Commercial Property Refinance NZ: Your 2026 Guide to Unlocking Equity and Better Rates

What if the bank’s “no” isn’t actually a dead end, but a sign that your current loan has simply outgrown your business? Many Kiwi property owners feel stuck with high interest rates or rigid terms that were set years ago. It’s draining to feel like your growth is being held back by a lender who doesn’t understand your vision, especially when you’re trying to make sense of complex terms like repayment safety margins or loan-to-value limits. You deserve a financial partner who sees the potential in your portfolio rather than just the risks on a spreadsheet.

Securing a commercial property refinance NZ wide is about more than just finding a cheaper rate; it’s a strategic reset to align your debt with your 2026 goals. In this guide, you’ll learn how to restructure your debt to release equity for expansion and take advantage of the current 2.25% base interest rate environment. We’ll walk through how to navigate the latest financial regulations and show you how to trade cold, corporate interactions for a lending relationship that actually supports your long-term success. Whether you’re looking to lower your monthly repayments or access a lump sum for your next big move, we’ve got the roadmap to get you there.

Key Takeaways

- Discover how a commercial property refinance NZ wide can help you break free from rigid bank structures and align your debt with your 2026 business goals.

- Learn how to identify and unlock “lazy” equity in your property to fund your next stage of growth or expansion.

- Compare the strict criteria of mainstream banks against the flexible, fair dinkum alternatives offered by 2nd tier lenders across New Zealand.

- Get a clear roadmap for your refinance journey, from gathering your financial documents to securing a fresh valuation that reflects your asset’s true value.

- Understand the value of having a dedicated advocate from Mortgage Suite Ltd who uses decades of industry experience to negotiate better terms on your behalf.

What is commercial property refinance and why consider it in 2026?

Refinancing is essentially the process of replacing your current commercial loan with a fresh one, often from a new lender who offers better terms. Think of it as a tactical move to improve your financial position or fuel business expansion. In the current market, many Kiwi business owners are finding that the “big four” banks have become a bit too rigid with their lending criteria. By looking at a commercial property refinance NZ wide, you can move away from those strict boxes and find a debt structure that actually breathes with your business.

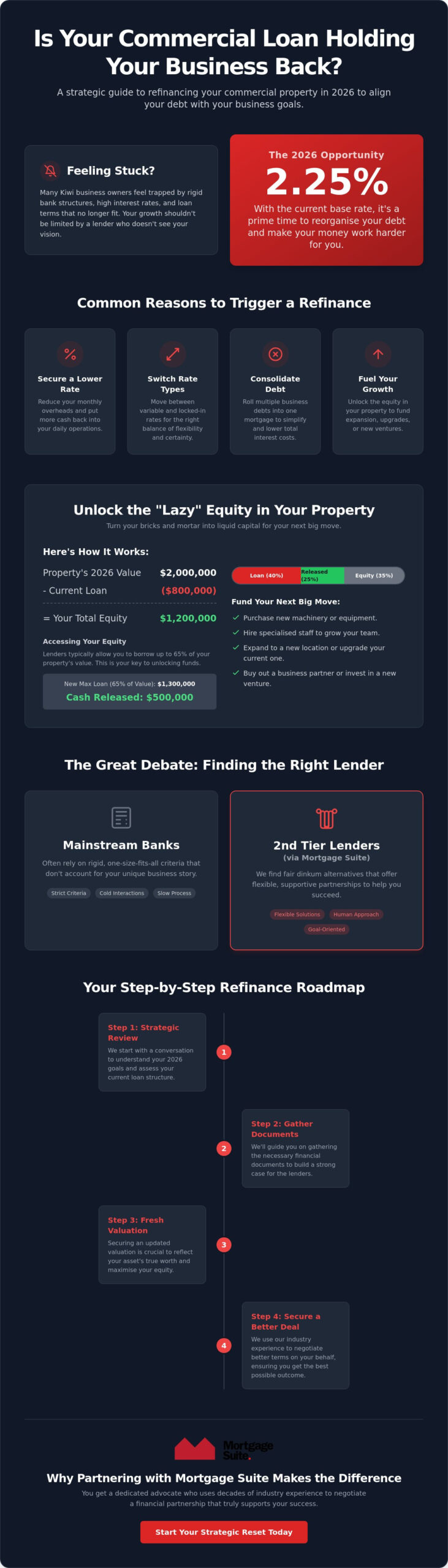

To understand the basics, you might ask, what is a commercial mortgage and how does it differ when you’re swapping lenders? While the underlying asset stays the same, the rules of the game change based on the lender’s appetite for risk and their current interest rates. With the Reserve Bank’s base rate sitting at 2.25% in mid-2026, it’s a prime time to reorganise your debt to better suit your current cash flow needs. It’s about making your money work harder for you, rather than just serving the bank’s requirements.

Common reasons to trigger a refinance

Most people start looking at their options when they feel they’re paying too much or when their business needs have shifted. Here are the main drivers we see in the 2026 landscape:

- Securing a lower interest rate: This is the most common reason. Reducing your monthly overheads puts more cash back into your daily operations.

- Switching interest rate types: You might want to move between variable vs locked-in interest rates to find the right balance of flexibility and certainty based on current market trends.

- Debt consolidation: You can often roll various business debts into one single commercial mortgage. This simplifies your life and usually lowers your total interest costs significantly.

Refinance vs. New Loan: What is the difference?

You might think a refinance is just as much hassle as buying a new property, but that’s rarely the case. Because you already own the asset, the assessment process can often be much faster than a new purchase. Lenders already have a track record of the property’s performance to look at. However, you do need to weigh up the costs for ending a contract early, often called break fees. We often find that if the long-term savings on a lower interest rate outweigh that initial cost, it’s a very smart move.

Your property’s updated 2026 valuation plays a massive role here too. If your building is worth more now than when you first bought it, your equity has grown. This updated value gives you much more leverage when talking to a commercial property refinance NZ specialist at Mortgage Suite Ltd, as it lowers the lender’s risk and can unlock better pricing tiers that weren’t available to you before.

Unlocking the goldmine: Using equity release for business growth

Your commercial property is more than just a place for the team to work or a spot to store your inventory. If you have owned your building for a few years, there is a good chance it is sitting on a pile of what we call “lazy” equity. Choosing a commercial property refinance NZ wide allows you to tap into that increased value, effectively turning your bricks and mortar into liquid cash. You are essentially replacing your current loan with a larger one and using the difference to fund your next big move, whether that is a new location or a major upgrade.

Using the value in your property is often the most cost-effective way to fund a new business venture because interest rates backed by property are almost always lower than other types of finance. This capital works as a brilliant small business loan NZ alternative, giving you the funds you need for new machinery, hiring specialized staff, or even buying out a business partner. By leveraging an asset you already own, you avoid the high costs and strict terms often found with unsecured business credit lines.

Calculating your usable equity

Lenders decide how much you can borrow based on the percentage of the property’s total value. In the 2026 market, a solid rule of thumb is that most lenders will let you borrow up to 60% or 65% of what the building is currently worth. However, not every property is treated the same. While a standard office or warehouse is usually straightforward, specialised buildings like medical centres or cold storage units might have slightly tighter limits.

According to insights from the Property Institute of New Zealand, professional valuation trends are vital because a fresh appraisal can often reveal far more equity than you might have estimated yourself. You could even use this extra cash to fund the deposit for a residential investment property, allowing you to grow your personal wealth alongside your business without having to save a fresh deposit from your daily cash flow.

Servicing the new debt

While having equity is a great start, you also need to prove that your business can handle the larger repayments. Lenders will look closely at how well your profit covers your interest payments. Simply put, they want to see a healthy safety margin where your business income is significantly higher than the cost of the loan. They aren’t just looking at the building; they are looking at the health and sustainability of the business operating within it.

Most traditional banks prefer to see two years of steady, healthy profit in your financial records. If your recent history has been a bit more varied due to growth or market shifts, some lenders can be more flexible, provided you can show a clear plan for how the released cash will drive your future income. If you are wondering how much your specific property could unlock for your business, it is worth having a chat with the team at Mortgage Suite Ltd to see what is possible for your situation.

The Great Debate: Mainstream banks vs. 2nd tier lenders

Choosing between a mainstream bank and a non-bank lender is one of the most important decisions you’ll make when looking at a commercial property refinance NZ wide. Mainstream banks are often the first port of call because they offer the lowest interest rates. However, they can be incredibly fussy about your financial history. If your business doesn’t fit into their narrow “perfect” box, you might find yourself facing a frustrating rejection. This is where a 2nd tier lender New Zealand owners trust comes into play. They offer a fair dinkum alternative by looking at the bigger picture of your business potential rather than just ticking boxes on a checklist.

The landscape for a commercial mortgage New Zealand wide has evolved significantly by 2026. Non-bank lenders are no longer just a “last resort” for those with bad credit. They’ve become highly competitive, offering tailored solutions that the big banks simply aren’t set up to handle. For many, refinancing to a non-bank is a strategic bridge that helps them navigate a period of rapid growth or a temporary dip in cash flow without the rigid constraints of traditional banking.

When to choose a non-bank refinance

There are several scenarios where a non-bank lender is actually the better choice for your commercial property refinance NZ project:

- Colourful financials: If you have a short trading history or your most recent tax returns don’t show the full strength of your business yet, a non-bank lender is much more likely to listen to your story and understand your future projections.

- Need for speed: Big banks are notorious for taking weeks, or even months, to make a decision. If you need to move fast to secure a time-sensitive opportunity, a 2nd tier lender can often provide an answer and the funds in a matter of days.

- Protecting your home: Many banks insist on “cross-collateralisation,” which means they use your family home as security for your business loan. Refinancing away from the bank can help you untangle these assets and keep your personal life separate from your business risks.

The path back to the bank

One thing many people don’t realise is that a non-bank loan doesn’t have to be a permanent fixture. We often view it as a temporary solution for 12 to 24 months. During this time, you can focus on stabilising your financials and building the “clean” track record that mainstream banks love. Once your business has matured and your books look more traditional, you can “graduate” back to a mainstream bank to secure those lower long-term rates. Having a seasoned advisor in your corner makes this transition much easier, as we know exactly what the big banks need to see before they’ll welcome you back. It’s about playing the long game to get the best result for your business.

Your step-by-step roadmap to a successful refinance

Getting your commercial property refinance NZ project across the line doesn’t have to be a headache if you follow a clear path. By 2026, the lending environment has become more nuanced, requiring a bit more preparation than a standard residential top-up. The first step is always to gather your “ducks in a row.” This means having at least two years of clean financial statements, including profit and loss reports and balance sheets, alongside your current loan details. Lenders want to see that your business is stable and that you’ve been a reliable borrower so far.

Once your paperwork is sorted, the process typically follows this sequence:

- Get a fresh valuation: With total commercial sales activity increasing by approximately $131 million in recent years, your property’s 2026 value is likely much higher than your last bank assessment.

- Compare lender appetite: Not every lender wants to fund a suburban retail block or a large industrial warehouse. We help you find the one whose current “appetite” matches your specific asset type to ensure a higher chance of approval.

- Negotiate the fine print: This is where we look at the General Security Agreements (GSA) and ensure the terms don’t pull your other business assets into the mix unnecessarily.

- Settlement: Your lawyers will coordinate with the new lender to pay off your old debt. From here, your new journey with better rates or extra capital begins.

Navigating the valuation process

One common trap is thinking you can use a simple residential “app” estimate for a commercial deal. Commercial valuations are far more complex. The valuer will look closely at your “yield” and “cap rates,” which are essentially ways of measuring the property’s income potential against its market risk. If you have strong tenants on long-term leases, your valuation will likely be much stronger. It’s a good idea to tidy up the building and ensure all maintenance records are up to date before the valuer arrives. A well-presented property suggests a well-managed business, which gives the bank more confidence during the commercial property refinance NZ process.

Negotiating the “hidden” terms

It is a mistake to focus solely on the interest rate. While the 2.25% OCR has kept base rates attractive, banks often hide extra costs in “line fees” or strict “covenants.” Covenants are the rules you must follow, such as maintaining a certain level of profit. If these are too tight, they can stifle your growth. We often work to get application fees reduced or waived entirely, and we structure the loan to ensure you have the flexibility to make changes later without being hit by more charges. If you want someone to handle these tricky negotiations for you, reach out to Mortgage Suite Ltd to start your roadmap today.

Why partnering with Mortgage Suite makes the difference

When you are looking to secure a commercial property refinance NZ wide, having the right person in your corner changes everything. Krish Krishna and the team at Mortgage Suite bring over 20 years of deep banking experience directly to your side of the table. We reckon every business owner deserves an advocate who speaks the bank’s language and knows exactly how to navigate their internal systems. Instead of you spending hours on hold or deciphering complex credit policies, we handle the heavy lifting of the application. This leaves you free to stay focused on what really matters; looking after your customers and growing your business.

Our expertise isn’t limited to one specific sector. Whether you are managing a large industrial warehouse, a bustling retail suite, or a specialised medical facility, we know how to present your case. We understand the nuances of the 2026 market and how to highlight the strengths of your property and business cash flow to get the deal sorted. We don’t just submit papers; we tell your story in a way that makes lenders want to say yes.

A personal approach to business finance

We are not a “set and forget” brokerage that disappears once the loan is settled. We are here for the long haul, acting as a steady hand as your business evolves. Our reputation as dedicated negotiators helps us find the “green light” for complex deals that other brokers might find too difficult. We specialise in those “out of the box” scenarios that mainstream banks often struggle with, using our industry connections to find flexible solutions that align with your specific goals. If there is a way to make the numbers work, we will find it.

Ready to chat about your options?

The first conversation you have with us is always free and completely confidential. We take the time to listen to your 2026 goals and look at your current debt structure to see if there is a better deal waiting for you. There is no pressure and no confusing jargon; just honest, professional advice from people who have seen every possible scenario. Let’s see how a commercial property refinance NZ could unlock new opportunities for your portfolio. Get in touch with Mortgage Suite today to explore your refinance options and start your next chapter with confidence.

Ready to unlock your property’s true potential?

The 2026 market offers a unique window to turn your commercial asset into a springboard for future success. Whether you’re looking to lower your overheads or tap into equity for a new venture, a commercial property refinance NZ project gives you the control back. You don’t have to stay stuck with a lender who doesn’t see your vision or understand your specific industry needs. Refinancing is your chance to reset the terms and ensure your debt is working for you, not the other way around.

At Mortgage Suite, we bring over two decades of banking and brokerage expertise to ensure you aren’t just another number in a system. We specialise in finding the right path, whether that’s with a mainstream bank or a flexible 2nd tier lender who can move as fast as you do. Our team acts as your personal advocate, handling the tricky negotiations and paperwork so you can get back to what you do best. We believe in building long-term partnerships based on trust and real results.

If you’re ready to see what’s possible, book a free refinance strategy session with Krish and the team today. We’ll look at your goals and find a solution that fits your business perfectly. It’s time to move forward with a financial partner who is as committed to your success as you are.

Frequently Asked Questions

Is it harder to refinance commercial property than a residential home?

It is generally more complex because lenders look at the strength of your business and the quality of your tenants rather than just your personal income. While a home loan is based on a standard set of rules, commercial deals are assessed on their individual merits. This requires more detailed paperwork and a deeper look at your long-term stability, lease agreements, and the specific industry you operate in.

How much equity can I pull out of my commercial property in NZ?

Most lenders in the current market will allow you to borrow up to 60% or 65% of the property’s total value. If your property is worth more now than when you bought it, you can use a commercial property refinance NZ project to access that extra cash for business growth. This is a great way to fund expansion or new investments, provided your business can comfortably service the larger loan.

What are the typical break fees when refinancing a commercial loan?

Break fees vary between lenders, but you might see a flat fee around $33 or a calculation based on 30 days of interest. It is important to ask your current bank for a specific “break cost” quote before you switch. This helps you determine if the long-term savings from a lower interest rate will outweigh the immediate cost of leaving your current contract early.

Can I refinance if my business has had a “tough” year financially?

You certainly can, though you may need to look beyond the mainstream banks for a solution. If your most recent tax returns show a dip in profit, a non-bank lender will often look at your overall track record and future projections rather than just your last 12 months. This “big picture” approach is a great way to secure the funding you need while your business gets back on its feet.

How long does the commercial refinance process actually take?

You should typically allow between four and eight weeks from your first conversation to the final settlement. While some 2nd tier lenders can move much faster if you have all your documents ready, the process involves valuations and legal checks that take time to get right. Starting the process early ensures you aren’t rushed into a deal and gives us plenty of time to negotiate the best terms.

Do I need a new valuation when I refinance my commercial property?

Yes, almost every lender will require a fresh valuation to confirm the property’s current market value. Since the 2026 lending landscape relies heavily on accurate data, a new report ensures the bank is comfortable with the loan amount. It also gives you the best chance of unlocking the maximum amount of equity if the property has increased in value since you first took out your loan.

What is an “Interest Cover Ratio” and why does it matter for my refinance?

This is a tool lenders use to see if your business makes enough profit to pay the interest on the loan several times over. They want to see a safety margin so that even if your income drops slightly, you can still meet your repayments. A strong ratio makes you a much more attractive borrower and can often lead to more competitive interest rates and better terms.

Can I refinance a commercial property that has a vacant tenancy?

It is possible, but it usually requires a specialist lender who understands your specific market. Mainstream banks generally prefer properties with consistent income from long-term leases. If you have a vacancy, we can often find a commercial property refinance NZ solution that provides a bridge until you find a new tenant. Once the building is full again, we can then look at moving you back to a traditional bank.