealth creation. Let’s work together to ensure your portfolio is robust, profitable, and ready for whatever the market brings next.

Take control of your property investment future

An interest only investment property loan nz is more than just a way to lower your monthly outgoings; it’s a tactical choice that gives you the flexibility to grow your portfolio with confidence. We’ve seen how smart debt structuring and choosing the right lender can help you manage your cash flow while staying ahead of changing regulations. Whether you’re looking to clear your personal mortgage faster or secure your next rental, having a clear plan is what separates a successful investor from the rest.

At Mortgage Suite, we bring over 20 years of banking and brokerage experience to the table. We specialise in complex investment structures and have deep connections with both mainstream and second-tier non-bank lenders. We’ll handle the heavy lifting and act as your dedicated negotiator to ensure you get the best possible outcome for your personal situation. Book a strategy session with Krish and the Mortgage Suite team today to start refining your strategy for 2026. We’re excited to partner with you on your journey toward long-term wealth and success.

Frequently Asked Questions

Can I get an interest-only loan for my own home in NZ?

Yes, it is possible, but banks are generally much stricter with home loans for owner-occupiers. They usually only grant these for a short period, typically one to two years, for specific reasons like a temporary drop in income or during major renovations. Mainstream lenders prefer you to pay down the debt on your own home to build equity rather than just paying the interest.

How long can an interest-only period last on an investment property?

Most mainstream banks in New Zealand offer interest-only terms between one and five years. However, there are exceptions, such as ANZ, which currently offers up to ten years for property investors. If you need a longer period to suit your strategy, we often look at non-bank lenders who can provide more flexibility with their timeframes and extension options.

Will an interest-only loan cost me more in the long run?

You will pay more total interest over the life of the loan because you aren’t reducing the principal balance. Since the debt stays the same, the bank charges interest on the full amount for a longer period. While the monthly outgoings are lower, you need to weigh this up against the long-term cost, though many investors find the improved cash flow is worth the trade-off.

Do I need a bigger deposit for an interest-only investment loan?

The deposit requirements are usually the same as a standard loan, which is typically 30% for investors under current 2026 LVR rules. The main difference lies in the bank’s assessment of your ability to pay. They will check your income more rigorously to ensure you can still afford the repayments once the interest-only period ends and you’re required to pay back the principal.

Can I switch from principal and interest to interest-only midway through my loan?

You can certainly ask to switch, but the bank will treat this as a fresh application. They’ll perform a full credit assessment to make sure you meet their current 2026 lending standards. This includes checking your income against the latest debt-to-income (DTI) restrictions to ensure the new repayment structure is sustainable for your personal situation and doesn’t put you at risk.

What happens if the property value drops during my interest-only period?

If the property value falls, your equity decreases because your loan balance remains exactly the same. This doesn’t usually impact your daily life unless you need to sell the property or refinance with a different lender. It’s a reminder of why we always recommend keeping a healthy equity buffer and taking a long-term view of the New Zealand property market.

Are interest-only loans still tax-deductible in New Zealand?

Yes, 100% of the interest on residential investment loans is deductible for the 2025/2026 tax year. This full restoration of deductibility makes an interest only investment property loan nz a highly effective tool for landlords. It allows you to maximise your tax claims while keeping your monthly costs low, which is a significant shift from the rules we saw a few years ago.

Why would a non-bank lender be better for an interest-only loan?

Non-bank lenders often provide a level of flexibility that the big retail banks simply can’t match. They are frequently more willing to offer longer interest-only terms or work with borrowers who have complex income, such as being self-employed. If you’ve hit a wall with your current bank’s internal limits, a second-tier lender can often provide the breathing room you need to keep growing.