Subdivision Finance NZ: Your 2026 Guide to Funding Your Land Project

What if the “No” you just received from your bank is actually the best thing that could happen to your development? It’s a common story in the 2026 market. You have the land and the vision, but the big banks are tightening their belts and drowning you in talk of pre-sales and drawdowns. Securing subdivision finance nz doesn’t have to be a roadblock that stops your project before the first spade hits the dirt.

Most landowners find the process of funding a project incredibly stressful, especially when faced with hidden civil costs and confusing council fees. We agree that it’s a lot to handle on your own. This guide promises to give you the clarity you need to move forward with confidence. You’ll discover how to bypass mainstream bank hurdles, understand the non-bank options available to you, and learn the best ways to maximise your profit in this changing regulatory environment. We will walk you through the entire path from your initial application to the final settlement, ensuring you have a steady hand to guide you.

Key Takeaways

- Understand why a standard home loan won’t work for development and how the right funding structure turns one piece of land into multiple titles.

- Compare the major banks with private lenders to find a path that avoids endless red tape and keeps your project moving.

- Uncover the hidden costs like council fees and civil works that you must account for when securing subdivision finance nz.

- Learn how to build a rock-solid case for approval by focusing on the one document every lender considers a “must-have.”

- Discover how professional negotiation and years of banking experience can help you bridge the gap between a “no” and a successful project.

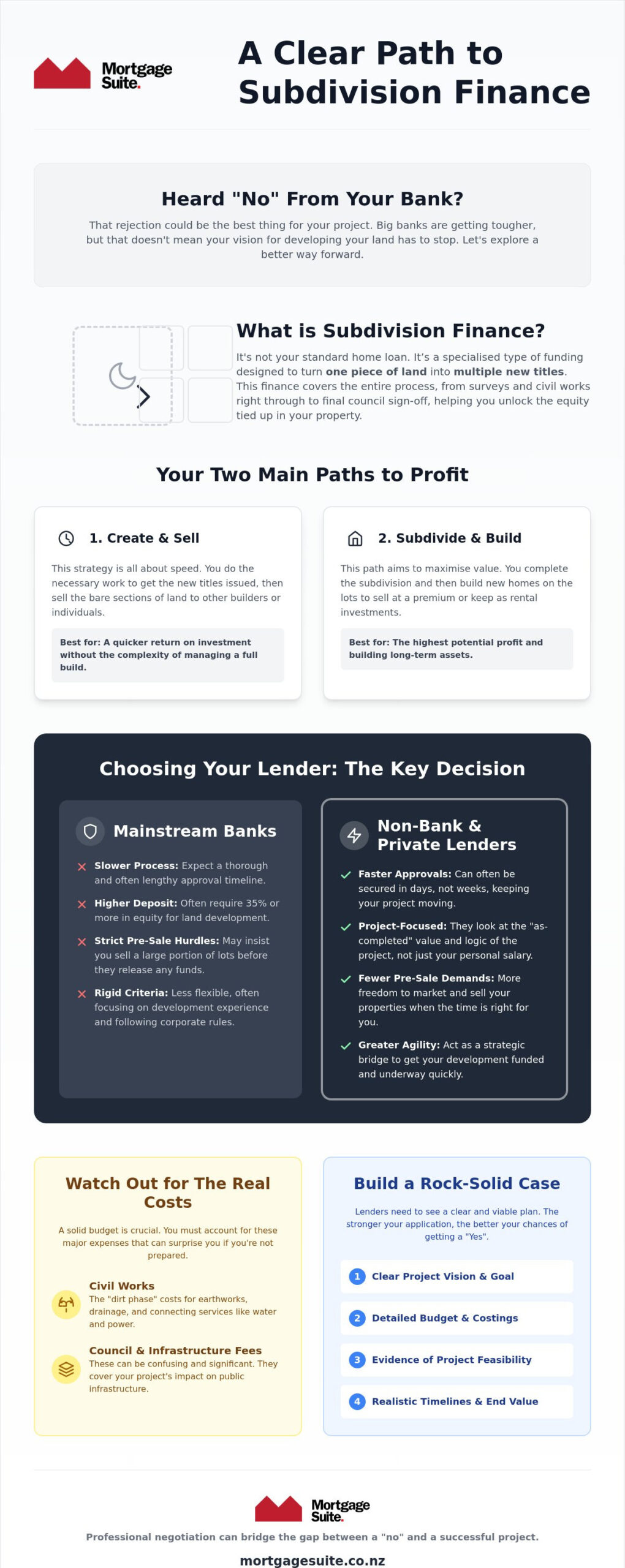

What is Subdivision Finance and Why Does it Matter?

Think of subdivision finance nz as the specialised engine that powers your project from a simple idea to a profitable reality. It isn’t just a standard mortgage with a different name. This is a specific type of funding designed to handle the transition of one piece of land into multiple legal titles. While your everyday home loan is great for buying a finished house, it isn’t built to handle the complexities of a development site. You need money that works as hard as you do, covering everything from the first survey to the final council sign-off.

The goal here is simple: you want to unlock the equity sitting in your land. By dividing the property, you create new assets that didn’t exist before. This process, formally known as Subdivision (land), requires a lender who understands that you aren’t just buying a home; you’re running a business venture. The right subdivision finance nz package stays with you through the “dirt” phase, the civil works, and right up until you receive your Statement of Compliance from the local council.

The Two Main Ways to Profit from Your Land

Most of our clients choose one of two paths. The “Create and Sell” strategy is popular because it’s often faster. You do the work to get the new titles and then sell the bare land to someone else. It’s a great way to get a quick return without the stress of a full build. On the other hand, the “Subdivide and Build” strategy offers the most long-term value. You keep the land, build new homes, and either sell them for a premium or keep them as rentals. Because these paths have different risks and timelines, the type of loan you need will change depending on your final goal.

Why Your Current Bank Might Say No

It’s incredibly frustrating to be turned down by a bank you’ve been with for years. Mainstream banks often see vacant or “unimproved” land as a high-risk gamble. They might demand that you have years of development experience or insist on pre-sales before they’ll even look at your application. If you find yourself hitting a brick wall, it’s time to look at 2nd tier lender New Zealand options. These lenders are often more interested in the actual feasibility of your project than just following a rigid set of corporate rules. Having this backup plan ensures your project doesn’t stall just because a big bank didn’t see the potential you do.

Bank Loans vs. Non-Bank Lenders: Choosing Your Path

Deciding where to source your capital is the most critical choice you’ll make for your development. While many Kiwis naturally head to the “Big Four” banks first, the 2026 lending landscape for subdivision finance nz is much broader than it used to be. The right choice depends entirely on your timeline, your cash flow, and how much “red tape” you’re willing to handle. While banks offer the most attractive interest rates on paper, their rigid criteria can often stall a promising project before it even gets off the ground.

Non-bank lenders, on the other hand, operate with a different level of flexibility. They tend to focus on the logic of the project itself rather than just your personal salary or background. This shift in focus is why many successful developers use alternative funding to keep their projects moving when a traditional bank says no. 2nd tier lending acts as a strategic bridge for developers who need speed and fewer pre-sale hurdles to reach their goals.

The Mainstream Bank Approach

If you choose a traditional bank, you should expect a thorough and often slow process. Banks typically demand significantly higher deposits for land development, often asking for 35% or more in equity. Their biggest hurdle is the “pre-sale” requirement. A bank might insist that you sell a large portion of your lots before they release any funds. This cautiousness stems from the complex legal requirements found in the Resource Management Act 1991, as banks want to be certain the project is financially viable before they take on the risk.

The Non-Bank and Private Advantage

Non-bank and private lenders offer a level of agility that mainstream banks simply can’t match. Approvals can often be secured in a matter of days rather than weeks, which is vital when you’re trying to settle on a property or start civil works. These lenders often look at the “as-completed” value of your project. Instead of just looking at what the dirt is worth today, they consider the value of the new titles you’re creating. This approach, combined with fewer pre-sale requirements, allows you to market your property when the timing is right for you, not just when the bank says so. If you’re unsure which route fits your specific project, the team at Mortgage Suite Ltd can help you weigh up these options to find the most profitable path forward.

The Real Costs: Infrastructure, Fees, and the ‘Money Pit’

On paper, turning one lot into two or three looks like a guaranteed win. However, the reality of subdivision finance nz is that the most significant costs often hide beneath the surface. It isn’t just about the purchase price; it’s about the “hard costs” that turn a piece of dirt into a buildable site. Many first-time developers are caught off guard by the sheer scale of investment required before a single house frame even goes up. This is where a project can easily become a “money pit” if you haven’t planned for the specific expenses that councils and contractors will demand.

Because these costs are so front-heavy, property development loans NZ are structured differently than a standard mortgage. Instead of getting all the money at once, you use “progressive drawdowns.” This means your lender releases funds in stages as you hit specific milestones, such as completing the drainage or finishing the roading. We always recommend setting aside a contingency fund of at least 10% to 15% of your total budget. Whether it’s hitting unexpected rock during excavation or a sudden change in council requirements, having that buffer prevents your project from grinding to a halt.

Council Fees and Civil Works

In 2026, council fees remain a major hurdle. In Auckland, for example, development contributions can range from approximately $20,400 to $49,000 per new lot depending on the area. You also have to account for the Watercare infrastructure growth charge, which is now roughly $29,300 per unit. These “entry fees” simply give you the right to subdivide. On top of that, you must pay for the physical work to connect every new lot to power, water, and sewage. These civil works are often the biggest drain on your cash flow, but they are essential for creating a valuable asset.

Managing Your Cash Flow During the Build

One of the best ways to protect your sanity during a project is through “capitalised interest.” This is a common feature in subdivision finance nz where the interest payments are added to the loan balance instead of you paying them out of your pocket every month. It keeps your cash free for the actual work. To make sure everything stays on track, lenders often use a Quantity Surveyor (QS) to check the progress. The QS visits the site, confirms the work is done, and gives the green light for the next drawdown. If you find a perfect new site while your current project is still finishing, you might consider bridging finance nz to secure the next opportunity without waiting for your current lots to settle.

The Approval Checklist: What Lenders Need to See

Getting a “yes” for subdivision finance nz isn’t just about owning a great piece of land. It’s about showing you have a solid plan to turn that dirt into a profit. Lenders are naturally a bit cautious, and they want to see that you have done your homework before they hand over any money. You need to put together a professional package that shows you understand the risks and have a clear way to handle them. A lender’s confidence is built on the strength of your planning, not just the size of your property.

Before you pick up the phone to talk to a broker, start gathering your essential papers. This includes your personal money statements, a clear copy of your ownership papers, and any letters you’ve had from the council about planning permission. Having these ready to go shows that you are a serious developer who understands the process. It makes the whole conversation much smoother from the very first day.

Proving the Project Works (The Feasibility)

Your feasibility study is the most important part of your toolkit. It is basically the story of how your project will actually make money. It needs to break down every single cost, what you expect to sell the new lots for, and your final profit. One common mistake is being a bit too optimistic about those final sale prices. If your numbers look too high compared to what’s actually selling nearby, a lender will lose trust in your whole plan. You also need to account for GST, which can take a big bite out of your budget if you haven’t planned for it properly.

Your Experience and Your Team

If this is your first time doing a project like this, don’t worry. You can use the experience of your team to reassure the lender. Having a seasoned planner or a project manager with a great track record makes a massive difference to your application. Lenders also look much more favourably on projects that have fixed-price contracts for the work in the ground. This locks in your costs and prevents the “money pit” scenario we talked about earlier. Securing subdivision finance nz is much easier when you have a specialist broker to help package your story. If you’re ready to get moving, reach out to the team at Mortgage Suite Ltd to see how we can help you secure the funding you need.

How Mortgage Suite Ltd Navigates the Subdivision Maze

Krish Krishna brings over 20 years of big bank experience to your side of the table. It is your secret weapon when you are talking to lenders. When you are dealing with the tricky world of subdivision finance nz, you don’t just need someone to fill out forms. You need a veteran who knows exactly how those big banks think and what they want to see in a successful plan. Mortgage Suite Ltd acts as a bridge between your vision and the money needed to build it. Our goal is to take the stress out of the money side of things, especially when the usual banks make it feel like you are hitting a brick wall.

We believe in a partnership that stays away from confusing business talk. You won’t find us using complex terms that make your head spin. Instead, we focus on clear, honest chats about what your project needs to get across the finish line. Because we have built strong connections all over New Zealand, we can find private funding options that you won’t find by just walking into a local branch. We know which lenders are actually looking for development projects right now, which saves you a lot of time and hassle.

A Personal Approach to Complex Finance

At Mortgage Suite Ltd, we don’t just “process” paperwork. We mentor you through the whole process of getting your loan. Whether you are in a big city or a smaller regional centre, our national reach means we help Kiwis everywhere unlock what their land is worth. We handle those tough talks with lenders so you don’t have to. If a lender has questions about your timeline, we are the ones who step in and stick up for you. We use our reputation to find solutions that keep your project moving and protect your profit. You are never just a number to us; you are a partner whose success is our priority.

Getting Started with Mortgage Suite Ltd

The first step is always the easiest. It starts with a simple, friendly chat to see if your project has “legs.” We will listen to your goals and help you decide which path makes the most sense for you. From there, we help you get your plan and your team organised so you have the best shot at getting a “yes.” We know exactly what lenders need to see to feel good about your project. Ready to see what your land is really worth? Let’s chat about your subdivision goals today.

Ready to Unlock Your Land’s Potential?

Turning a single plot of land into multiple titles is a major project, but it remains one of the most effective ways to build wealth in the 2026 market. Success depends on choosing the right path between traditional banks and more agile non-bank lenders. You now understand the need to account for those hidden infrastructure costs and why a rock-solid feasibility study is your best tool for approval. Getting the right subdivision finance nz is the foundation for your entire project.

With over two decades of banking and brokerage experience, Krish Krishna and the team are ready to help you move forward. We specialise in 2nd tier and non-bank lending solutions that often provide the flexibility you won’t find on the high street. Our national service covers all of New Zealand, ensuring you have a seasoned mentor by your side regardless of where your land is located. We handle the tough negotiations so you can focus on the build.

Don’t let red tape or a bank’s “no” stop your progress. Book a consultation with Krish and the team at Mortgage Suite today. We are here to help you turn your vision into a profitable reality.

Frequently Asked Questions

Can I get a land development loan if I’ve been declined by my bank?

Yes, you absolutely can. Traditional banks often have very narrow “boxes” that many profitable projects simply don’t fit into. We specialise in connecting developers with 2nd tier and private lenders who prioritise the actual feasibility and logic of your project over a rigid computer-generated credit score. If your land has value and your plan is solid, there is almost always a funding path available.

How much deposit do I need for a subdivision in New Zealand?

While mainstream banks typically ask for a deposit of 35% or more, non-bank options can be much more flexible. These lenders often look at the “as-completed” value of your project rather than just the current price of the land. This means if you already own the property, the equity you’ve built up over time could potentially cover the entire deposit for your civil works.

What are ‘pre-sales’ and do I always need them to get funding?

Pre-sales involve selling your new lots to buyers before the final titles have been issued. Big banks often demand these to prove there is a market for your project before they release any funds. However, many private lenders don’t require them at all. This gives you the freedom to finish the project first and sell when the market is stronger, potentially increasing your final profit margin.

Can I use the equity in my current home to fund a subdivision?

Yes, using the equity in your existing property is one of the most common ways to kickstart a development. By securing your subdivision finance nz against your home, you can often access the cash needed for those early council fees and civil works. It’s a smart way to get the project moving without needing to have a large amount of cash sitting in the bank.

How long does it usually take to get subdivision finance approved?

If you are working with a non-bank or private lender, you can often get an approval in just a few days. Mainstream banks are much slower and can take several weeks to process the same application because of their internal red tape. Speed is often vital when you are trying to secure a site or book a contractor who has a limited window of availability.

Is it better to subdivide and sell bare land or build houses first?

The best choice depends on your personal goals and your tolerance for risk. Selling bare land is generally faster and requires less capital, which makes it a lower-risk option. Building houses on the new lots involves more work and a longer timeline, but it usually offers a significantly higher profit. We can help you look at the numbers for both strategies to see which fits your situation.

What happens if my infrastructure costs go over budget?

If you hit an unexpected hurdle that pushes costs up, the first step is to talk to your lender immediately. This is why we build a contingency buffer into your initial budget. If you’ve already used that buffer, we can often negotiate a “top-up” or look at alternative subdivision finance nz options to ensure the project reaches completion. The key is having a specialist who can manage those tough conversations for you.

Do I need to pay the loan back monthly while the subdivision is happening?

Not necessarily. Many development loans offer “capitalised interest,” which means you don’t have to make monthly repayments while the work is being done. The interest is simply added to the total loan balance and paid back in full once the new lots are sold and settled. This is a huge help for your cash flow, as it keeps your money free for the actual development costs.