Declined by the Bank for a Home Loan in NZ? Your 2026 Recovery Guide

You’ve spent months skipping the extras and watching your savings grow, only to have a single email turn your home-buying dreams upside down. It’s a gut-wrenching moment when you realise you’ve been declined by bank home loan NZ lenders, especially when the Reserve Bank’s 2.50% OCR hike and strict debt-to-income limits make the goalposts feel like they’re constantly moving. The big banks are operating with more “computer says no” logic than ever before, leaving many great borrowers feeling stuck in the dark.

We know how confusing and unfair this feels, but a rejection from a main bank isn’t a dead end. This guide will show you exactly how to navigate the current market, from understanding why the banks are so rigid to finding alternative lenders who look at your real-life situation rather than just a spreadsheet. You’ll discover a clear path to approval and the confidence to try again with a much stronger strategy that works for the 2026 landscape.

Key Takeaways

- Understand why automated bank systems might reject you and how to move past a “computer says no” decision.

- Pinpoint the exact reasons why you were declined by bank home loan NZ lenders so you can fix the issues before applying again.

- Discover how second-tier lenders provide a flexible alternative for those who don’t meet the rigid criteria of the big mainstream banks.

- Learn the steps to perform an honest audit of your finances and credit history to build a much stronger case for your next application.

- See how professional guidance and insider knowledge can help you re-frame your story and negotiate a better outcome with the right lender.

Understanding Why the Mainstream Banks Said No

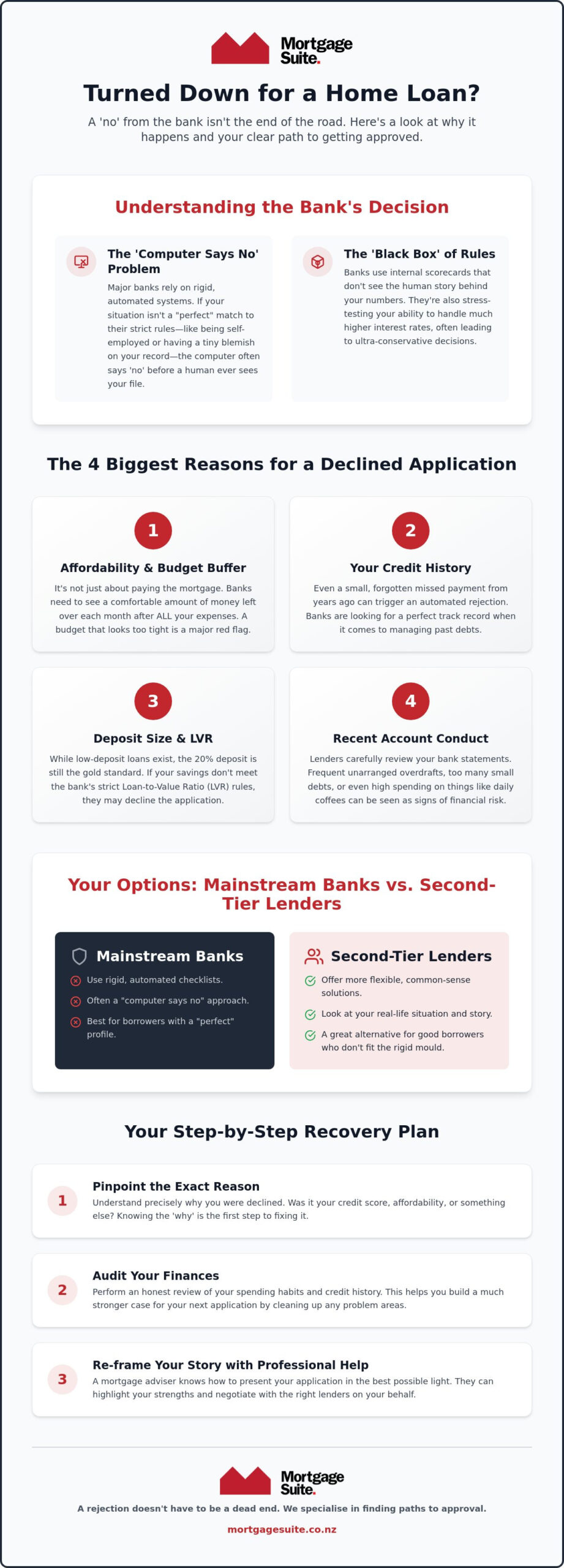

Getting that email from your bank can feel like a personal rejection of your whole financial history. It’s heart-breaking when you’ve spent years saving and sacrificing, only to find yourself declined by bank home loan NZ lenders at the final hurdle. Most of the time, this isn’t actually about you as a person. It’s about a rigid set of rules that banks use to filter out anyone who doesn’t fit a very specific, narrow mould. In 2026, those rules have become tighter than ever.

Banks today rely heavily on automated systems that make decisions in seconds. These systems are designed to find “perfect” profiles, which usually means a steady salary and zero debt. If your life is even slightly different, like being self-employed or having a small blemish on your record, the computer often triggers a “no” before a human even looks at your paperwork. When you are declined by bank home loan NZ staff, it feels like a final verdict, but it’s usually just a sign that their specific checklist doesn’t match your life.

There is also a big difference between a “Hard No” and a “Soft No.” A hard no usually comes from serious money issues in the past. A soft no is often just a mismatch with the bank’s current rules. Maybe your debt is slightly too high compared to your income, or the bank has already given out too many low-deposit loans for that month. These are hurdles, but they don’t have to be the end of the road.

The “Black Box” of Bank Rules

Banks use a “black box” approach to decide who gets a loan. They use internal scorecards that don’t account for the human story behind your bank statements. In July 2026, with the official interest rate sitting at 2.50%, banks are checking if you can handle higher payments if rates climb even further. They want to be absolutely certain you can manage if interest rates go well above the current 5% range.

Your internal scorecard is also affected by your history. If you’re wondering What is a credit score?, it’s essentially a number that tells a lender how reliable you’ve been with money in the past. Even a clean record can fail if the bank decides they have enough loans in your specific job industry or suburb. It’s not about you; it’s about their own balance sheet and their current appetite for risk.

The Impact of Strict Lending Laws

New Zealand’s lending laws have changed the game for anyone wanting a home. Even with a new regulator taking over in July 2026, the rules remain very strict. Banks are legally required to make sure you won’t struggle to pay. This is why they look at every single transaction, flagging things like your daily coffee or a gym membership. They are forced to be ultra-conservative to protect themselves.

Krish Krishna, who has spent over twenty years in the banking world, has seen this shift first-hand. Lending used to be based on your character and a handshake. Today, it’s almost entirely based on data and algorithms. The bank doesn’t see your potential; they only see the numbers on the screen. Understanding this shift is the first step to moving away from the big banks and finding a lender who will actually listen to your story.

The 4 Biggest Reasons for a Declined Home Loan Application

If you’ve been declined by bank home loan NZ lenders, it usually comes down to four specific areas where the bank feels the risk is just too high. While the bank’s decision might feel like a mystery, it almost always relates to how your current financial life fits into their strict 2026 rulebook. Understanding these reasons is the first step toward fixing them.

The first major hurdle is your affordability. This isn’t just about whether you can pay the mortgage today; it’s about whether you’ll have enough money left over after all your other expenses are paid. Banks want to see a comfortable “buffer” in your budget. Second, your past history with money plays a huge role. Even a tiny missed bill from a few years ago can be a red flag. It is well worth checking how your credit score impacts borrowing because banks often use automated systems that reject anything less than a perfect record.

The third reason involves your deposit size. While there are special programmes for first-home buyers with a 5% deposit, the standard 20% requirement is still the benchmark for most. If the property value has shifted or your savings aren’t quite enough to satisfy the bank’s “loan-to-value” rules, they may decline the application. Finally, your account conduct is under the microscope. Lenders look at your bank statements to see if you frequently go into unarranged overdraft or have too many small debts. If your statements are looking a bit messy, you might want to chat with us at Mortgage Suite Ltd to see how we can help you tidy things up.

Debt-to-Income Limits and Hidden Costs

In 2026, the debt-to-income limits set by the Reserve Bank are a primary reason for rejections. For most people buying a home to live in, banks are restricted from lending more than six times your gross yearly income. This includes all your debts, not just the new mortgage. “Hidden” costs like Buy Now Pay Later schemes or interest-free store cards can drastically reduce how much you can borrow. Even a small $50 weekly payment to one of these services can knock thousands of dollars off your total loan amount.

Property Type and Location Restrictions

Sometimes the bank says no because of the house itself rather than your money. Mainstream lenders are often wary of very small apartments, homes with potential structural risks, or properties in certain rural areas. An un-lendable property is any dwelling that doesn’t meet a bank’s security criteria. If you have your heart set on a unique home or an “as-is” sale, the big banks might not be the right fit for that specific property.

Comparing Your Options: Mainstream Banks vs. 2nd Tier Lenders

When you’ve been declined by bank home loan NZ lenders, it’s easy to feel like you’ve run out of road. But the New Zealand lending market is much broader than just the big household names you see on the high street. If the mainstream banks have said no, it’s often because your life doesn’t fit into their very specific, automated box. This is where alternative or “non-bank” lenders come into play. These are established, professional financial companies that operate with more flexibility than traditional banks.

The main trade-off here is between flexibility and cost. Mainstream banks usually offer the lowest interest rates, but they demand a perfect application. Alternative lenders might charge a slightly higher rate or a one-off fee, but they are far more willing to listen to your actual circumstances. They don’t just look at a score; they look at your potential. For a deeper look at who these providers are, check out our guide on non-bank lenders NZ.

Think of these lenders as a strategic bridge. Instead of waiting years for a small credit issue to disappear or for your business to show several years of perfect records, an alternative loan gets you into your home now. You can start building your own equity and benefit from any house price growth while you prove your reliability to the market over the next year or two.

The Human Element in Alternative Lending

The biggest benefit of these lenders is that they don’t rely on a computer to make the final call. Instead of an automated system that rejects you for one minor mistake, you benefit from having a real person review your application. They want to know the “why” behind your situation. For example, if your deposit was slightly lower than 20%, they might look at your strong career history as a way to balance that risk.

We recently helped a self-employed tradie who was in this exact position. He had plenty of work and a great income, but because he’d only been in business for 18 months, the big banks wouldn’t even open his file. By using an alternative lender, Mortgage Suite Ltd showed a human assessor his actual bank statements and current contracts. He got his approval in days, proving that being declined by bank home loan NZ lenders doesn’t have to stop you from buying a house.

Stepping Stones: The Long-Term Strategy

We usually suggest using these alternative lenders for about 12 to 24 months. During this time, you make every payment on time and build up your equity as the property value grows. Once your situation has stabilised and your records are up to date, Mortgage Suite Ltd can then help you move back to a mainstream bank at a lower interest rate. You can read more about this transition in our 2nd tier lender New Zealand guide.

Your Step-by-Step Recovery Plan After a Loan Rejection

Getting the news that you’ve been declined by bank home loan NZ lenders is a shock, but it’s not the end of the road. You need a calm, methodical plan to turn things around. Instead of letting frustration take over, follow these steps to rebuild your application and get back on track. The goal is to move from a “no” to a “yes” by addressing the specific hurdles the bank identified.

The first step is to get the specific reason for the decline in writing. Don’t just accept a vague explanation over the phone. You need to know if the issue was your income, your deposit, or perhaps a blemish on your credit report. Once you have this, conduct an honest audit of your finances. Look at your bank statements and credit file through the eyes of a lender. If you see frequent “buy now, pay later” payments or small overdraft fees, you’ve found your starting point for improvement.

It’s also vital to pause all new credit applications immediately. Every time you apply for a new limit or a store card, it leaves a footprint on your file that can look like credit stress to a bank. Instead, consult a specialist broker who understands the alternative lending market. They can help you organise a pivot strategy. This might involve staying with your current bank and fixing your spending habits, or it might mean switching to a lender that is more comfortable with your specific situation. If you’re ready to stop the guesswork, reach out to us today to get a clear plan for your next move.

Cleaning Up Your Financial Act

To win over a new lender, you need to prove you are a reliable borrower. This often requires a period of what we call clean spending. Clean spending is a three-month period of zero unarranged overdrafts or missed payments. It shows a lender that you are in total control of your money. You should also look at closing down any unused credit cards or “zombie” accounts. Even if you don’t use the balance, the bank counts that entire credit limit as a potential debt, which can significantly lower your borrowing power under the current DTI rules.

Protecting Your Credit File

Many people make the mistake of “shopping around” by applying at multiple banks directly after being declined by bank home loan NZ lenders. This is a recipe for disaster. Each application can lower your credit score further. A specialist broker acts as a firewall for your credit file. We only submit your application to the lender most likely to approve it, saving your score from unnecessary hits. For those who have more complex credit issues, our guide on non-conforming home loans New Zealand provides a detailed look at how to secure a mortgage even when your history isn’t perfect.

How Mortgage Suite Ltd Turns a ‘No’ Into a ‘Yes’

Rejection from a main bank doesn’t have to be the end of your property journey. It’s often just a sign that your application needs a different approach. When you’ve been declined by bank home loan NZ lenders, the team at Mortgage Suite Ltd steps in to bridge the gap between rigid bank rules and your personal goals. We don’t see you as a credit score; we see you as a partner who deserves a fair go in a tough 2026 market.

Our strength lies in Krish Krishna’s 20 plus years of insider banking experience. Krish understands the “black box” of bank credit policies because he’s spent decades on the other side of the desk. This deep institutional knowledge allows Mortgage Suite Ltd to “re-frame” your story. We know how to present your finances in a way that addresses a lender’s specific fears, turning a potential rejection into a confident approval. It’s about more than just filling out forms; it’s about high-level negotiation and advocacy.

One of the biggest advantages of working with Mortgage Suite Ltd is our access to the 2nd tier market. Many of the most flexible alternative lenders in New Zealand don’t deal with the public directly. They only work through trusted brokers. This means we can open doors that are otherwise locked, giving you access to home loans that main banks simply can’t offer. We fight for your approval by manually pitching your case to the right person, ensuring your human story isn’t lost in an automated system.

Specialist Solutions for Unique Situations

We realise that everyone’s financial path looks different. If you’re a business owner or a contractor, you might find our help with low doc home loans nz particularly useful. Mainstream banks often struggle with self-employed income, but we know which lenders appreciate your entrepreneurial drive.

Mortgage Suite Ltd also handles “Bad Credit” scenarios with zero judgement. Whether it’s an old default or a temporary setback, we focus on the solution rather than the mistake. Our expertise also extends to more complex needs, such as property development and commercial pivots. When a bank pulls back on a project, we have the connections to find alternative funding that keeps your development moving forward.

Ready to Get Your Property Dreams Back on Track?

Many people think they need to wait six or twelve months after being declined by bank home loan NZ lenders to try again. In reality, waiting can sometimes be the wrong move, especially if property prices are rising or your current living situation is costing you money. A strategic pivot to an alternative lender could get you into your home today, allowing you to build equity right now.

We offer a “No Worries” consultation where we’ll give you an honest assessment of your options. No jargon, no judgement, just a clear path forward. If you’re tired of the “computer says no” routine, it’s time to talk to a veteran who knows how to get a “yes.” Book a strategy session with Krish at Mortgage Suite Ltd today and let’s get you sorted.

Take the Next Step Toward Your New Home

Being declined by bank home loan NZ lenders is a significant hurdle, but it’s certainly not a dead end for your property dreams. You’ve now seen that a rejection is often just a sign that your financial profile doesn’t fit a specific bank’s automated rules for 2026. By tidying up your account conduct and considering the flexible options offered by second-tier lenders, you can bridge the gap and secure your property much sooner than you think.

Success in today’s complex market requires more than just a decent deposit; it needs a dedicated negotiator who understands how the system works from the inside. Mortgage Suite Ltd brings over two decades of banking and brokerage experience to your side. Krish Krishna specialises in alternative lending solutions that mainstream banks often overlook, acting as a steady hand to guide you through the process.

Don’t let a single “no” stop you from reaching your goals. Talk to Krish at Mortgage Suite Ltd—Let’s turn that “No” into a “Yes”. We are ready to help you find a clear path forward and get your plans back on track with confidence.

Frequently Asked Questions

Why did the bank decline my home loan if I have a 20% deposit?

Banks look at more than just the size of your deposit. Even with 20% equity, they need to be certain your income can cover the repayments if interest rates go up. They use a higher “test rate” to see if you have enough money left over after all your usual bills and debts are paid. If your monthly surplus is too low, the deposit size doesn’t matter to their automated systems.

How long should I wait to apply again after being declined by a bank in NZ?

There is no set rule, but waiting three months is often wise if you need to show better spending habits. If the decline was simply because that specific bank didn’t like your property type, you could potentially apply elsewhere straight away. The key is to fix the underlying issue first so you don’t end up with another rejection on your record.

Can a mortgage broker help if I’ve already been declined?

A mortgage broker is often the first person you should call after being declined by bank home loan NZ lenders. We can look at the bank’s feedback and determine if it was a “soft no” based on their internal policy or a “hard no” due to credit issues. From there, we can match you with a lender that values your specific financial profile and understands your story.

Is a 2nd tier lender safe for a New Zealand home loan?

Yes, these lenders are safe and highly regulated in New Zealand. They provide a vital service for people who don’t fit the narrow criteria of mainstream banks. While they might not have branches on every corner, they are professional organisations that must follow the same consumer protection laws as any other lender. They are a legitimate path to home ownership for many Kiwis.

Will being declined for a mortgage hurt my credit score?

A rejection doesn’t show up on your credit report, but the fact that you applied does. Each application creates a “hard enquiry,” and having too many of these in a short period can lower your score. It suggests to other lenders that you might be struggling financially. This is why it is much safer to let a broker handle the enquiries for you to protect your file.

What is the most common reason for a mortgage decline in 2026?

The introduction of Debt-to-Income (DTI) ratios is currently the biggest hurdle. As of July 2026, most banks won’t lend more than six times your gross annual income if you are buying a home to live in. When you combine this with high interest rates and strict spending checks, it’s becoming much harder for the average Kiwi to meet the mainstream bank’s rigid criteria.

Can I get a home loan if I am self-employed and have been declined?

You certainly can, as being declined by bank home loan NZ institutions is a common experience for business owners. Mainstream banks often want two years of perfect financial records. Alternative lenders are much more flexible. They can often use your recent bank statements or a shorter history of financial accounts to prove you can afford the loan. We specialise in finding these common-sense solutions.

How much more does a non-bank home loan cost compared to a bank?

Non-bank lenders generally have slightly higher interest rates and may charge an establishment fee. This reflects the fact that they are taking on more risk or doing more manual work to assess your application. Most of our clients see this as a temporary cost; it’s a way to get into a home now and build equity before eventually moving back to a bank later.