Non-Bank Lenders NZ: Your 2026 Guide to Alternative Home Loans

What if a “no” from your local bank wasn’t the end of your home ownership dream, but actually the start of a smarter, more flexible path? If you’ve been turned away because you’re self-employed, have a smaller deposit, or just don’t fit into a tidy little box, it’s easy to feel like the door is locked for good. You might even worry that looking at non bank lenders nz means dealing with “loan sharks” or unregulated companies. It’s a common concern, but the reality in 2026 is far more professional and helpful than the old myths suggest.

We understand that your financial situation is unique, and you deserve a partner who sees the person behind the paperwork. In this guide, we’ll show you how alternative lenders provide a genuine fair go for Kiwis and how to pick the right one for your specific goals. You’ll learn about the “stepping stone” strategy that helps you build equity now so you can move to a mainstream bank later. We’ll also compare the latest 2nd tier options to help you find a clear, safe pathway to your new front door.

Key Takeaways

- Understand why these lenders don’t need a full banking licence to provide a secure and professional home loan.

- Discover how non bank lenders nz use a much larger “box” to assess applications, giving hope to those who don’t fit the standard bank criteria.

- Learn how to get your paperwork in order, including how to handle “alt-doc” evidence if you’re self-employed or run your own business.

- See why these institutions are often the first choice for investors who need to move fast on a property deal without the usual red tape.

- Find out how having a dedicated advocate can help you navigate the 2nd tier market and negotiate a deal that actually fits your life.

What Exactly is a Non-Bank Lender in the NZ Market?

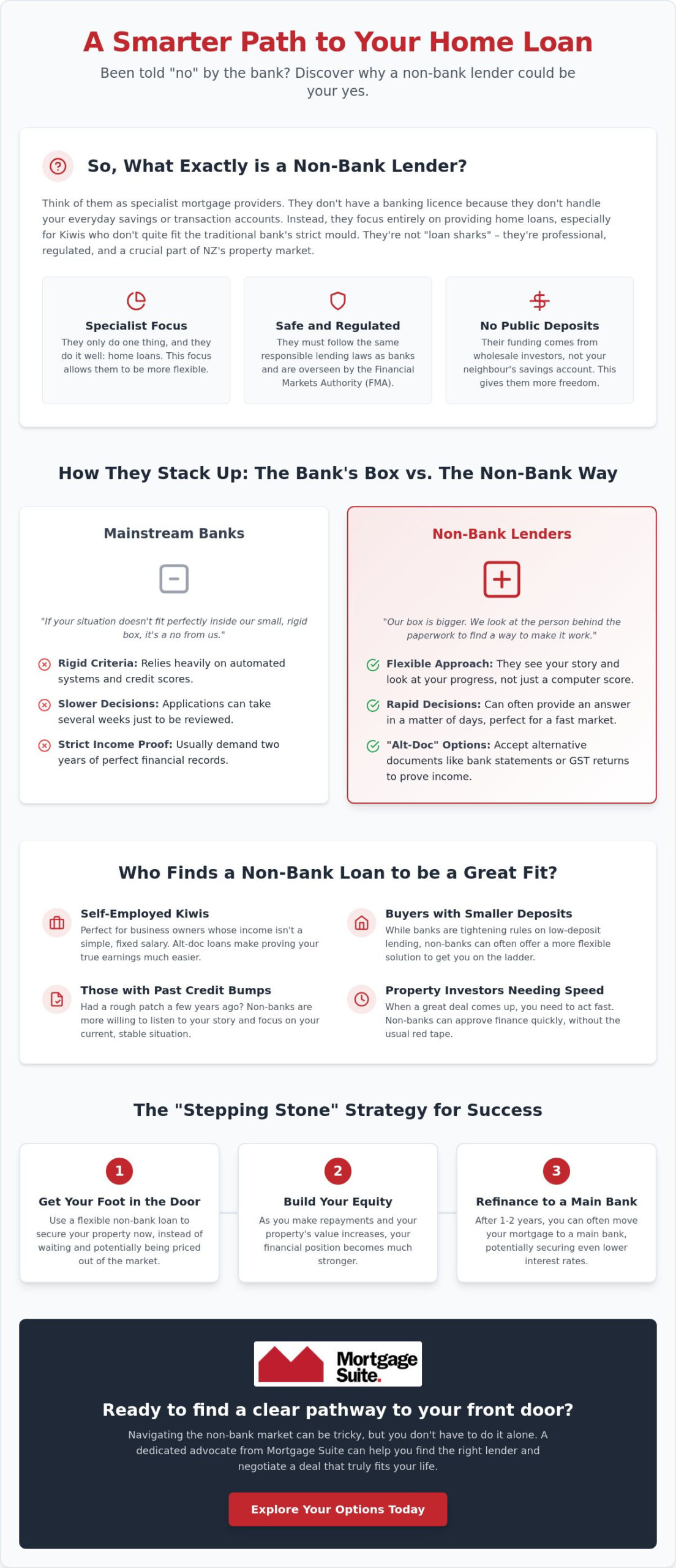

Most Kiwis grow up thinking that if you want a home loan, you have to talk to one of the big banks. But the market has changed. A non-bank financial institution is essentially a company that provides mortgages without being a registered bank. They don’t have a full banking licence from the Reserve Bank; this means they operate differently from the household names you see on every street corner. While they might not be as famous as the “Big Four,” they play a massive role in helping people get onto the property ladder.

The biggest difference is that non bank lenders nz don’t take deposits from the public. You can’t open a savings account or set up a term deposit with them. Because they aren’t managing your everyday transaction accounts, they can focus entirely on being specialist providers for unique situations. They provide a vital alternative for people who don’t fit the standard criteria that mainstream banks demand. It’s about looking at the person, not just a computer program or a rigid set of numbers.

When you look at the landscape of non bank lenders nz, you’ll find they are still strictly regulated and must follow the same responsible lending laws as any other financial institution. They have to be registered on the Financial Service Providers Register; and they are overseen by the Financial Markets Authority. They aren’t “loan sharks” or unregulated outfits. They’re professional organisations that offer a steady hand when the big banks say no.

The Difference Between 2nd Tier and Non-Bank

In the industry, we often use the term “2nd tier” to describe these lenders. It’s just a way of saying they sit in the category right below the main banks. While “non-bank” is the technical term, your mortgage broker might use them interchangeably. Don’t let the “2nd tier” label fool you into thinking they’re small. Many of these lenders are huge, well-funded organisations that have helped thousands of Kiwis into homes over several decades. They simply choose to operate as specialists rather than trying to be everything to everyone.

Where the Money Comes From

If they don’t take your savings, where does the cash for your mortgage come from? Instead of using money from a neighbour’s savings account, non-banks get their funds from wholesale investors, credit lines, or large investment funds. This funding structure is actually a benefit for you. It gives them more freedom to create flexible rules because they aren’t tied to the same rigid deposit-taking regulations as the big banks. A non-bank lender is a private finance company that specialises in flexible mortgage solutions.

Non-Bank Lenders vs Mainstream Banks: Spotting the Differences

Imagine the big four banks, ANZ, Westpac, BNZ, and ASB, as a very small, rigid box. If your financial situation doesn’t fit perfectly inside, the lid won’t close, and you’ll likely receive a “no.” In contrast, non bank lenders nz operate with a much larger box. They aren’t just looking for the perfect applicant; they’re looking for a way to make the deal work. While a big bank might take three weeks just to look at your paperwork, a non-bank often makes a decision in a matter of days. This speed is vital for property investors or anyone trying to secure a home in a fast-moving market.

There’s also a significant difference in how they view you as a person. Big banks rely heavily on automated systems and algorithms. If the computer says no, that’s usually the end of the conversation. This is why non bank lenders nz are often the go-to for people who need a decision that isn’t just based on a computer score. They still value the human element and want to hear the story behind the numbers. If you had a rough patch a few years ago but things are steady now, they’ll actually listen to your explanation and look at the progress you’ve made since then.

Lending Criteria: Why the “No” Becomes a “Yes”

This flexibility is most obvious for self-employed Kiwis. Banks usually want two years of perfect tax returns, which isn’t always realistic for a growing business. Non-banks offer loans that use alternative income documents, which let you prove your income using bank statements or GST returns instead. They also take a more common-sense approach to minor credit issues or “black marks” from the past. Even if you’re looking at a property type that banks find “risky,” such as a small apartment or a home in a rural area; a non-bank is often more willing to take a look. If you’re unsure where you stand, it’s worth having a chat with an expert to explore your options across different lenders.

Interest Rates and Fees

We have to be straight with you: these loans usually come with higher interest rates than what you’ll see on a bank’s billboard. This is called a “risk premium.” Because the lender is being more flexible with their rules, they charge a bit more to cover that extra risk. You’ll also likely see an “application fee” or “establishment fee.” While big banks often waive these, they are a standard part of the process with 2nd tier lenders. It’s the price of getting a “yes” when everyone else said “no,” and for many, it’s a small price to pay to get into their own home sooner.

Why You Might Reckon a Non-Bank Loan is the Right Move

Deciding to look beyond the big banks is often about reclaiming control of your financial future. If you’ve ever felt like your application was unfairly judged by a cold algorithm, you’ll appreciate what we call the “Fair Go” approach. While mainstream banks are bound by rigid rules, non bank lenders nz have the freedom to look at the person behind the paperwork. They understand that life isn’t always a straight line. Maybe you’ve changed careers recently, or perhaps your income fluctuates because you’re a contractor. These lenders see the potential in your situation where a big bank might only see a risk. For borrowers with non-standard income or a unique financial background, non-conforming home loans in New Zealand offer a tailored pathway that mainstream banks simply can’t provide.

This flexibility is a game changer for property investors. In a market where great deals don’t wait around, the ability to move quickly is your greatest asset. Non-banks are also far more practical with how they view the total amount you owe compared to what you earn. While the big institutions have tightened their belts significantly in 2026, alternative lenders often provide more wiggle room for those with solid equity. They are also the masters of bridging finance. If you’ve found your next dream home but haven’t quite settled the sale on your current one, these lenders can bridge that gap and keep your plans on track.

The Pros: Flexibility and Speed

The most obvious benefit is the lack of red tape. You won’t find yourself trapped in a loop of endless branch appointments or repetitive phone calls. These organisations are built for efficiency. They are particularly good at handling income that doesn’t come from a standard salary, such as large annual bonuses or commission-based pay, which big banks often discount or ignore entirely. Because their systems are streamlined, non-bank lenders can often approve a loan in as little as 48 hours. This allows you to bid with confidence at auctions or make unconditional offers while others are still waiting for a callback.

The Cons: What to Watch Out For

It’s important to be realistic about the trade-offs. The primary drawback is the cost; interest rates are higher because the lender is taking on a situation the big banks won’t touch. These higher rates will increase your monthly repayments, so your budget needs to be robust. Some smaller finance houses might also offer shorter loan terms, perhaps only two or three years, rather than the standard thirty. We always suggest viewing a non-bank loan as a “stepping stone.” The goal is usually to secure the property now, build up your equity, and then move back to a mainstream bank once your situation fits their smaller box again.

How to Get Your Ducks in a Row for a Non-Bank Application

Preparing for a home loan application can feel like a big task, especially if you’ve already had a knock-back from a major bank. The good news is that non bank lenders nz have a different set of rules, but they still want to see that you’re a responsible borrower. Taking a few proactive steps now will make the whole process much smoother and increase your chances of a “yes.” It’s all about showing that while you might not fit the bank’s current box, you’re a reliable person with a solid plan.

The first thing you should do is get a “health check” on your credit file. You need to know exactly what’s on there before a lender sees it. If there are any small errors or old bills you’ve forgotten about, now is the time to tidy them up. If you’re self-employed, start gathering your “Alt-Doc” evidence. This usually includes things like GST returns or six months of business bank statements. Because you aren’t providing standard tax returns, these documents are your best way to prove your business is healthy and your income is steady. If your situation involves a complex income structure or past credit issues, it’s also worth reading up on how non-conforming home loans work in New Zealand to understand all the options available to you.

The “Stepping Stone” Strategy

One of the biggest secrets to success in this market is understanding that a non-bank loan doesn’t have to be a thirty-year commitment. We often use these loans as a “stepping stone” to get you where you want to go. The goal is to use twelve to twenty-four months of perfect repayment history to “clean up” your profile. By showing a mainstream bank that you can handle a mortgage at a slightly higher rate without ever missing a payment, you become a much more attractive customer to them later. Mortgage Suite specialises in these transition plans, helping you map out exactly how to move from a 2nd tier lender back to a big bank once your equity has grown or your credit has improved.

Common Paperwork Requirements

Your bank statements are incredibly important when dealing with non bank lenders nz. They aren’t just looking at the numbers; they’re looking at your character. Consistent saving habits or a history of on-time rent payments speak volumes. They want to see that you can manage your day-to-day cash flow responsibly. You should also expect to provide a registered valuation for the property you’re buying. Since these lenders are taking on a bit more risk, they need to be 100% certain about the value of the asset they’re lending against. If you’re ready to get started, it’s a good idea to chat with a specialist broker who can guide you through each step.

Partnering with Mortgage Suite to Navigate the 2nd Tier Landscape

Finding the right path through the alternative lending market is much easier when you have a seasoned expert in your corner. Krish Krishna brings over 20 years of banking experience to the table, giving you a genuine “inside edge” that most borrowers simply don’t have access to. Because he understands exactly how the big banks think and where their limits lie, he can position your application to get the best possible result from non bank lenders nz. This isn’t just about filling out forms; it’s about having a veteran negotiator who knows how to tell your story in a way that lenders respect.

At Mortgage Suite, we act as your personal advocate throughout the entire process. We don’t just work for one lender; we have the freedom to compare options across the entire 2nd tier landscape to find the one that truly fits your life. Whether you are a first-home buyer trying to break into the market or an experienced investor with a complex portfolio, our goal is always your long-term financial health. We aren’t interested in just getting you a quick loan and moving on. We want to ensure that every move you make today sets you up for a stronger financial position tomorrow.

Why a Broker is Essential for Non-Bank Loans

It’s a little-known fact in the industry that many non bank lenders nz actually prefer to work exclusively through brokers. They don’t have large branch networks, so they rely on specialists like us to ensure an application is professional and complete. We take the time to compare the fine print that you might easily miss on your own, such as hidden fees or restrictive terms that could make it harder to switch back to a bank later. If you are just starting your journey, our Home Loans for First Home Buyers guide provides a fantastic foundation for understanding your options in the current market.

Taking the First Step

If you’ve been feeling the weight of a recent bank rejection, remember that it’s often just the start of a new conversation. We’ve helped countless Kiwis who thought their home ownership dreams were over simply because they didn’t fit a standard bank profile. We encourage you to reach out for a no-obligation chat so we can look at your situation with a fresh, professional perspective. We’ll help you map out a clear strategy, whether that’s a short-term bridging loan or a longer-term “stepping stone” plan. Book a consultation with Mortgage Suite today and let’s find the right way forward for you.

Ready to Unlock Your Home Ownership Future?

Finding a way forward when the big banks have said no is all about looking at the bigger picture. You’ve seen how non bank lenders nz provide a genuine alternative by focusing on your unique story rather than just a computer score. By using these flexible options as a stepping stone, you can secure your property today and build the perfect profile to move back to a mainstream bank in the future. It’s a tactical approach that puts you back in the driver’s seat of your financial journey.

With over 20 years of banking expertise, Mortgage Suite acts as your dedicated advocate across all of New Zealand. We specialise in 2nd tier lending solutions and know exactly how to navigate the fine print to find a deal that actually works for you. Don’t let a “no” from a branch manager be the final word on your dreams. Talk to Mortgage Suite about your non-bank loan options today and let’s start planning your next move. We’re here to help you turn that property goal into a reality with a clear, professional path forward.

Frequently Asked Questions

Are non-bank lenders in NZ safe to use?

Yes, they are absolutely safe as long as they are registered on the Financial Service Providers Register. While they don’t have a full banking licence, they must still follow the same responsible lending laws as the big banks. This means they are legally required to ensure you can afford the loan without undue hardship. They are professional institutions overseen by the Financial Markets Authority, not unregulated private individuals.

Do non-bank lenders always have higher interest rates?

Most of the time, yes, interest rates from non bank lenders nz are higher than what you’ll find at a mainstream bank. This extra cost reflects the “risk premium” the lender takes on by being more flexible with their rules. However, the gap between bank and non-bank rates can fluctuate depending on the market and your specific situation. It’s the trade-off for getting a “yes” when a bank says “no.”

Can I use my KiwiSaver with a non-bank lender?

You can certainly use your KiwiSaver first-home withdrawal with most non-bank lenders. The process for withdrawing your funds is handled by your KiwiSaver provider and your lawyer; it doesn’t actually depend on who your mortgage is with. As long as you meet the standard criteria for a first-home withdrawal, those funds can be used as part of your deposit for an alternative home loan just like a bank loan.

What is the difference between a 2nd tier lender and a loan shark?

The difference is entirely about regulation and professional standards. A 2nd tier lender is a legitimate, registered financial institution that follows strict government rules and responsible lending laws. A “loan shark” is typically an unregulated person or business that charges illegal interest rates and uses predatory tactics. Non-bank lenders are reputable companies often funded by large wholesale investors and operate with complete transparency and legal oversight.

Can I move my mortgage from a non-bank to a main bank later?

Moving your mortgage back to a main bank is actually the goal for many of our clients. We call this the “stepping stone” strategy. Once you’ve built up more equity in your home or cleaned up your credit history with twelve to twenty-four months of perfect repayments, you’ll find that the big banks are much more likely to welcome you back. It’s a great way to secure a house now while planning for lower rates later.

Do non-bank lenders require a 20% deposit?

Not necessarily, as non bank lenders nz are often much more flexible with deposit sizes than the big four. While some might still look for 20 percent, others have options for those with smaller deposits, especially for first-home buyers. The exact amount you’ll need depends on the specific lender’s rules and the type of property you’re buying. They look at your overall financial health rather than just a single percentage.

What happens if a non-bank lender goes out of business?

If a lender closes down, your mortgage doesn’t just disappear, but it also doesn’t mean you have to pay it back instantly. Usually, your loan contract is simply sold to another financial institution. You would continue making your repayments as normal, just to a different company under the same terms you originally agreed to. Your home remains secure as long as you keep up with your regular mortgage payments.

Why was I declined by a bank but approved by a non-bank?

Banks use very rigid, automated systems that automatically decline anyone who doesn’t fit a perfect profile. If you have a unique income source, like being self-employed, or a small mark on your credit file, the bank’s computer often just says “no.” Non-bank lenders use human judgement to look at the story behind your numbers. They are willing to consider the context of your situation and find ways to make the loan work.