How to Qualify for a Home Loan in NZ: The 2026 Comprehensive Checklist

What if a "no" from a mainstream bank wasn’t a closed door, but a sign that you simply needed a more tailored approach to your finances? Many Kiwis feel a sense of dread when looking at their bank balance, especially with the 2024 debt-to-income (DTI) restrictions still making things difficult for first home buyers and investors alike. You’re likely searching for exactly how to qualify for a home loan NZ lenders will approve in 2026. With the Official Cash Rate at 2.25 percent and standard one-year rates sitting near 4.89 percent, the financial landscape requires a steady hand and a clear strategy.

It’s completely natural to feel anxious about your credit score or confused by the difference between a 5 percent and 20 percent deposit requirement. We believe that every borrower deserves a transparent path to home ownership. This comprehensive checklist will help you master the financial requirements and documentation needed to secure your New Zealand home loan with confidence. We’ll examine everything from modern servicing requirements to the 2nd tier lending options that provide a vital lifeline when mainstream banks hesitate.

Key Takeaways

- Learn how the 2026 lending benchmarks, including the 2.25 per cent OCR and DTI restrictions, define your current borrowing power.

- Discover how to qualify for a home loan NZ lenders will approve by mastering the “uncommitted monthly income” test and optimising your debt-to-income ratio.

- Understand why a rejection from a mainstream bank isn’t the end of the road and how 2nd tier lenders offer flexible paths for non-conforming borrowers.

- Secure a seamless application process by using our master checklist to gather “Golden Documents” and proactively fix credit report errors.

- Gain the confidence of having a seasoned advocate to negotiate complex bank policies and ensure your financial readiness is presented in the best possible light.

Table of Contents

-

The Fundamental Pillars of Home Loan Qualification in New Zealand

-

Mainstream Banks vs. 2nd Tier Lenders: Finding Your Best Path

The Fundamental Pillars of Home Loan Qualification in New Zealand

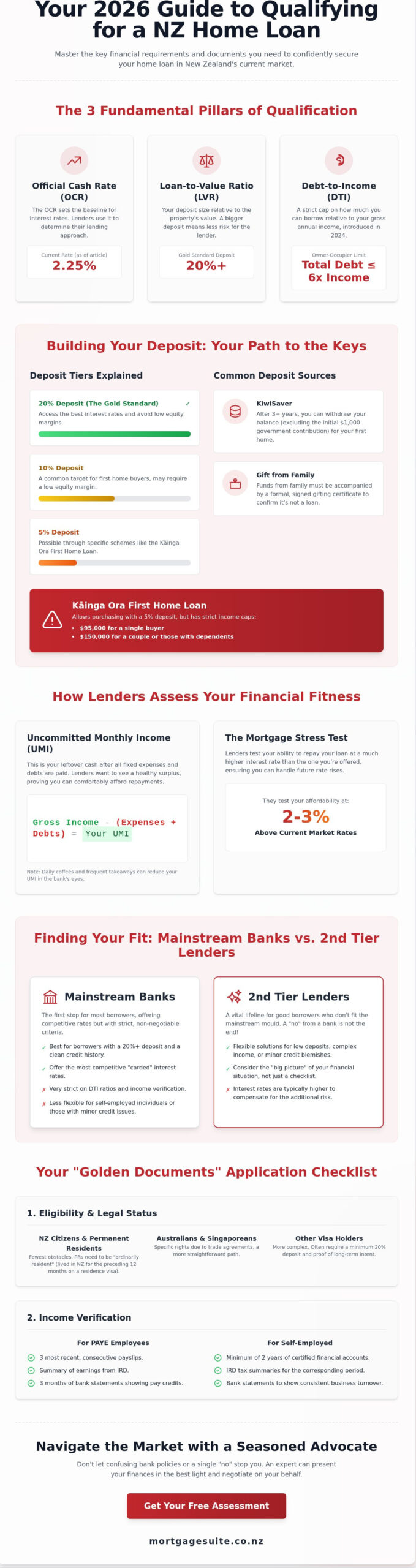

Home Loan Qualification is the process of proving both financial stability and collateral security to a lender. In the 2026 market, this proof is measured against three specific benchmarks: the Official Cash Rate (OCR), Loan-to-Value Ratios (LVR), and Debt-to-Income (DTI) caps. With the OCR currently at 2.25 percent, banks have maintained a cautious approach to lending, making it essential to understand how to qualify for a home loan NZ lenders will actually approve. Understanding New_Zealand’s property market dynamics helps explain why these hurdles exist; they act as a safeguard for both the borrower and the financial system against future economic volatility.

The deposit you bring to the table remains the primary factor in determining your interest rate and lender options. While a 20 percent deposit is the gold standard for avoiding low equity margins and securing the best carded rates, many first-time buyers aim for the 10 percent or 5 percent thresholds. If you’re looking at a 5 percent deposit through the Kāinga Ora First Home Loan, you’ll need to stay within the income caps of $95,000 for a single buyer or $150,000 for couples or those with dependents. If your income exceeds these limits but your deposit is small, you aren’t necessarily out of options, but you’ll likely need to explore low deposit home loan NZ solutions through 2nd tier lenders who offer more flexibility.

Residency and Legal Status Requirements

Before you start visiting open homes, you must confirm your legal eligibility to purchase property. New Zealand citizens and permanent residents face the fewest obstacles. To be considered "ordinarily resident", you typically need to have lived in New Zealand for the preceding 12 months and held a valid residence class visa during that entire period. Australians and Singaporeans enjoy specific rights due to trade agreements, but most other visa holders will find the path more complex. If you’re on a work visa, banks often require a minimum 20 percent deposit and proof of your long-term intent to remain in the country.

The Deposit: KiwiSaver, Grants, and Savings

Your KiwiSaver account is likely to be your most significant tool for building a deposit. In 2026, you can withdraw your total balance, excluding the initial $1,000 government contribution, as long as you’ve been a member for at least three years. Don’t forget that the First Home Grant was discontinued on 22 May 2024, so it’s no longer a source of funding for new applicants. If you’re receiving financial help from family, lenders will require a formal gifting certificate. This document confirms the funds are a non-repayable gift, ensuring the bank doesn’t view the contribution as an undisclosed debt that would negatively impact your DTI ratio. Understanding the full picture of home loan deposit requirements NZ lenders apply in 2026 can help you plan your savings strategy with far greater precision.

Assessing Your Financial Fitness: Income, Expenses, and DTI

Securing a deposit is only half the battle. In 2026, understanding how to qualify for a home loan NZ lenders will sign off on requires a deep dive into your Debt-to-Income (DTI) ratio. Since the regulations introduced in mid-2024, banks are strictly limited in how much high-DTI lending they can provide. For most owner-occupiers, this means your total debt, including your new mortgage, should not exceed six times your gross annual income. If you’re looking at First Home Loan eligibility criteria, you’ll see that income caps and DTI limits work together to define your maximum borrowing ceiling.

Beyond the raw numbers of your salary, credit officers now scrutinise your "uncommitted monthly income". This is what remains after all your essential costs, existing debts, and a buffer for life’s surprises are deducted. It’s why your daily latte habit or frequent Uber Eats orders actually matter; they represent discretionary spending that could, in the bank’s eyes, be redirected toward mortgage repayments. Lenders stress-test your ability to pay at interest rates 2-3% higher than current market rates. This ensures that even if the OCR climbs further, your household budget won’t collapse under the weight of rising repayments.

Income Verification for Different Employment Types

The way you earn your living dictates the paperwork you’ll need to provide. PAYE employees usually have the simplest path, requiring three months of consecutive payslips and a summary of earnings from the IRD. If you’re self-employed, the requirements are more stringent. You’ll need at least two years of certified accounts and IRD tax summaries to prove your business is stable and profitable. Contractors and those in the gig economy often face more scrutiny due to irregular income. Lenders will look for a consistent history of contracts and a healthy "buffer" in your savings to offset periods between jobs. If your income structure is complex, speaking with a specialist can help you present your earnings in the most favourable light.

The Expense Audit: Cleaning Up Your Transaction History

Banks will typically request three to six months of transaction history to look for "red flag" behaviours. Frequent gambling transactions, heavy reliance on Buy Now Pay Later (BNPL) services, or a long list of unused subscriptions can signal poor financial discipline. We recommend "grooming" your accounts at least 90 days before you apply. This means clearing small debts and ensuring your bank statements reflect a disciplined, organised lifestyle. Existing liabilities like car loans or high credit card limits also reduce your borrowing power. Even if you don’t use your full credit limit, the bank calculates your DTI based on the total limit available to you, not just the balance you owe.

Mainstream Banks vs. 2nd Tier Lenders: Finding Your Best Path

Receiving a rejection letter from a major bank can be disheartening, but it certainly isn’t the end of your home ownership journey. The New Zealand financial market is more diverse than many realise. While mainstream banks have rigid, automated systems, 2nd tier lenders often take a more holistic, manual approach to assessing risk. If you are struggling with how to qualify for a home loan NZ banks have declined, these alternative lenders provide a vital pathway. They are often willing to look at the story behind the numbers, providing solutions for those who don’t fit the traditional "cookie-cutter" borrower profile.

The trade-off for this increased flexibility is typically a slightly higher interest rate and potentially different fee structures. However, this cost should be viewed as a strategic investment. At Mortgage Suite Ltd, we specialise in acting as the bridge between you and these alternative capital sources. We understand which lenders have an appetite for specific scenarios, ensuring you don’t waste time on applications destined for another decline. Our role is to negotiate the best possible terms, ensuring your path to property is as smooth and cost-effective as possible.

When to Consider a Non-Bank Lender

Non-bank lenders are an excellent option if your credit history has a few old marks, such as a past default that has since been resolved. They are also far more pragmatic when it comes to non-standard property types, including tiny homes, small inner-city apartments, or leasehold titles that mainstream banks often avoid. Additionally, self-employed individuals who have been trading for less than two years often find a much warmer reception here. These lenders focus on your current ability to service the debt rather than just your historical tax returns.

The Path Back to Mainstream Banking

We often recommend using 2nd tier lending as a short-term stepping stone, typically for a period of one to three years. During this time, your main goal is to build equity and maintain a flawless repayment history. This period allows you to "season" your financial profile and move past any previous credit issues. Once you have reached a stronger equity position or have established a consistent track record, we can then help you refinance back to a mainstream lender. This transition allows you to benefit from lower interest rates while having already secured the property you want.

Your Step-by-Step Home Loan Qualification Checklist

Securing a pre-approval is your most powerful tool when entering the 2026 property market. It transforms you from a casual browser into a serious buyer, giving you the confidence to bid at auction or make unconditional offers. Understanding how to qualify for a home loan NZ lenders will prioritise involves more than just a healthy savings account; it requires a disciplined approach to paperwork. Before you approach any lender, we strongly advise checking your credit report. You can access your report for free from major providers like Centrix or Equifax. Reviewing this early allows you to fix any administrative errors or old disputes before a credit officer sees them.

Organise your documents in a digital folder for instant access during negotiations.

This proactive step ensures that when a property catches your eye, you aren’t scrambling for old payslips while another buyer swoops in. Having your files ready also demonstrates to the bank that you are a reliable, low-risk borrower who manages their affairs with professional precision. It reflects a level of financial readiness that can often sway a lender’s decision in your favour.

The Documentation Master List

-

Identification: A current passport or New Zealand driver’s licence, along with a recent utility bill or bank statement as proof of address.

-

Financials: Three to six months of consecutive bank statements for every account you hold, including credit cards and savings.

-

Proof of Deposit: Latest KiwiSaver statements, a formal gift letter if family is assisting, or receipts for term deposits.

-

Employment Proof: Your three most recent payslips or a signed employment contract if you have recently started a new role.

The Final "Ready to Buy" Sanity Check

Before you sign a Sale and Purchase Agreement, perform a final audit of your timeline. If you are using KiwiSaver for your deposit, initiate the withdrawal process early, as it typically takes 10 to 15 working days for funds to clear. While the First Home Grant was discontinued on 22 May 2024, you should verify that any other scheme approvals, such as the First Home Loan, remain current and valid for your intended purchase. Finally, ensure you have maintained a strict "spending freeze" for at least 90 days. This means no new debt, no large luxury purchases, and no changes to your credit limits. If you’re ready to take the next step, you can apply for a home loan with our team to get your pre-approval underway.

Navigating the 2026 Market with a Seasoned Advocate

The 2026 lending environment is a complex machine with many moving parts. Between the 2.25 percent OCR and the rigid DTI caps, simply walking into your local branch often leads to a dead end. Going direct to a single bank limits your options to their specific, often inflexible, criteria. We believe that understanding how to qualify for a home loan NZ lenders will back requires a more sophisticated approach. At Mortgage Suite Ltd, we leverage over 20 years of deep institutional banking experience to act as your dedicated advocate. We don’t just process applications; we negotiate on your behalf to find a solution that fits your unique financial reality.

Our consultative method ensures that your home loan is a foundation for long-term wealth, not just a monthly expense. We look beyond the immediate approval to see how your debt structure will perform over the next decade. Whether you are seeking a standard residential loan or require the flexibility of 2nd tier capital, our team is committed to the removal of obstacles. This seasoned perspective is particularly valuable for those who have been told "no" elsewhere. We know exactly how to present your case to the right people to get to "yes".

Why Expertise Matters in a Volatile Market

A home loan is more than just an interest rate. The fine print often contains the most significant risks and opportunities. We help you understand the long-term impact of interest-only periods, the benefits of offset accounts, and the potential sting of break fees if you need to refinance. If your situation is non-conforming, our access to 2nd tier loans ensures you aren’t left behind by the mainstream banking system. For those just starting out, our Home Loans for First Home Buyers in New Zealand: The 2026 Comprehensive Guide provides an even deeper look at the specific grants and schemes available this year.

Your Partnership for Success

Our relationship with you doesn’t end when you get the keys. We view ourselves as your long-term partners in success. As your equity grows, we can help you plan the transition from first-home buyer to property investor. We provide ongoing support, reviewing your rates and structure as the OCR shifts or your life circumstances change. This proactive management ensures you are always in the best possible position to build equity. Booking a no-obligation strategy session is the first step toward financial readiness. Contact Mortgage Suite Ltd to start your qualification journey today and take control of your property future with a steady hand by your side.

Take the Next Step Toward Your New Zealand Home

Mastering the details of your debt-to-income ratio and maintaining a disciplined expense audit are the true keys to success in today’s market. While the 2026 lending environment remains complex, you don’t have to face it alone. We’ve explored the necessity of digital document readiness and the strategic advantage of looking toward 2nd tier lenders when mainstream banks say no. Understanding how to qualify for a home loan NZ lenders will approve is about more than just numbers; it’s about presenting a story of financial reliability.

With over 20 years of banking and lending expertise, our team acts as dedicated negotiators for both first-home buyers and seasoned investors. We are specialists in 2nd tier and non-bank solutions, ensuring that every client has a viable path forward regardless of their initial bank feedback. Secure your financial future with a tailored home loan strategy from Mortgage Suite. Your property goals are within reach, and with the right advocate, you can navigate this market with absolute confidence.

Frequently Asked Questions

How much deposit do I really need for a home loan in NZ in 2026?

You generally need a 20 per cent deposit to access the best interest rates and avoid low equity margins in the current market. However, eligible first-home buyers can still secure a low deposit home loan NZ with as little as a 5 per cent deposit through the Kāinga Ora First Home Loan scheme. For those who don’t meet those specific income caps, a 10 per cent deposit is often the minimum required by mainstream banks, though lending at this level remains restricted.

Can I qualify for a home loan if I am self-employed with only one year of accounts?

Most mainstream banks require at least two years of certified accounts to prove income stability and business longevity. If you have only been trading for one year, banks can still consider your application if you can provide with a 12 months Profit & Loss projection and Cash Flow forecast. If your forecasts are consistent with your historical trading and or larger projections can be mitigated, then you are in the game. Failing, this then there are 2nd Tier Lenders that can assist you. These lenders take a more manual approach to your application, focusing on your current business performance and future potential rather than just a long historical track record.

What is the maximum Debt-to-Income (DTI) ratio NZ banks allow?

For owner-occupiers, the standard maximum DTI ratio is six, meaning your total debt cannot exceed six times your gross annual income. For property investors, the limit is slightly higher at seven. Banks are required to limit high-DTI lending to 20 per cent of their new loans, so staying below these thresholds is a critical part of how to qualify for a home loan NZ lenders will readily approve.

How does my credit score affect my ability to qualify for a mortgage?

Your credit score acts as a financial reputation check that lenders use to gauge your reliability and risk profile. A high score suggests disciplined financial habits, which can help you secure lower interest rates and faster approvals. If your score is lower due to past defaults, it won’t necessarily stop your journey, but it may mean you need to work with alternative lenders who are more comfortable with credit-impaired applications.

Can I use my KiwiSaver for a deposit if I have owned a home before?

Yes, you may be able to withdraw your KiwiSaver funds as a "second-chance" buyer if your financial position is deemed similar to that of a first-home buyer. You will need to apply to Kāinga Ora for a determination of your status before your provider can release the funds. This is a vital lifeline for those looking to re-enter the property market after a significant life change or a financial setback.

What happens if my home loan application is declined by a mainstream bank?

A decline from a mainstream bank is often just the start of a more tailored conversation about your options. We first review the specific reasons for the decline, such as a high DTI ratio or recent discretionary spending habits. From there, we can look toward 2nd tier lenders who offer more flexible criteria. This allows you to secure your property now while working on a plan to refinance back to a bank later.

How long does the home loan pre-approval process take in NZ?

You should typically allow between two and five working days for a standard pre-approval, though complex applications can take longer. Having your "Golden Documents" organised in a digital folder beforehand is the best way to speed up this process. Once issued, a pre-approval is usually valid for 90 days, giving you the breathing room to attend auctions and negotiate with sellers with total confidence.

Do banks count student loans as debt when qualifying for a mortgage?

Banks definitely include student loans in their assessment because the mandatory repayments reduce your "uncommitted monthly income". While the loan itself is interest-free, the deductions from your salary lower your ability to service a mortgage. When we calculate how to qualify for a home loan NZ, we factor these repayments into your DTI ratio to ensure your borrowing level remains sustainable and within current regulatory limits.