Property Development Loans NZ: Your 2026 Guide to Funding Your Next Project

What if the success of your next build depended less on your bank balance and more on the way you pitch your story to a lender? If you’ve been trying to secure property development loans NZ wide lately, you’ve likely noticed that the big banks aren’t making things easy. With bank stress tests still sitting around 8.5% and pre-sale requirements feeling more like a mountain than a hurdle, it’s easy to feel like your project is stuck in the mud before the first shovel even hits the ground.

We know how draining it is to have a viable site ready to go, only to be held back by rigid lending criteria that doesn’t account for your track record. You deserve a financial partner who sees the potential in your plans rather than just a list of risks. This guide is here to give you a clear path forward, showing you how to secure the right development finance by looking at both mainstream banks and more flexible second-tier options that actually want to help you build.

We will walk through the specific documents you need to prepare to impress any lender and explain the key differences between bank and non-bank funding. By the end, you’ll know exactly how to navigate the 2026 market and which doors to knock on to get your project moving.

Key Takeaways

- Understand how property development loans NZ work through staged payments to keep your build costs under control.

- Compare the lower rates of big banks with the flexibility of second-tier lenders to see which one fits your project best.

- Find out what lenders are really looking for, from your own track record to having a solid equity position.

- Get a clear roadmap for organising your feasibility study so you can prove your project is a winner.

- Discover how having a seasoned expert on your side can help translate your project into a plan that lenders love.

What Exactly Are Property Development Loans and How Do They Work?

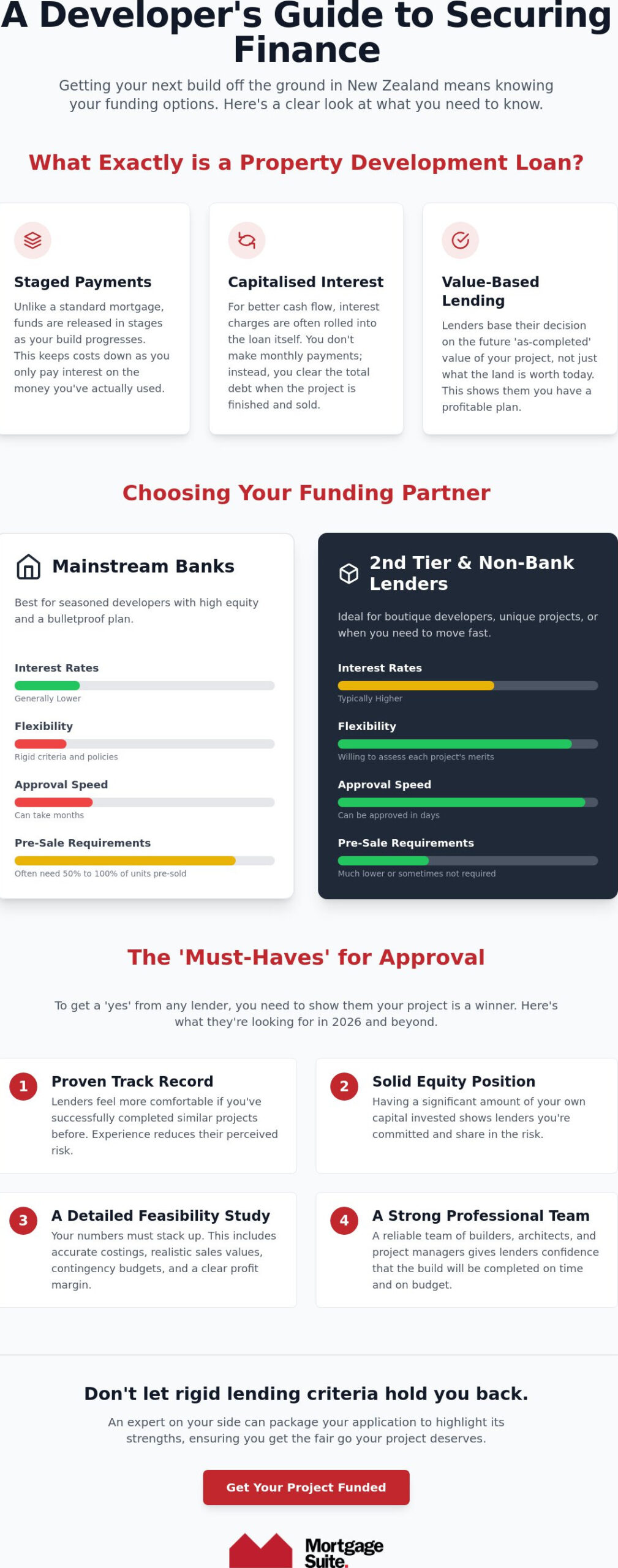

Think of a property development loan as a specialised toolkit designed for one specific job: getting your project from a set of blueprints to a finished set of keys. These are specialised funds used for building new dwellings or tackling major renovations that go far beyond a simple kitchen refresh. Essentially, a property development loan is a short-term, interest-only facility designed specifically for the construction phase of a project. Whether you’re a first-timer building a duplex in your backyard or a seasoned pro doing a small townhouse block, these tools are built to handle the unique rhythm of a construction site.

Unlike a standard home loan where you get the money upfront to buy an existing house, these loans are usually drawn down in stages, often called progress payments. This means you only pay interest on the money you’ve actually used at each point of the build, which helps keep your costs down while the foundations are being poured. To make this work, the lender doesn’t just look at what your patch of dirt is worth today. They base their lending on the “as-completed” value, which is what the finished project will likely sell for in the current market. Understanding the wider real estate development process is vital here, as it helps you see why lenders are so focused on your exit strategy and the final valuation before they’ll ever release a cent.

The Difference Between a Mortgage and Development Finance

A standard mortgage is all about you: your salary, your spending habits, and your ability to make monthly payments. Property development loans NZ lenders offer are different because they focus almost entirely on project feasibility. They want to know if the numbers actually stack up and if the project makes sense in the current climate. One of the best parts for your cash flow is a feature called capitalised interest. In plain English, this means the bank lets the interest bill grow alongside the building, and you clear the debt in one go at the finish line. You don’t have to worry about finding the cash for monthly interest payments while you’re still waiting for the roof to go on.

Why a “Fair Go” from a Bank Can Be Hard to Get

Banks are naturally cautious. They see a new build as a bundle of risks, from rising material costs to potential labour shortages. In 2026, with the Official Cash Rate at 2.25% and inflation sitting around 3.10%, banks have tightened their belts significantly. Even if your project is solid, you might find them asking for a high number of pre-sales or testing your ability to pay at rates as high as 9%. This is where having a professional broker becomes your secret weapon. We know how to package your application so it speaks the bank’s language, highlighting the strengths they might otherwise miss. We ensure you aren’t just another number in a spreadsheet but a developer with a plan that deserves a fair go.

Mainstream Banks vs. 2nd Tier Lenders: Choosing Your Funding Partner

Deciding who will fund your project is one of the biggest calls you’ll make. In the world of property development loans NZ, you’ve essentially got two paths: the big mainstream banks or the flexible non-bank lenders. While the big banks often have the flashiest offices and the lowest interest rates, they also come with the longest lists of demands. If you’re a boutique developer working on a smaller project, you might find that the “big four” aren’t actually the best fit for your needs. Most bank products are built for massive multi-million dollar schemes, leaving the smaller, high-quality projects feeling a bit left out in the cold.

The speed of approval is often the dealbreaker. Banks can take months to process a complex application, often getting bogged down in committee meetings and endless requests for more data. In contrast, a 2nd tier lender can often give you a green light in just a few days. This speed is crucial when you’re trying to secure a prime site in a competitive market before someone else snaps it up. This rapid pace of construction actually aligns with the goals of the NZ housing and urban development work programme, which aims to get more quality homes built faster across our communities to meet growing demand.

When to Stick with the Big Banks

Mainstream banks are perfect for developers who have plenty of runs on the board. If you’ve got high equity, a spotless credit history, and you’ve already secured pre-sales for 50% to 100% of your units, the bank’s lower interest rates make a lot of sense. You’ll pay less for your money, but you’ll pay for it in “red tape” and administrative hurdles. They’ll want to see every tiny detail of your professional team and your business before they say yes. It’s a low-cost option, but only if you’ve got the time and the patience to jump through every single hoop they hold up.

The Advantages of Non-Bank (2nd Tier) Funding

For many, especially those on their first or second project, a 2nd tier lender New Zealand offers a much smoother ride. They are far more flexible when it comes to pre-sales. In some cases, they might not require any at all. This allows you to start building sooner and potentially sell your units for a better price once they are finished and people can actually walk through them. While the interest rates are higher, usually 2-6% above bank rates, the trade-off is higher LVRs and interest-only periods that protect your cash flow. Many developers use this as a stepping stone, finishing the build with a non-bank lender and then refinancing to a cheaper bank loan once the project is finished. If you’re feeling stuck between these two worlds, chatting with an expert can help you see which path actually leads to a finished build.

The ‘Must-Haves’ for Approval: What NZ Lenders Are Looking For in 2026

When you apply for property development loans NZ lenders aren’t just looking at a patch of dirt or a set of drawings. They’re looking at you. Think of it like a job interview where the stakes are hundreds of thousands, or even millions, of dollars. Lenders fund the people behind the project as much as the project itself. They want to know that when things get tough, you’ve got the grit and the team to see the build through to the end. This means your personal track record and your financial “skin in the game” are the very first things they’ll check.

A clean credit history is non-negotiable for the big banks, and even second-tier lenders will look closely at any past hiccups. Beyond your credit, your equity position needs to be solid. Most lenders expect you to contribute at least 20% to 35% of the project’s total cost. They want to see that you’re just as committed to the success of the build as they are. Pre-sales remain the biggest hurdle for many developers in 2026. While some flexible lenders might let you start without them, mainstream banks often demand that 50% to 70% of the units are sold before they’ll release the first cent of funding. Managing this requirement often means working closely with a real estate agent early on to prove there’s genuine demand for what you’re building.

Organising Your Development Team

Lenders often care more about your builder than your architect. A beautiful design is great, but a builder with a reputation for finishing on time and within budget is what keeps a bank manager calm. You’ll also need a Quantity Surveyor (QS) on your side. The QS acts as the bank’s eyes and ears, verifying that the costs you’ve listed are realistic and that the work has actually been done before a progress payment is made. If this is your first project, don’t be afraid to bring in a mentor or a project manager with runs on the board. Citing resources like the Property Council New Zealand can help you stay up to date with industry standards and show lenders you’re serious about following best practices.

Financial Ratios You Need to Know

You’ll hear a lot of talk about LTC (Loan-to-Cost) and LVR (Loan-to-Value). LTC is simply how much the bank will lend against the total cost of the build, while LVR is the percentage they’ll lend against the final value of the completed project. Gross Realisation Value (GRV) is the total expected sales price of all units including GST. Lenders use this figure to work out their overall risk. It’s also vital to include a contingency fund in your budget. We always recommend planning for a 10-15% cost blowout. Having this buffer built-in doesn’t just protect you from surprises; it shows the lender you’re a professional who understands that construction rarely goes perfectly to plan.

Your Roadmap to Funding: How to Organise Your Application

Getting your paperwork in order for property development loans NZ can feel like a project in itself. If you’ve ever felt overwhelmed by the sheer volume of documents requested, you aren’t alone. The secret is to stop thinking of it as a loan application and start viewing it as a business proposal. Lenders want to see that you’ve thought through every possible scenario, from the first digger on site to the final sale. Following a structured roadmap ensures you don’t miss the small details that could stall your funding.

The journey usually follows these five clear steps:

- Step 1: The Feasibility Study. This is your foundation. You need to prove the numbers actually stack up before you even think about approaching a bank.

- Step 2: Broker Consultation. Instead of knocking on every door yourself, we scout the market to find the lender whose current “appetite” matches your specific project.

- Step 3: The Pitch Deck. You’ll need your resource consents, builder contracts, and professional bios ready to go. This is where you sell the “story” of your project.

- Step 4: The Funding Offer. Once a lender says yes, you’ll get an offer with “conditions precedent.” These are things like a final valuation or reaching a certain number of pre-sales.

- Step 5: Settlement and First Draw. This is the finish line. Your legal team handles the settlement, and you get your first progress payment to start the work.

The Power of a Feasibility Study

A good feasibility study is more than just a budget. It needs to account for the GST on your sales, council levies, and the marketing costs required to find buyers. If your plan is to keep the units once they’re built, you should use residential investment property loans NZ as a baseline for your long-term exit strategy. This shows the lender you’ve considered how you’ll move from a high-interest construction loan into a more sustainable long-term mortgage once the build is complete.

Avoiding Common Application Blunders

One of the biggest mistakes we see is underestimating “soft costs.” It’s easy to remember the timber and the concrete, but it’s the interest payments, legal fees, and professional consultants that often catch people out. You also need a rock-solid exit strategy. Lenders hate uncertainty, so you must be clear about whether you intend to sell the units or hold them as rentals. Finally, always be honest about your credit history. It’s much easier for us to work through a past issue if we know about it upfront rather than having the lender discover it during their final checks. If you want to make sure your application is bulletproof from day one, let’s talk about your project today.

Navigating the NZ Development Landscape with Mortgage Suite

Securing property development loans NZ isn’t just about spreadsheets; it’s about the people who represent you. At Mortgage Suite, we don’t just pass your papers across a desk and hope for the best. Our director, Krish Krishna, brings over 20 years of deep banking experience to every project we handle. Having spent two decades on the other side of the lending fence, Krish knows exactly how credit managers think. He understands what makes them nervous and, more importantly, what gives them the confidence to say “yes.” This insider knowledge is your secret weapon when you’re trying to fund a project in a fluctuating market.

We act as your translator. Often, a great project gets rejected simply because it wasn’t presented in a language the bank understands. We take your vision, your numbers, and your track record, and we package them into a professional proposal that highlights the strengths of your deal. We specialise in those “tough” deals that mainstream banks might put in the “too hard” basket. Where a big bank might see a problem with a lack of pre-sales or a unique site, we see a solution through our network of flexible 2nd tier lenders. Our commitment is to a partnership that goes beyond just signing a loan document; we’re here to see your project through to completion.

From First Home to First Development

Many of the successful developers we work with didn’t start with a multi-unit block. They started with a single property and a dream. We love helping investors transition from being passive owners to active developers. By linking your current portfolio to new funding opportunities, we can help you unlock equity you might not even realise you have. Even if you’re just starting out, we can help first home buyers in New Zealand lay the groundwork today for a future in development. It’s about building a long-term plan where your success is our priority.

Ready to Get Cracking on Your Next Project?

With the Official Cash Rate sitting at 2.25% as of May 2026 and new housing targets always on the horizon, this year is full of opportunity for those who have their finance ready to go. Don’t let a “no” from a big bank be the end of your development dreams. The value of a no-obligation chat is that it gives you a clear picture of where you stand right now and what you need to do to get where you want to be. It’s about removing the obstacles so you can focus on what you do best: building.

We’re more than just brokers; we’re your advocates and negotiators. We stay with you from the first application until the final unit is sold and the loan is cleared. If you’re ready to get your project off the ground with a team that truly cares about your results, get in touch with us today. Let’s find the right path to fund your next build together.

Build Your Future with Confidence

Securing the right funding is the foundation of any successful build. Success in this market involves more than just finding a good site; it requires a bulletproof feasibility study and a development team that lenders can trust. Whether you’re aiming for the lower rates of a mainstream bank or the speed and flexibility of a second tier lender, the key is to present your project in a way that makes sense to the credit managers holding the purse strings.

Navigating the various property development loans NZ has to offer can feel complex, but you don’t have to do it alone. With over 20 years of banking and mortgage expertise, we specialise in handling the tough, complex commercial deals that others often avoid. We take pride in being your personal advocate, using our deep industry knowledge to negotiate directly with all NZ lenders on your behalf.

If you’re ready to get your project moving, talk to Krish Krishna about your property development funding today. We’re here to provide the steady hand and seasoned advice you need to see your project through to completion. Your next project is closer than you think, and we’re ready to help you make it happen.

Frequently Asked Questions

Can I get a property development loan with no experience?

Yes, you can, but you’ll need to surround yourself with a professional team that has plenty of runs on the board. Lenders look at the experience of your builder and project manager to offset your lack of history. If your team is solid and your feasibility study is airtight, a lender is much more likely to give you a fair go on your first project.

How much deposit do I need for a development loan in NZ?

Lenders generally expect you to contribute between 25% and 40% of the total project cost. While mainstream banks typically fund 60-75% of the build, some flexible 2nd tier lenders might allow a smaller deposit if the project shows a very strong profit margin. Using existing equity in other properties is a common way to cover this requirement without needing cash.

What are the current interest rates for property development loans?

Interest rates for property development loans NZ vary depending on the lender’s risk assessment. Mainstream banks usually charge between 1% and 4% above their standard mortgage rates. For 2nd tier or private lenders, you should expect total interest costs to range from 8% to 15% given the extra flexibility and speed they provide compared to traditional banks.

Do I need pre-sales to get a development loan?

It depends on which lender you approach. Mainstream banks often demand that 50% to 70% of the units are sold before they’ll release any funding for construction. However, many non-bank lenders don’t require any pre-sales at all. This allows you to start building immediately and potentially sell the finished units for a higher price once the project is complete.

How do progress payments work during construction?

Money is released in stages as your build hits specific milestones, such as the floor slab being poured or the roof being installed. A Quantity Surveyor will visit the site to check the work is done correctly before the bank releases the next payment. This ensures the funds are only used for actual progress, keeping both you and the lender protected throughout the build.

Can I use my existing home equity for a development project?

Yes, leveraging the equity in your current home or investment portfolio is one of the most effective ways to fund a project. By using the value you’ve already built up, you can often cover the required deposit without having to find a large amount of physical cash. This makes it much easier for established homeowners to transition into property development.

What happens if my construction costs go over budget?

If your costs increase, you’ll first tap into your contingency fund, which we always recommend setting at 10% to 15% of the total build cost. If you go beyond this buffer, you’ll need to either provide more of your own cash or talk to us about negotiating a loan increase. Having a professional advocate helps when presenting these cost changes to your lender.

Is it better to use a bank or a non-bank lender for my first project?

For a first project, a non-bank lender is often the better choice despite the higher interest rates. Their flexibility and willingness to fund projects without pre-sales mean you can get started faster and build your track record. Once you’ve successfully finished a few projects, you’ll find it much easier to meet the stricter criteria and lower rates offered by mainstream banks.