Home Loan Deposit Requirements NZ: Your 2026 Guide to Getting on the Property Ladder

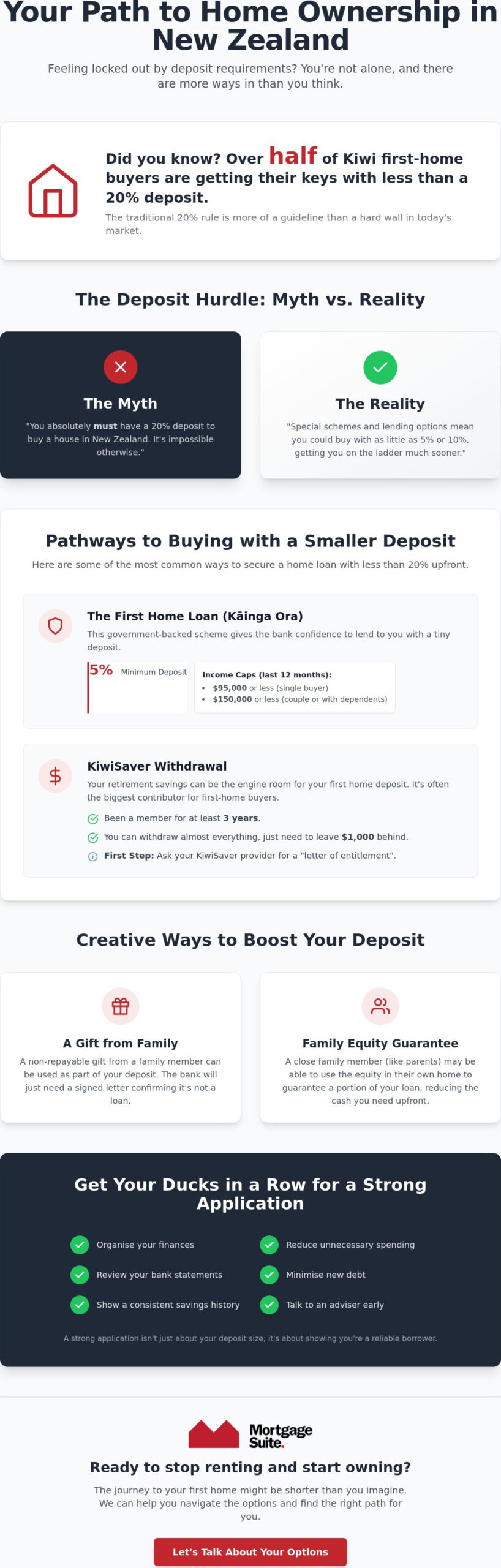

Did you know that over half of Kiwi first-home buyers are currently getting their keys with less than a 20% deposit? It’s a statistic that might surprise you, especially if you’ve spent months feeling like the goalposts for home loan deposit requirements NZ are constantly moving. While the traditional 20% benchmark is often presented as a brick wall, the reality of the 2026 property market is far more flexible for those who have a steady hand to guide them through the various options available.

We know it’s exhausting to hear conflicting advice about 5%, 10%, and 20% deposits while worrying that a mainstream bank might simply say no. It’s a stressful spot to be in, but you don’t have to navigate this journey alone. This guide will show you exactly how much you need to save and reveal the clever ways to buy your first home even with a smaller savings pot. We’ll break down the current Kāinga Ora 5% rules, explain why new builds are a game-changer for low deposits, and give you the practical knowledge and confidence to finally stop renting and start owning.

Key Takeaways

- Understand why the traditional 20% deposit isn’t always a requirement and how you can join the thousands of Kiwis buying with a much smaller upfront payment.

- Learn how to navigate the current home loan deposit requirements NZ, including government-backed schemes that allow for a deposit as low as 5%.

- Discover creative ways to boost your deposit, from utilising family equity guarantees to receiving gifts that help you reach your goal faster.

- Find out how to look beyond mainstream banks and explore alternative lending options if your financial situation doesn’t fit their rigid criteria.

- Pick up expert tips on organising your finances and bank statements to ensure your 2026 application is as strong as possible before you approach a lender.

The lowdown on home loan deposit requirements NZ in 2026

When you start looking at houses, the first big hurdle is always the deposit. Simply put, a home loan deposit is the chunk of cash you pay upfront when you buy a property. Your house deposit is simply the difference between the total purchase price of your new home and the amount you need to borrow through a mortgage. It represents your “skin in the game,” and it’s the primary way banks measure how much risk they’re taking on when they lend you money.

In New Zealand, you’ll often hear about the “20% rule.” This isn’t just a random number the banks made up to be difficult; it’s largely driven by the Reserve Bank of New Zealand. They set these rules to keep the entire housing market stable and ensure that both lenders and borrowers don’t end up in over their heads. While the home loan deposit requirements NZ can feel like a massive barrier, understanding why these rules exist is the first step toward navigating them successfully. The government has tried various ways to help people enter the market, such as the KiwiBuild programme, which aimed to increase the supply of affordable homes for those struggling to save a massive deposit.

Why do banks prefer a 20% deposit?

Banks love a 20% deposit because it acts as a safety net. If property values take a temporary dip, that 20% buffer ensures the bank can still recover the loan amount if the house needs to be sold. From your perspective, having that 20% often unlocks the “special” lower interest rates that you see advertised on billboards. If you have a smaller deposit, banks often charge extra costs, sometimes called low equity margins, which can make your monthly repayments more expensive. Aiming for that 20% mark is the most straightforward way to keep your long term costs down.

The difference between a deposit and equity

It’s easy to get these two terms mixed up, but they’re actually quite different. A deposit is the actual cash you have sitting in your bank account right now, ready to be handed over. Equity, on the other hand, is the value of the property you actually own after you subtract what you owe the bank. For example, if your house is worth $800,000 and your mortgage is $600,000, you have $200,000 in equity.

First-home buyers almost always start with a cash deposit, often built up through years of disciplined saving or KiwiSaver contributions. Investors, however, often use the equity in their existing homes to buy more property. Understanding this distinction is vital because it changes how you approach home loan deposit requirements NZ depending on where you are in your property journey. Whether you’re starting with a pile of cash or looking to leverage what you already own, the goal is the same: showing the bank you have a solid foundation.

How to buy a house with a 5% or 10% deposit

If you’ve been staring at house prices and feeling like you’ll be renting forever, I have some good news. The 20% rule we discussed earlier isn’t a legal requirement for everyone. In fact, there are several pathways that allow you to bypass the standard home loan deposit requirements NZ and get into your own place much sooner than you might have expected. While the big banks prefer a larger buffer, they are permitted to lend a certain percentage of their money to people with smaller deposits, provided those borrowers are in a strong financial position.

Using KiwiSaver to boost your deposit

For most Kiwis, KiwiSaver is the engine room of their house deposit. If you have been a member for at least three years, you can generally withdraw almost all of your savings to put toward your first home. You just need to leave a minimum of $1,000 in your account. The very first thing you should do is contact your provider and ask for a “letter of entitlement.” This document is vital because it proves to the bank exactly how much cash you can contribute. It’s often the single biggest contributor for first-home buyers, turning a modest savings account into a serious deposit overnight.

Government help: The First Home Loan

This is a significant leg-up for those struggling to reach the 10% or 20% mark. The First Home Loan scheme is underwritten by Kāinga Ora, which essentially means the government gives the bank the confidence to accept a tiny 5% deposit. To qualify in 2026, you must meet certain income criteria. Specifically, you need to have earned $95,000 or less in the last 12 months as a single buyer, or $150,000 or less if you are buying as a couple or have dependents. While the government has removed the previous house price caps, you still need to prove to the lender that your income is high enough to comfortably service the mortgage repayments every fortnight.

Beyond government schemes, new builds or “turnkey” properties are another excellent option. These homes are often exempt from the usual lending restrictions, meaning banks are frequently more willing to offer 10% deposit options on brand-new houses. This can be a much easier path than trying to buy an existing home where the 20% rule is more strictly applied. If you want to explore these pathways in more detail, our low deposit home loan NZ guide provides a deeper look at the mechanics of these applications. If you’re feeling overwhelmed by the choices, chatting with a specialist mortgage adviser can help you identify which low-deposit route is the most realistic for your current income and savings.

Creative ways to top up your house deposit

Saving for a house in 2026 doesn’t have to be a solo mission. Many Kiwis find that the quickest way to meet home loan deposit requirements NZ is by combining their resources with others. Whether that’s a partner, a sibling, or a close friend, sharing the deposit burden can cut your saving time in half and get you into the market much sooner. If you are considering this path, our ultimate first home buyer guide New Zealand offers practical strategy tips on how to structure these types of joint purchases safely.

The “Bank of Mum and Dad”: Gifting and Guarantees

The “Bank of Mum and Dad” remains a powerhouse in the local property market. If your family is in a position to help, a gifted deposit can bridge the gap to that 20% mark. However, there is a specific process to follow. Banks require a “gifted deposit letter” signed by your family members, which confirms the money is a true gift and not a loan that needs to be repaid. This ensures your debt-to-income ratio stays healthy and the bank feels confident in your ability to manage the mortgage.

If your parents don’t have spare cash but do have equity in their own home, a family guarantee might be the answer. This allows them to use a portion of their property’s value as security for your loan. It’s a clever way to meet the home loan deposit requirements NZ without anyone actually handing over a cent upfront. While the First Home Loan scheme is a government-backed option for low deposits, a family guarantee is a private arrangement that can often achieve a similar result for those who don’t meet the government’s income caps.

Using equity if you already own property

If you already own a home and want to grow your portfolio, you might not need any cash at all. By re-mortgaging your current property, you can “unlock” the value you’ve built up over the years and use it as a deposit for your next purchase. This is a common strategy for those looking at residential investment property loans NZ, where the deposit requirements are usually higher, often around 30% or 35%.

Using equity is a sophisticated way to expand your holdings without draining your savings account. It allows you to leverage the growth in the market to fund your next move. Just remember that you’ll need to prove to the bank that your income can support the increased debt across both properties. This approach turns your existing home into a financial tool that helps you climb the property ladder faster than saving cash ever could.

What to do if the big banks say “no”

Getting a “no” from a big bank can feel like a punch in the gut, but it’s rarely the end of the road. These major lenders have very specific, rigid “boxes” that you have to fit into. If your life doesn’t look exactly like their standard template, they might decline you even if you’re actually quite good with money. It’s helpful to remember that a rejection is often just a “not right now” from that particular bank, rather than a final verdict on your home ownership dreams.

While the big four banks have strict rules, there is a whole world of alternative lending that offers much more flexibility. These lenders take a different approach to home loan deposit requirements NZ, looking at your overall financial situation rather than just ticking off automated boxes. If your deposit isn’t quite the standard shape or your income is a bit unique, a 2nd tier lender New Zealand might be the solution you’ve been looking for.

Why non-bank lenders are a smart alternative

These lenders are often a lifesaver for people who are self-employed or those who have had a few credit hiccups in the past. They usually have more wiggle room with deposit sizes than the big banks do. You can think of these loans as a temporary bridge. They get you into your home today so you can start building equity. Once you’ve shown you can handle the mortgage for a year or two, you can often move your loan back to a mainstream bank to get different interest rates.

Navigating the 2nd tier landscape

There’s an old myth that non-bank lenders are a “last resort” or a bit dodgy, but that’s simply not true. They are reputable, regulated businesses that just have a different appetite for risk and a more human way they review your application. Because this part of the market is so varied, having an expert in your corner is a must. We can help you find a lender that fits your specific needs and help you plan your eventual move back to a big bank. If the mainstream lenders have turned you away, reach out to our team at Mortgage Suite Ltd to see what other doors we can open for you.

Getting your ducks in a row for a 2026 application

You’ve explored the rules and the creative workarounds. Now comes the most important part: making yourself look like the perfect borrower on paper. Even if you meet the basic home loan deposit requirements NZ, a messy bank statement or a forgotten credit card debt can stall your progress. It’s about presenting a clear, stable financial picture that gives lenders the confidence to say yes. It’s not just about the money you have; it’s about the habits you show.

Before you even think about visiting an open home, you need to get a pre-approval. This is essentially a “green light” from a lender that tells you exactly how much you can borrow. It saves you from the heartbreak of falling in love with a house that’s out of your price range. For a step-by-step guide on this process, check out our how to qualify for a home loan NZ checklist. Having this sorted early means you can act quickly when you find the right place.

The 3-month “financial diet”

Banks in 2026 are incredibly thorough. They don’t just look at your salary; they look at what we call your financial character. This means they’ll scan your bank statements for the last three to six months to see exactly where your money goes. Frequent takeaway orders, multiple streaming subscriptions, or regular high-end retail spending might seem small, but they suggest a lack of discipline to a lender. We recommend a three-month “financial diet” before you apply. This involves cutting back on unnecessary spending and ensuring you stay well within your credit limits.

Most importantly, you need to show “genuine savings.” This is money you’ve actually saved over time through your own hard work, rather than a lump sum gift or a windfall. Lenders value this because it proves you have the discipline required to manage a mortgage long-term. By tidying up your accounts now, you make it much easier for a bank to approve your application later.

Why a mortgage broker is your best advocate

Working through the maze of home loan deposit requirements NZ is much easier when you have a veteran in your corner. A mortgage adviser isn’t just someone who fills out forms. We are your advocates and negotiators. We know which lenders are currently looking for new customers and which ones have tightened their belts. At Mortgage Suite Ltd, we have over 20 years of experience in the mortgage world, making the “impossible” happen for our clients. We handle the heavy lifting, from the initial paperwork to the final negotiation with the bank. Our goal is to take the stress off your shoulders and find a path forward, even if your situation doesn’t fit the standard mould.

Your path to home ownership starts here

Getting on the property ladder might feel like a mountain to climb, but the path is often clearer than it first appears. We’ve explored how the traditional 20% rule isn’t your only option. Between government-backed schemes for 5% deposits and the flexibility offered by new builds, your current savings might already be enough to get you started. Success in the current market comes down to two things: cleaning up your financial habits to meet home loan deposit requirements NZ and having the right advocate to navigate the lending system for you.

Our team at Mortgage Suite Ltd brings over 20 years of deep banking and brokerage experience to your side. As a trusted NZ family business, we are specialists in 2nd tier and complex loans, helping Kiwis who don’t fit the rigid boxes of mainstream banks. We pride ourselves on providing a personalised service that focuses on your long term success rather than just a transaction. Ready to see if you qualify? Chat with Krish and the team at Mortgage Suite Ltd today.

You don’t have to figure out these complex financial decisions alone. With a bit of disciplined planning and a steady hand to guide you, that first set of house keys is well within your reach.

Frequently Asked Questions

Can I buy a house in NZ with a 5% deposit in 2026?

Yes, you can buy with a 5% deposit through the First Home Loan scheme if you meet the income caps we discussed earlier. This is currently one of the most effective ways to manage the home loan deposit requirements NZ when you’re starting with a smaller savings pot. You just need to show the bank that you have a steady income and can comfortably handle the mortgage repayments.

Does my KiwiSaver count as a house deposit?

It certainly does, and for many people, it’s the biggest part of their upfront payment. If you’ve been a member for at least three years, you can withdraw your savings and employer contributions, though you must leave at least $1,000 in your account. Just remember to get a letter from your provider early on so you know exactly how much you have to work with.

What is the First Home Grant and is it still available?

The First Home Grant was a government payment that ended on May 22, 2024, so it’s no longer available for new applicants. While that specific cash help has gone, the First Home Loan scheme still exists to help people get into a home with just a 5% deposit. For a full breakdown of what changed and what government support remains available today, our guide on First Home Grant NZ eligibility explains the current landscape clearly. It’s one of the remaining ways to work around the standard home loan deposit requirements NZ.

Do I need a 20% deposit for a brand-new house?

No, you generally only need a 10% deposit for a brand-new house or a property that’s being built. New builds are usually exempt from the standard deposit rules that the Reserve Bank sets for older houses. This makes them a fantastic option if you’re finding it difficult to save the full 20% buffer that big banks usually ask for.

Can my parents give me money for a house deposit?

Yes, your parents can provide a gifted deposit as long as they sign a letter confirming it doesn’t need to be paid back. This ensures the bank doesn’t view the gift as another debt you have to manage. They could also use a family guarantee, which uses the value in their own home as security so you don’t need as much cash upfront.

What happens if I have a 10% deposit but the bank says no?

If a big bank turns you down, it doesn’t mean you’re stuck. Alternative lenders often have more flexible rules for people who have a 10% deposit but don’t fit the standard bank criteria. At Mortgage Suite Ltd, we can help you find a lender that looks at your whole financial picture and values your income and stability over a rigid set of rules.

How long does it take to get a home loan pre-approval?

Most pre-approvals take between two and five working days, depending on how busy the banks are and how complex your finances look. Having your bank statements and proof of income organised before you apply will help speed things up. Once you have that “green light,” you can go house hunting with the confidence of knowing exactly what your budget is.