Residential Investment Property Loans NZ: The 2026 Investor’s Reference Guide

What if a “no” from your bank was actually the best thing that could happen to your property portfolio? Many Kiwi investors feel stuck right now, watching great opportunities pass them by because securing residential investment property loans NZ feels harder than ever. It’s incredibly frustrating when you know you have the equity to grow, but the calculations on a bank’s spreadsheet just won’t budge due to strict LVR restrictions and debt-to-income caps.

We agree that the current market requires more than just a standard application; it requires a genuine strategy. In this guide, we’ll show you how to navigate the 2026 lending landscape with confidence and professional insight. You’ll learn how to unlock your existing equity to fund your next purchase, even when mainstream banks say no, and how to structure your debt to make the most of the 100% interest deductibility rules. We’re going to break down the move toward second-tier lenders and interest-only options that can help you organise your finances to prioritise cash flow and long-term growth.

Key Takeaways

- Get a clear picture of the 2026 market and why a custom strategy for residential investment property loans NZ is the key to building real wealth.

- Learn how to work around the 30% deposit hurdle by unlocking the value already sitting in your current property.

- Explore the flexible options offered by second-tier lenders that often say “yes” when the big banks have too many rules.

- Discover how to structure your loans with interest-only periods to keep your cash flow healthy and make the most of tax benefits.

- Understand how an expert advocate can handle the hard work and negotiations to ensure you get the best possible outcome for your portfolio.

Exploring the NZ Residential Investment Landscape in 2026

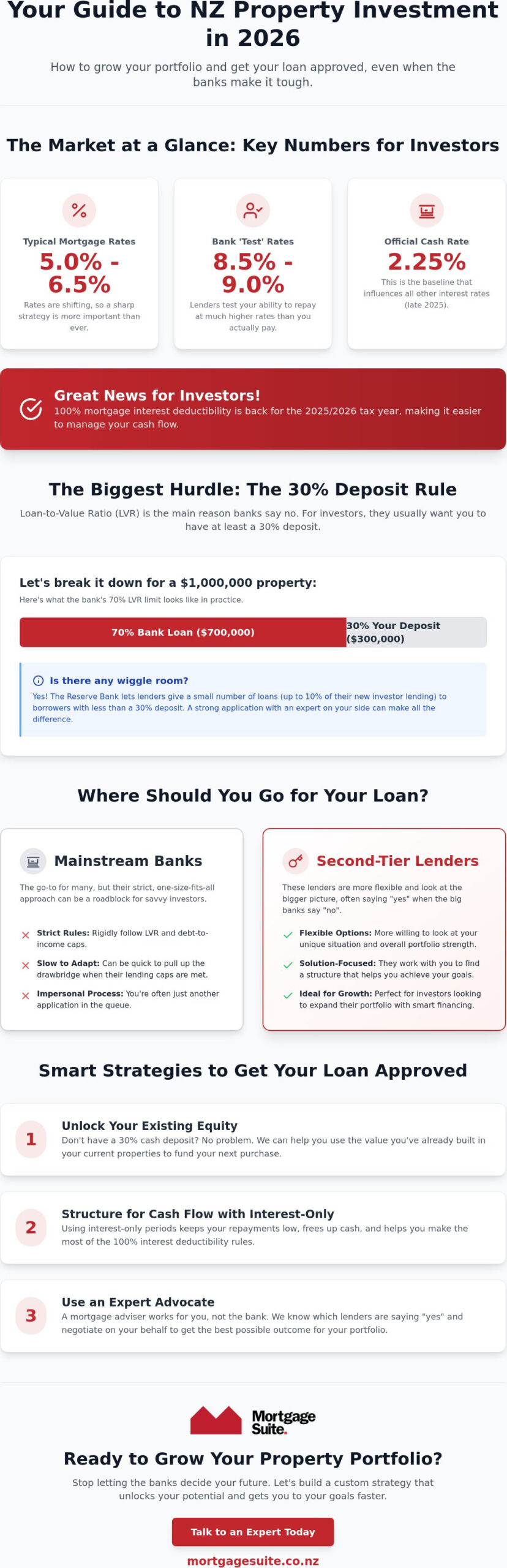

By 2026, the New Zealand property market has found its feet again, but it is certainly not the same game it was five years ago. Investors are now looking at residential investment property loans NZ with a fresh set of eyes. With the Official Cash Rate sitting at 2.25% in late 2025 and mortgage rates hovering between 5% and 6.5% for most of 2026, the “set and forget” mortgage is officially a relic of the past. Banks are constantly tweaking their appetites; one week they are hungry for new business, and the next, they have pulled up the drawbridge based on their internal caps.

The regulatory environment has also shifted significantly. For the 2025/2026 tax year, the return of 100% interest deductibility has breathed new life into the sector. This change makes it much easier to balance the books, especially for seasoned investors looking to expand their portfolios. However, you cannot just rely on the rules being in your favour. Success in this market requires staying ahead of fluctuating interest rates and understanding that bank criteria can change without warning. It is a more active, hands-on era for property owners.

Why Property Still Holds Its Value

Property remains a top choice for Kiwis building long-term wealth because it provides a tangible asset in an uncertain world. While we have seen plenty of headlines about the New Zealand property bubble, the underlying reality is a chronic shortage of quality housing in our major centres. Even when market conditions feel a bit patchy, the long-term capital growth trends across the country have historically rewarded those who stay the course.

- Capital Gains: Long-term value increases remain a primary driver for wealth building.

- Rental Yield: In 2026, many investors are prioritising higher yields to help cover bank test rates, which are currently sitting between 8.5% and 9%.

- Strategic Resilience: A well-chosen rental property provides a steady income stream and a hedge against inflation that other investments struggle to match.

The Role of Professional Advice

This is where having a seasoned pro in your corner makes all the difference. A standard bank manager is often just processing an application, but a long-term mortgage partner is looking at your entire financial future. Talking to a broker is spot on for those wanting to save time and avoid the stress of being declined by a mainstream lender. We know which banks are currently “open for business” for residential investment property loans NZ and which ones have tightened their belts.

We advocate for you to ensure you get a fair go from lenders. This might mean negotiating a discount on advertised rates; mortgage brokers in early 2026 were able to secure average discounts of around 0.13% on 6-month fixed terms. More importantly, we help you navigate the bridge between rigid institutional banking and your personal goals, making sure your loan structure works for you, not just the bank.

Decoding LVR Restrictions and Deposit Requirements for Kiwis

LVR is the percentage of a property’s value that you borrow, acting as a key risk measure for New Zealand lenders. For most people looking at residential investment property loans NZ, this three-letter acronym is the single biggest hurdle between them and their next title deed. While you might have bought your own home with a small deposit, the rules for rentals are historically much tighter. Banks generally view investment properties as slightly higher risk, which is why they ask you to have more skin in the game.

The “30% Rule” has been the standard for some time now. In simple terms, if you want to buy a rental, the bank usually wants you to provide 30% of the purchase price upfront. This ensures that even if the market takes a dip, the bank’s loan is well-covered. However, as of December 2025, there is a bit of breathing room. The Reserve Bank now allows banks to allocate up to 10% of their new investor lending to those with less than a 30% deposit. It isn’t much, but it means a “no” isn’t always final if your overall profile is strong.

How the 70% LVR Limit Works

Getting your head around the math is the first step. If you’re eyeing up a property worth $1 million, a 70% LVR limit means the bank will only lend you $700,000. You need to find the other $300,000 yourself. The Reserve Bank keeps these “speed limits” in place to prevent the economy from overheating and to protect the banking system from sudden shocks. If property values drop, a high LVR could mean you owe more than the house is worth. That is a position no investor wants to be in, so these rules actually provide a bit of a safety net for your portfolio.

Exemptions You Should Know About

Not every deal requires a massive cash deposit. The most common way around the 30% rule is the “New Build” exemption. To encourage more housing supply, the government often allows investors to get into brand-new properties with as little as a 20% deposit. This can be a game-changer for someone starting out. Another powerful strategy is using home equity for investment NZ. Instead of saving cash, you use the value built up in your own home to act as the deposit for the new rental.

You also need to consider your long-term hold strategy in light of the Bright-line test. While the rules have fluctuated, your intention for the property impacts how lenders view your stability. If you are feeling stuck on the numbers, we can help you work out your next move with a quick, no-pressure chat to see what is possible for your situation.

Mainstream Banks vs. 2nd Tier Lenders: Choosing Your Path

Most Kiwis grow up believing that the “Big Four” banks are the only place to go for a mortgage. While they are a solid choice for a standard home loan, they can be incredibly rigid when it comes to residential investment property loans NZ. These major institutions often use a “cookie-cutter” approach. If your financial situation doesn’t fit their specific mould, you might find yourself facing a flat refusal. In 2026, with Debt-to-Income (DTI) restrictions limiting high-debt lending, many investors are being turned away simply because they already have a few properties under their belt.

Being declined by a mainstream bank isn’t the end of your journey; it’s often just the beginning of a much better deal. This is where second-tier and non-bank lenders become a secret weapon for successful investors. These lenders aren’t just a backup plan. They are a strategic alternative for those who need a bit more flexibility than a traditional bank can offer. At Mortgage Suite, we specialise in non bank investment property loans NZ because we know that a “no” from a bank manager usually just means they don’t have the right product for your specific goals.

When the Bank Says No

There are plenty of reasons a bank might say no. Since July 2024, banks have been restricted in how much high-DTI lending they can do. For an investor in 2026, a DTI of 7 is considered high. If your total debt is seven times your gross annual income, a mainstream bank might struggle to approve you. Other common hurdles include being self-employed without two years of perfect tax records or trying to buy a non-standard property. Non-bank lenders take a more “human” approach to your numbers. They are legitimate, safe alternatives that look at the big picture rather than just ticking boxes on a spreadsheet.

Comparing Your Options

When you look beyond the big banks, you’re often trading a slightly higher interest rate for significantly more flexibility and speed. While a major bank might take weeks to process a complex investment application, a second-tier lender can often give you an answer in a matter of days. This speed can be the difference between securing a great deal and missing out entirely. We help you compare these options side-by-side. We’ll show you the true cost of the loan versus the potential growth of your portfolio, ensuring you get a fair go and a loan that actually helps you move forward.

Strategic Loan Structures: Interest-Only and Equity Unlocking

While everyone chases the lowest interest rate, savvy investors know that the way you set up your debt is what actually builds wealth. Choosing the right structure for your residential investment property loans NZ can be the difference between a portfolio that grows and one that stays stagnant. In 2026, the strategy is all about flexibility. With the 100% interest deductibility rules fully restored, many of our clients are opting for an interest only investment property loan nz to keep their monthly costs down and make the most of their tax benefits.

This approach allows you to focus your spare cash on paying down the mortgage on your own home first. It is a classic move that we often recommend because it puts money back in your pocket while your investment property hopefully gains value in the background. The goal is to make your money work harder for you, not the other way around. By only paying the interest, you’re keeping your outgoings low and your cash flow healthy, which is vital when bank stress tests are still quite high.

Unlocking Your “Lazy Equity”

Many people are sitting on a goldmine without even realising it. Equity is simply the difference between what your property is worth and what you owe the bank. You don’t always need a formal valuation to get a rough idea; looking at recent sales in your street is a great place to start. If your home is worth $1.2 million and your mortgage is $500,000, you have $700,000 in equity. Banks won’t let you use all of it, but they might let you borrow up to 80% of your home’s value to fund your next move.

The process of an equity release home loan NZ allows you to pull that value out and use it as a deposit for a rental. This means you can buy your next investment without needing to save a single cent in cash. It is the fastest way to scale your portfolio, provided you have the income to support the new lending. If you want to see how much you could potentially tap into, talk to us about your loan structure today to get a clear picture of your options.

Cash Flow Management Strategies

Managing a rental in 2026 isn’t just about collecting rent; you need to be smart with how that money moves. While interest-only loans are popular for their tax benefits, some investors prefer the traditional route of paying back the loan plus interest to slowly chip away at the debt. It really depends on whether you’re chasing immediate cash flow or long-term debt reduction. We also see a lot of success with offset accounts. By keeping your savings in an account linked to your loan, you only pay interest on the difference, which can save you thousands over the years.

Revolving credit is another handy tool for the modern investor. It acts like a giant overdraft, giving you instant access to funds when a great property deal pops up. Having these structures in place before you start house hunting means you can move quickly when the right opportunity arises. It is all about being organised and ready to strike when the market is in your favour with Mortgage Suite Ltd in your corner.

Securing Your Investment Loan with Mortgage Suite Ltd

Securing residential investment property loans NZ shouldn’t feel like a solo battle against a giant machine. When you work with Krish Krishna and the team at Mortgage Suite Ltd, you’re putting over 20 years of deep banking experience in your corner. We know exactly how the big lenders think because we’ve spent decades on the other side of the desk. This insider knowledge is what allows us to fight for your approval, finding the specific path that leads to a “yes” when other brokers might have already thrown in the towel. We don’t just fill out forms; we build a case for your success.

Our process is designed to take the weight off your shoulders. From that very first chat where we map out your goals, all the way through to the day the deal is finalised, we handle the heavy lifting. We don’t just want to get you a loan; we want to ensure it’s the right setup for your long-term wealth. We’re here to build a relationship, acting as your steady hand in a market that can sometimes feel quite unpredictable. Our commitment doesn’t end when the papers are signed; we stay in touch to ensure your finance structure still fits as your life and the market change.

The Mortgage Suite Ltd Advantage

What sets us apart is our ability to look beyond the standard bank offerings. We have access to a huge range of lenders, from the household names to specialist providers that many people don’t even know exist. This means we can find a home for almost any deal, no matter how complex your situation might seem. You’re never just a number to us. We treat every client as a partner, providing a personalised service that focuses on removing obstacles and creating a clear run toward your investment goals. We have a reputation for getting those tricky, non-standard deals across the line because we aren’t afraid to roll up our sleeves and negotiate hard on your behalf.

We act as a bridge between the rigid world of institutional banking and your personal needs. Our proactive attitude and dedication to overcoming challenges have made us a trusted mentor for investors across the country. Whether you’re dealing with self-employment income or a property that doesn’t fit the usual mould, we know how to present your story to the right lender to get the result you need.

Your Next Steps

Ready to see what is possible for your portfolio? To get the ball rolling, it helps to gather a few essentials. Having your income proof, current mortgage details, and a clear idea of your investment goals ready will make our first conversation even more productive. We invite you to book a consultation where we can look at your numbers and show you exactly how to grow your portfolio in 2026. It is about more than just a transaction; it is about setting you up for a future of financial freedom. Get started with Mortgage Suite Ltd and secure your investment future today and let’s turn your property plans into a reality.

Take the Next Step Toward Your Property Goals

Building a property portfolio in today’s market doesn’t have to be a stressful uphill battle. By now, you’ve seen that the right strategy for residential investment property loans NZ is about much more than just chasing the lowest interest rate. It’s about having the flexibility to move quickly, the insight to unlock your existing equity, and the grit to look beyond the big banks when their rigid rules don’t fit your situation. Whether you are a first-time investor or a seasoned pro, the key is to stay proactive and keep your loan structures working as hard as you do.

We’re here to help you navigate these choices with confidence and clarity. With over 20 years of banking and brokerage experience, we specialise in 2nd tier and alternative lending solutions that mainstream banks often overlook. We provide a nationwide service across New Zealand, ensuring every investor gets a fair go and a dedicated advocate in their corner. We know the hurdles, but we also know the way around them.

Your next investment is waiting, and we’d love to help you reach it. Talk to Krish and the team at Mortgage Suite to secure your investment loan today. Let’s get your financing sorted so you can focus on growing your wealth and securing your financial future. You’ve got the vision, and we have the expertise to help you make it happen.

Frequently Asked Questions

How much deposit do I really need for an investment property in NZ in 2026?

You generally need a 30% deposit for most residential investment property loans NZ. While the Reserve Bank allows banks to lend to a small number of investors with less than this, those spots are limited and usually go to the strongest applicants. If you are looking at a brand-new build, you can often still get started with a 20% deposit.

Can I use my KiwiSaver for an investment property loan?

No, you cannot use your KiwiSaver funds to purchase an investment property. KiwiSaver withdrawals are strictly reserved for buying your very first home to live in or for your retirement. However, once you’ve used KiwiSaver to get into your first home and built up some equity, you can eventually use that equity as a deposit for a rental.

What is a 2nd tier lender and are they safe for property investors?

A second-tier lender is a non-bank financial institution that offers property loans outside the traditional “Big Four” banks. They are a perfectly safe and regulated alternative for Kiwis. These lenders often have more flexible criteria, making them ideal for investors who might be self-employed or have complex income structures that mainstream banks struggle to process.

How does the Bright-line test affect my investment loan decision?

The Bright-line test affects your tax obligations rather than the loan itself, but it’s a vital part of your long-term strategy. It determines whether you’ll pay tax on any profit if you sell the property within a certain timeframe. Lenders will want to see that you have a stable plan for the property, as your intention to hold or sell can impact your overall financial position.

Can I get an interest-only loan for my residential investment property?

Yes, interest-only terms are a very common choice for residential investment property loans NZ in 2026. Because 100% of the interest is now tax-deductible for the 2025/2026 tax year, this structure helps you maximise your cash flow. Most lenders will offer interest-only periods for up to five years, though some specialist lenders can provide even longer terms.

What is the maximum LVR for an investment property in New Zealand?

The standard maximum LVR for an existing investment property is 70%, meaning you need a 30% deposit. If you’re buying a new build, the maximum LVR often increases to 80%, allowing you to get in with a 20% deposit. Banks are restricted by “speed limits” that cap how much high-LVR lending they can do each month.

How do I calculate how much equity I can use for a new loan?

You can usually use up to 80% of your current home’s value, minus your existing mortgage. For example, if your home is worth $1 million and you owe $500,000, 80% of the value is $800,000. Subtract your $500,000 mortgage, and you have $300,000 in usable equity. This amount can act as the 30% deposit for a new $1 million investment property.

What should I do if my bank declines my investment property loan application?

Don’t assume a “no” from your bank is the end of the road. Banks often decline applications because of rigid internal rules or high debt-to-income ratios, which currently sit at a cap of 7 for most investors. Your next step should be to look at non-bank lenders who take a more personal approach to your numbers and can often find a way to say “yes”.