Using Home Equity for Investment in NZ: A 2026 Guide to Growing Your Wealth

What if your most valuable asset is currently sitting idle while you wait years to save up a massive cash deposit? For many Kiwis, the dream of building wealth feels blocked by strict bank rules and the confusing maze of LVR limits. It’s completely normal to feel a bit hesitant about over-leveraging, especially with interest rates shifting and the latest debt-to-income rules in play.

The good news is that you don’t necessarily need a pile of cash to get started. By using home equity for investment NZ, you can unlock the value already tied up in your bricks and mortar to fuel your next move. This guide will walk you through the process of identifying your “usable equity” and show you how to work through the 2026 lending landscape with confidence. We’ll look at how to bypass common roadblocks, understand the current 70% LVR rules for investors, and find a lender that fits your specific situation so you can grow your portfolio without the stress.

Key Takeaways

- Learn how to identify the portion of your home you truly own and how market changes can speed up your wealth-building journey.

- Discover the simple two-step process for using home equity for investment NZ to calculate exactly how much you can borrow.

- Explore why using your home’s value can help you start investing years earlier than waiting to save a traditional cash deposit.

- Understand your options if a big bank turns you down, including how non-bank lenders can provide a path forward.

- Get a practical checklist for organising your documents so you’re ready to chat with a specialist and take the next step.

What is home equity and how does it work for NZ investors?

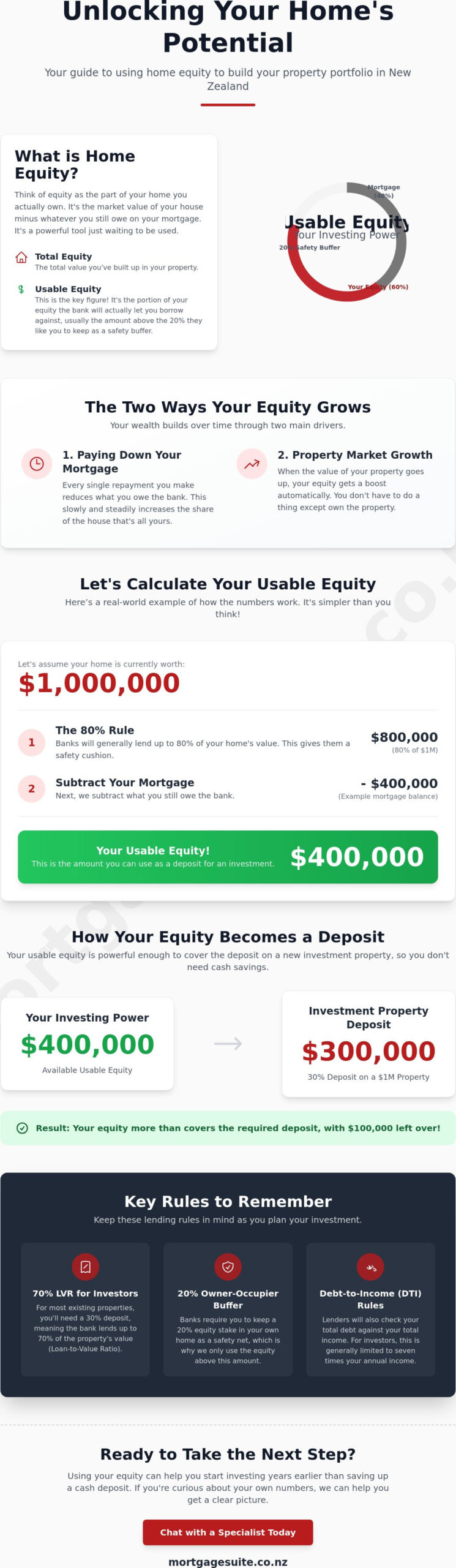

Equity is essentially the share of your home that belongs to you rather than the bank. Think of it as the cash you’d have left over if you sold your house today and paid back every cent you owe on your mortgage. It isn’t just a number on a statement; it’s a powerful financial tool. Many people wonder, what is home equity? and how can it help them build a future. In New Zealand, this value grows in two main ways. First, every time you make a mortgage repayment, you’re slowly buying back your house from the bank. Second, if the market value of your property increases, your equity gets a natural boost without you lifting a finger.

In 2026, we’re seeing a unique shift in the market. With the Reserve Bank holding the Official Cash Rate at 2.25% as of May 2026 and signalling potential hikes, understanding how to use what you already have is more important than ever. Instead of waiting years to save a massive pile of cash, using home equity for investment NZ allows you to treat that value like a virtual deposit. It’s a way to jumpstart your portfolio while your current home does the heavy lifting.

The difference between total equity and usable equity

It’s a common mistake to think you can spend every dollar of equity you have. Banks are cautious; they want a safety buffer to protect themselves if property prices take a sudden dip. Because of this, they won’t let you borrow against 100% of your home’s value. Generally, for your own home, banks prefer you to keep at least 20% of the value as a “hands-off” zone. Your usable equity is the amount above that 20% mark. This is the only figure that really matters when you’re planning your next move.

How your home becomes the deposit for a rental

You might have heard the term “cross-collateralisation.” It sounds like a mouthful, but it just means the bank uses your current home as security for a new loan on an investment property. Under the rules set in December 2025, investors usually need a 30% deposit for a rental property. By using home equity for investment NZ, you can cover that 30% using the value in your existing home instead of cash. This removes the massive hurdle of saving for years. It gives you the freedom to act when the right opportunity comes along, using the house you already live in to secure your family’s financial future.

Calculating your usable equity: The 2026 NZ rules

Figuring out your actual borrowing power starts with a bit of simple arithmetic. While your bank statement shows your current balance, it doesn’t tell the full story of your potential. To get a clear picture of using home equity for investment NZ, you first need a realistic appraisal of what your home would sell for in the current market. Once you have that number and your exact mortgage balance, you can start applying the 2026 rules that banks use to decide how much they’ll lend you.

The process follows four logical steps. First, get that professional appraisal. Second, confirm your remaining mortgage balance down to the cent. Third, apply the 80% rule to your home; banks generally want you to keep 20% of the value as a safety net. Finally, you must factor in the current limits for the new property you want to buy. Following the NZ government house buying process is essential here, as it ensures you’re across the latest tax and compliance requirements while you crunch these numbers.

Understanding RBNZ LVR (Loan-to-Value Ratio) limits

As of the latest updates in December 2025, the Reserve Bank has set clear boundaries for investors. For most existing homes, you’ll need a 30% deposit, meaning the bank will lend up to a 70% LVR. LVR is simply the relationship between the money you owe and the property’s value as determined by the bank. If you’re looking at a new build, the rules are often more relaxed, sometimes requiring a much smaller deposit. You also need to keep the Debt-to-Income (DTI) rules in mind, which since July 2024, generally limit investor lending to seven times your annual income.

A quick example of the maths in action

Let’s look at how this works in the real world. Imagine you own a home worth $1 million with a $400,000 mortgage. The bank allows you to borrow up to 80% of your home’s value, which is $800,000. Subtract your $400,000 mortgage, and you have $400,000 in “usable” equity. If you want to buy an investment flat for $1 million, the 30% deposit requirement is $300,000. Because you have $400,000 available, your equity completely covers the deposit. You could potentially buy that investment property without touching your savings. If these numbers feel a bit overwhelming, a quick chat with the team at Mortgage Suite Ltd can help clear up exactly where you stand.

The pros and cons of using equity for property investment

Deciding to tap into your home’s value is a big step. It’s a bit of a balancing act between the excitement of growing your wealth and the reality of taking on more responsibility. One of the biggest wins is speed. In a market where prices can shift quickly, waiting to save a 30% cash deposit can mean you’re stuck on the sidelines for years. By using home equity for investment NZ, you can jump in as soon as the numbers make sense. Plus, since April 2025, you can once again claim 100% of your interest costs as a tax deduction on residential rentals, which makes the maths much friendlier than it was a few years ago.

On the flip side, you’re signing up for a bigger mortgage. That means your monthly repayments will increase, and you need to be sure your income can handle it. There’s also the risk of negative equity. If the market takes a breather and property values drop, you could end up owing more than the properties are worth. It’s a rare scenario for long-term investors who buy well, but it is something you should always keep in the back of your mind before signing on the dotted line.

Why using equity beats a personal loan every time

If you need funds for a deposit, a personal loan might seem like a quick fix, but it’s usually a poor choice for property. Mortgage rates are significantly lower than unsecured debt rates, which can save you thousands in interest over the life of the loan. You also have the luxury of spreading those repayments over 25 or 30 years, which keeps your weekly cash flow much healthier. Keeping everything organised under one lending umbrella also makes your life a lot simpler when it comes to tax time and your annual financial reviews.

Managing the risks of a bigger mortgage

Success in property isn’t just about buying; it’s about staying in the game. Banks focus heavily on your ability to meet repayments, especially with the 2024 DTI rules in place. Even with the OCR sitting at 2.25% as of May 2026, the Reserve Bank has hinted that rate hikes are likely. You should always test your budget against higher interest rates to ensure you aren’t caught out if your fixed term ends and rates have moved up. One strategy worth exploring is an interest only investment property loan NZ investors are increasingly using to free up monthly cash flow and keep their portfolio growing during uncertain rate environments. A solid “rainy day” fund is also a must. Rentals have a habit of needing urgent repairs at the worst possible time, and you don’t want to be scrambling for cash when the hot water cylinder gives up. Being prepared for these moments is what separates a stressed landlord from a successful investor.

The step-by-step process to unlock your equity

Once you’ve crunched the numbers and seen the potential in your own home, it’s time to move from theory into action. The actual process of using home equity for investment NZ starts with a conversation with a specialist broker who knows the 2026 lending landscape inside out. They’ll help you look past the standard bank calculators to see what’s truly possible for your situation. Your first job is to get your paperwork sorted. This means gathering recent bank statements and proof of income to show the bank that you aren’t just asset-rich, but also a reliable borrower who handles their day-to-day cash flow with discipline.

Sometimes, the bank’s automated valuation system might give you a figure that feels a bit low. If that’s the case, a registered valuation from an independent professional can often reveal the true market value of your property, potentially unlocking more funds for your deposit. Once your value is confirmed and your application is reviewed, the goal is to secure a pre-approval. This is a game-changer. It gives you the confidence to walk into an auction or make an offer on a rental property knowing exactly where you stand, without the stress of a last-minute scramble for finance.

Preparing your finances for the bank’s “stress test”

Banks are incredibly thorough when they review your spending habits. They aren’t just looking at your salary; they’re checking your discretionary spending to see how a new loan will affect your lifestyle. Those daily flat whites or frequent takeaway meals might seem small, but they’re factored into the bank’s “stress test” of your finances. One of the smartest things you can do before applying is to “clean up” any short-term debt, like car loans or credit cards. Reducing these monthly obligations makes your application look much healthier and can significantly boost your borrowing power when you’re eyeing up a rental property.

Sticking with your bank vs. looking elsewhere

It’s easy to stay with your current bank because it feels simple, but simplicity can sometimes come at a cost. While your own bank knows your history, a different lender might offer more flexible terms or a lower interest rate that saves you thousands over time. For example, non-bank investment property loans NZ can often provide the breathing room that traditional institutions can’t, especially if your income situation is a little unique. A broker is essential here to compare the fine print and find the best fit for your long-term goals. If you’re ready to start the journey, chat with the experts at Mortgage Suite Ltd to see which path is right for you.

When the bank says “No”: Alternative equity solutions

It’s a frustrating moment when you’ve done the maths, found the perfect property, and your long-term bank turns you down. Mainstream banks are often bound by rigid “box-ticking” exercises that don’t always account for the complexities of real life. They might decline an application because of your age, a small blemish on your credit history, or because your income doesn’t fit their standard template. This is especially common for self-employed Kiwis or those with multiple income streams. However, a “no” from a big bank isn’t the end of your journey toward using home equity for investment NZ.

There is a whole world of 2nd tier and non-bank lenders in the New Zealand market that operate with more flexibility. These lenders often look at the bigger picture, focusing on the quality of the property and your overall strategy rather than just a computer-generated credit score. At Mortgage Suite Ltd, we specialise in finding a “yes” when others have said “no.” We don’t believe in a one-size-fits-all approach. Instead, we focus on tailoring a solution that fits your specific life stage and your long-term wealth goals, ensuring you aren’t held back by institutional red tape.

The power of 2nd tier lending for property investors

2nd tier lenders provide a vital alternative for investors who need a more common-sense approach to borrowing. These lenders often place more weight on the property’s value and its potential rental return than on a perfect financial history. If you’re looking to bridge a gap, a Home Equity Loan can be a powerful tool to get your project moving. These solutions are often used as a short-term stepping stone. You can get into the market now, start growing your equity, and then look to move back to a mainstream bank once you’ve built up a track record or your circumstances change. It’s about keeping your momentum alive when the traditional path is blocked.

Why a veteran broker is your best negotiator

When you’re dealing with non-bank lenders, having a seasoned professional in your corner makes all the difference. Krish Krishna brings over 20 years of banking experience to the table, which means he knows exactly how to frame your story so lenders see the value in your application. Mortgage Suite Ltd acts as a bridge between the rigid world of finance and your personal needs, advocating for you to get the best possible terms rather than just the easiest ones. We take the stress out of the mountain of paperwork and the back-and-forth negotiations. This leaves you free to focus on what really matters: finding the right house and growing your family’s wealth. If you’ve hit a brick wall with your bank, let us help you find the way around it.

Take the first step toward your investment future

Your home is more than just a place to live; it’s a powerful financial engine that can help you grow your wealth. We’ve seen how using home equity for investment NZ allows you to bypass the long wait for a cash deposit and get into the market sooner. By understanding the 2026 lending rules and preparing your finances for the bank’s stress tests, you can turn your existing property value into a thriving portfolio.

Success in property investment often comes down to having the right expert in your corner. With over 20 years of banking expertise and a focus on personalised negotiation, Krish Krishna and the team are here to help you navigate every hurdle. We specialise in finding creative solutions through 2nd tier and non-bank lenders when mainstream banks aren’t the right fit. It’s about more than just a loan; it’s about building a partnership that supports your long-term goals.

Ready to see how much usable equity you have? Book a free equity strategy session with Krish today and get the clarity you need to move forward. Your next investment property could be closer than you think, and we’re excited to help you make it happen.

Frequently Asked Questions

How much equity do I need to buy an investment property in NZ?

You generally need enough equity to cover a 30% deposit for an existing investment property while keeping a 20% safety buffer in your own home. For a $1 million rental, you’d need to unlock $300,000 in usable equity. If you are looking at a new build, the deposit requirements are often lower, so it’s worth checking with a professional to see how the current LVR rules apply to your specific target property.

Can I use equity to buy an investment property with no cash deposit?

Yes, you can buy an investment property with zero cash by using home equity for investment NZ to secure the entire deposit. The bank uses the value in your current home as security for the new loan, meaning you don’t need to dip into your savings. As long as your “usable equity” covers the 30% requirement for an existing house, you can start your investment journey without needing a massive cash pile.

What are the risks of using my home equity for investment?

The main risks include increasing your total debt and the potential for property values to fall. If the market takes a dip, you could end up with negative equity, where you owe the bank more than the properties are worth. You also need to be sure your income can handle higher repayments if interest rates move up, especially since the Reserve Bank signalled in May 2026 that rate hikes are likely.

Do I need a registered valuation to use my home equity?

You will often need a registered valuation if the bank’s automated system doesn’t quite capture the true value of your home. While banks use their own data first, a professional valuer provides a detailed report that can often reveal more equity, especially if you’ve renovated. It’s a small upfront cost that can be the difference between getting a “yes” or a “no” on your investment loan application.

How does the bright-line test affect my investment if I use equity?

The bright-line test means you’ll pay tax on any profit if you sell your investment property within two years of buying it. As of July 1, 2024, the period was shortened to this two-year timeframe for residential property. While your family home is exempt, any rental property you buy using your equity will be subject to these rules. It’s a vital factor to consider when planning your long-term exit strategy.

Can I use equity for a business loan instead of a rental property?

Yes, you can certainly use your home’s equity to secure a business loan. Many Kiwis choose this path because mortgage rates are typically much lower than the rates for unsecured business lending. It’s a cost-effective way to find the capital you need to start a new venture or expand an existing one. Just remember that your home is acting as security, so you need a solid plan to manage the repayments.

What happens to my equity if house prices in NZ drop?

If house prices drop, your total and usable equity will decrease because your home is worth less on paper. While this doesn’t change your mortgage repayments, it does reduce your safety buffer and your ability to borrow more in the future. This is exactly why banks insist on leaving a 20% equity cushion in your own home; it protects both you and the lender if the property market takes a breather.

Is interest on an equity-funded investment loan tax-deductible?

Yes, full interest deductibility for residential investment properties was restored starting from the 2025/2026 income year. This means you can once again claim 100% of the interest you pay on your investment loan against your rental income. This change makes using home equity for investment NZ a much more attractive strategy for building wealth than it was a few years ago, as it significantly improves your weekly cash flow. For investors looking to maximise this benefit, exploring an interest only investment property loan NZ lenders offer can further boost your monthly returns by reducing your required repayments during the investment phase.