Low Doc Home Loans NZ: The 2026 Guide for Self-Employed Kiwis

What if the true value of your business wasn’t hidden behind a stack of two-year-old tax returns, but was found in the actual success you’re seeing right now? For many self-employed Kiwis, the dream of owning a home often feels like it’s on hold because mainstream banks refuse to look past rigid, traditional criteria. It’s frustrating to feel like your hard work doesn’t count just because your paperwork looks a bit different. While the market for low doc home loans nz has changed significantly under recent lending laws, the path to approval is still very much open if you know which doors to knock on.

I understand the anxiety that comes with a potential decline, which is why I’ve put together this updated 2026 guide to help you navigate the shift toward “Alt Doc” lending. You’ll discover how to secure a home loan using alternative proof like GST returns or bank statements, allowing you to move forward without waiting on the IRD. We’ll explore the specific documents that actually carry weight today and how to partner with lenders who appreciate business growth. By the end of this article, you’ll have a clear, stress-free strategy to get your application over the line and finally settle into your new home.

Key Takeaways

- Understand why the shift from “Low Doc” to “Alt Doc” means you can now use alternative proof like GST returns to show your true business income.

- Learn how to organise your bank statements and trading history to give lenders a clear, honest picture of your business’s success.

- Discover why 2nd tier lenders often provide the flexibility you need, even if you only have a 20% deposit or a shorter trading history.

- See how an expert broker acts as your advocate, packaging your application for low doc home loans nz to ensure it stands out to the right lenders.

- Find out how to clear common hurdles like credit blips or a short time in business so you can move forward with confidence.

What is a Low Doc Home Loan in New Zealand Today?

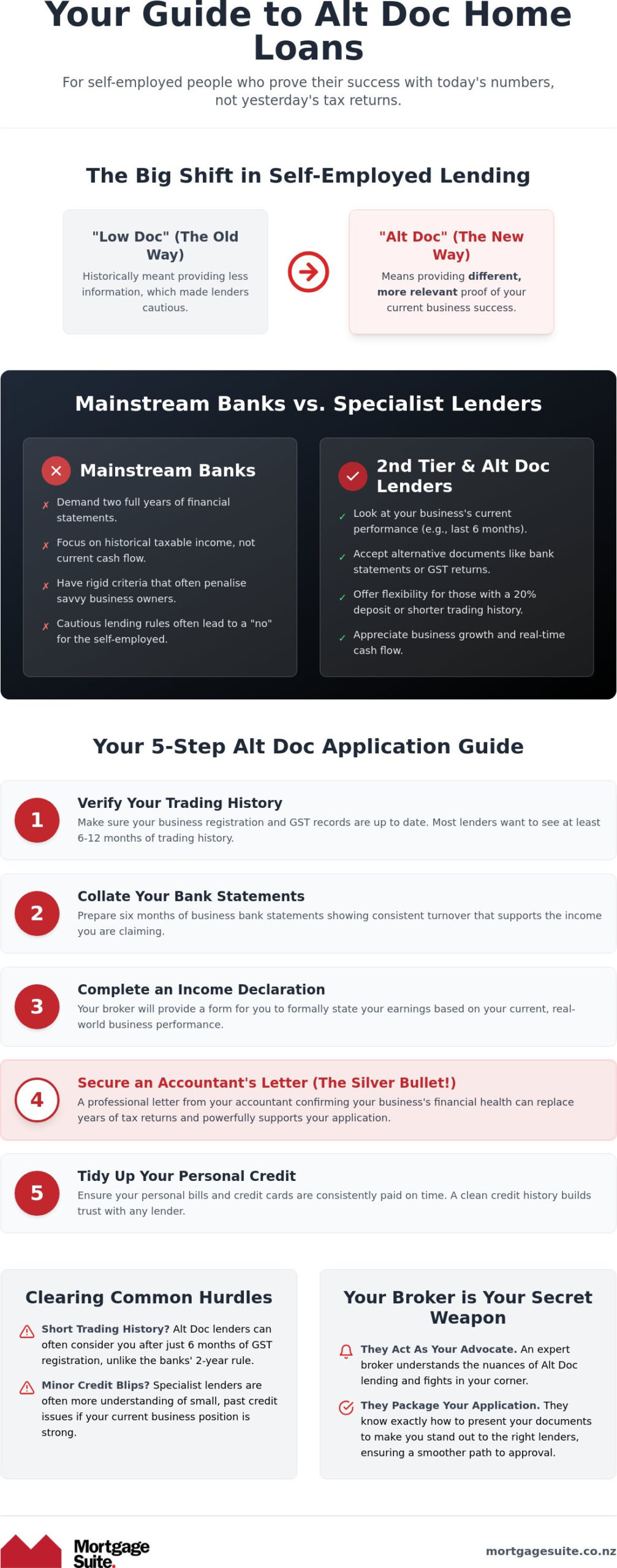

When you’re running your own show, your finances don’t always fit into a neat little box. A home loan for the self-employed shouldn’t depend on whether you have a perfect set of tax returns from two years ago. In the current market, low doc home loans nz have evolved into what we now call “Alt Doc” or alternative documentation loans. This doesn’t mean you’re providing “less” information; it means you’re providing “different” information that better reflects your current success. It is a way to prove your income using real-time data rather than historical tax records.

Historically, a low-documentation loan (low-doc) might have carried a different reputation, but in 2026, it’s a legitimate strategy for contractors, freelancers, and small business owners who have been GST registered for at least six months. It’s vital to understand that “low doc” is never “no doc”. Lenders still have a legal duty to ensure you can comfortably handle your repayments. They just use different tools to verify your income, such as your business bank statements or GST filings, to get a clear picture of your actual earnings.

Why traditional banks often say no

Most mainstream banks still cling to the “two-year rule”. They want to see two full years of financial statements and personal tax summaries before they even consider your application. The problem is that many savvy business owners use legal expenses to lower their taxable income. While this is great for your tax bill, it can make you look like you aren’t able to afford the repayments on paper when a bank calculates your borrowing power. Added to this is the impact of the CCCFA, which has forced banks to become incredibly cautious and rigid with their lending criteria, often leaving self-employed Kiwis out in the cold.

The rise of Alt Doc lending in 2026

The rise of Alt Doc lending is the biggest change for low doc home loans nz in 2026. This is where 2nd tier lenders have stepped up to fill the gap. Instead of looking at what happened in 2024, these lenders focus on your business’s current cash flow. They prioritise your valid NZBN and active GST status over ancient paperwork. By looking at your last six months of trading, they get a real-time view of your ability to manage a loan. If you want to see how these lenders operate, our 2nd tier lender New Zealand guide provides more detail on how they bridge the gap between rigid bank rules and your reality.

How to Prepare Your Alt Doc Application: A 5-Step Guide

Getting your ducks in a row before you talk to a lender is the best way to avoid the stress of a back-and-forth process. While the term low doc home loans nz might suggest a lack of paperwork, the secret to a quick approval is having the right alternative documents ready from the start. Follow these five steps to present a professional, clear case for your business success.

- Step 1: Verify your trading history. Ensure your NZBN is active and your GST records are up to date. Most lenders want to see you’ve been trading for at least six months to a year.

- Step 2: Pull your bank statements. You’ll need six months of business bank statements. These should show a consistent turnover that matches the income you’re claiming.

- Step 3: Complete a declaration form. Your broker will provide a “Self-Employed Declaration of Income”. This is a formal document where you state your earnings based on your current business performance.

- Step 4: Secure an accountant’s letter. A professional letter from your accountant can be a powerful substitute for traditional tax returns.

- Step 5: Tidy up your personal credit. Small blips can happen, but ensuring your personal bills and credit cards are paid on time helps build trust with the lender.

The “Accountant’s Letter” advantage

A well-drafted letter from your accountant is often the “silver bullet” for Alt Doc applications. It needs to clearly state that your business is financially healthy, stable, and that you can afford the loan repayments without any struggle. This one page can effectively replace a year’s worth of tax returns because it provides professional validation of your current financial position. When you speak to your accountant, explain your home loan goals so they can focus the letter on your business’s ability to generate steady cash flow. It’s about showing the lender that your business isn’t just surviving, it’s thriving.

Proving income through bank statements

Lenders look at your business account to see the “rhythm” of your money. They want to see regular deposits that prove your turnover is stable. One common concern is large, one-off expenses, like buying a new van or a specialised piece of equipment. Don’t worry about these; we can often treat these as “add-backs”. This means we explain to the lender that these were one-time costs or non-cash expenses like depreciation, which shouldn’t count against your ability to pay a mortgage. If you’re unsure how your statements look, talking to the team at Mortgage Suite Ltd early on can help you identify and explain any potential red flags before the lender ever sees them.

Mainstream Banks vs. 2nd Tier Lenders: Comparing Your Options

Choosing between a big bank and a 2nd tier lender isn’t just about comparing interest rates; it’s about finding a partner who actually wants to hear your business’s story. Mainstream banks often rely on rigid, computer-based systems that look for reasons to say no if your tax returns don’t meet their exact standards. In contrast, 2nd tier lenders are built for the complex reality of running a business. While you’ll generally need a 20% deposit for low doc home loans nz, the flexibility you gain is often the key to getting your house keys sooner rather than later.

The trade-off for this flexibility is usually a slightly higher interest rate. However, it’s vital to look at the bigger picture. Non-bank lenders often move much faster than the “big four” banks, with some approvals coming through in a matter of days. When you’re trying to secure a property in a competitive market, that speed is a massive advantage. You aren’t just paying for a loan; you’re paying for the ability to act quickly and bypass the bureaucracy that stalls so many other buyers.

Think of an alternative loan as a bridge. It’s a stepping stone that gets you into the property market today. Once you’ve built up some equity and have those two years of financial statements the big banks crave, we can look at refinancing you back to a mainstream lender at a lower rate. This strategy prevents you from being locked out of the market while property prices continue to climb. It’s about getting the house now and fixing the rate later down the track.

When the bank says no, who says yes?

This is where the world of non-bank lenders in NZ truly shines. These institutions use a human-led loan assessment, which means a real person looks at your application instead of a computer simply rejecting it. They are far more comfortable with diverse income streams and business “add-backs”. For example, if your profit looks low because you claimed significant depreciation or had a one-off equipment purchase, a 2nd tier lender will often count those amounts back into your income, giving you a much higher borrowing capacity.

Understanding the costs involved

It’s important to be clear about the costs from the start. Alternative loans sometimes come with an establishment fee that you wouldn’t typically see at a mainstream bank. You need to weigh this cost against the “cost of waiting”. If property prices rise significantly while you’re waiting a year to get your tax returns ready, that delay could cost you far more than a one-off fee. Working with a broker ensures you find the most competitive non-bank rate available, making sure the path to your new home is as affordable as possible.

Common Hurdles for Self-Employed Borrowers (and How to Clear Them)

The journey to home ownership for a business owner often feels like an uphill battle against a system designed for employees. Even when your business is thriving, you might face obstacles that make a standard bank manager shake their head. Whether it’s a “messy” financial year or a lack of recent tax records, these challenges are common. The good news is that low doc home loans nz are specifically designed to clear these hurdles. By focusing on your current success rather than past setbacks, we can find a path forward that values your business’s potential.

One of the biggest roadblocks is a short trading history. While mainstream banks usually demand two full years of profitable tax returns, many alternative lenders are happy to consider your application if you’ve been in business for just six to twelve months. Another frequent concern is a rough patch in your business’s past. If an unexpected bill or a slow season caused a dip in your credit score, non-conforming home loans can provide a lifeline. These products are tailored for Kiwis who don’t fit the “perfect” borrower profile but have a solid plan to move forward.

Presenting your income correctly is also vital. You might pay yourself a mix of dividends and a small salary to be tax efficient. A bank might only look at the salary, but a specialist lender will look at the total business profit available to you. If you’re struggling with a deposit, remember that you can often use equity in other assets or even a gift from family to reach that 20% mark required for most Alt Doc products.

What if my tax returns aren’t filed yet?

It’s a common story; your business is flying, but your accountant hasn’t quite finished last year’s books. This isn’t the deal-breaker it used to be. We can use your latest GST returns as interim proof of income to show how your business is performing right now. Combined with management accounts from your software, like Xero or MYOB, we can tell a compelling story of your current financial health. Being behind on paperwork is a hurdle we can jump by using real-time data to prove you can afford the repayments.

The importance of a clean credit file

Small business owners often have “busy” credit files because they’re frequently applying for trade credit or equipment finance. This can sometimes look like a red flag to a computer, but a human lender understands the context. Before you apply, it’s a good idea to “polish” your file by ensuring all personal utilities and credit cards are paid on time. If there is a mark on your record, don’t panic. Often, a simple explanation of what happened and how you’ve fixed it is all a specialist lender needs to hear. If you’re ready to see how your business stacks up, you can explore your home loan options with us today.

Why a Mortgage Broker is Your Secret Weapon for Low Doc Loans

Applying for low doc home loans nz directly with a mainstream bank is often a recipe for disappointment. Banks rely on rigid systems that aren’t built to understand the ebbs and flows of business income. When you walk into a branch, you’re often met with a “computer says no” outcome simply because your tax returns aren’t current. This is where a broker becomes your most valuable asset. We don’t just pass on your documents; we act as your advocate, translating your business success into a language that lenders understand and respect.

Our role is to package your application so it highlights your strengths rather than your paperwork gaps. We know which 2nd tier lenders are “hungry” for new business and which ones are currently offering the most flexible terms for your specific industry. By having a seasoned negotiator in your corner, you avoid the stress of multiple declines and protect your credit file from unnecessary enquiries. We use our 20 plus years of industry experience to navigate the hurdles we’ve discussed, ensuring your application lands on the desk of a human underwriter who can see the real value in your business.

A personal approach to complex finance

Krish Krishna has spent over two decades helping Kiwis navigate the complexities of the lending market. At Mortgage Suite Ltd, we believe in a partnership that lasts well beyond your initial settlement. We don’t just get you a loan and walk away; we help you build a long-term strategy. As we mentioned earlier, an Alt Doc loan is often a stepping stone. We’ll work with you over the coming years to monitor your business growth and identify the perfect moment to refinance you back to a mainstream bank once you have the traditional records they require.

Getting started with Mortgage Suite Ltd

We know that the thought of hunting down bank statements and GST records can feel overwhelming when you’re already busy running a business. Our goal is to take that weight off your shoulders. It all starts with a relaxed, no-obligation chat to see where you stand and what your goals are. We’ll give you a clear, honest assessment of your options and handle the heavy lifting of the application process for you. Ready to talk about your self-employed home loan? Get in touch with Mortgage Suite Ltd today.

Take the First Step Toward Your New Home Today

Running a business is a significant achievement, and it shouldn’t be the reason you’re locked out of the property market. We’ve seen how the shift toward alternative documentation means you can use real-time proof, like your GST returns and bank statements, to show lenders you’re a safe bet. Securing low doc home loans nz in 2026 isn’t about having less proof; it’s about using the right proof to tell your story. Whether you’re dealing with a short trading history or complex income streams, there’s almost always a path forward when you have the right advocate in your corner.

At Mortgage Suite Ltd, we bring over 20 years of banking and brokerage experience to the table. We specialise in 2nd tier and non-bank lending, providing tailored solutions for complex self-employed income that mainstream banks often overlook. You don’t have to navigate this paperwork hunt alone. We’re here to help you bridge the gap between your business success and your home ownership goals. Book a free consultation with our self-employed loan experts and let’s get your application moving. You’ve done the hard work of building your business; now let us do the hard work of securing your home.

Frequently Asked Questions

Can I get a low doc loan with only a 10% deposit in NZ?

The short answer is usually no. Most lenders providing low doc home loans nz require at least a 20% deposit because they are taking on more risk by not seeing your full tax returns. While some mainstream bank loans allow for a 10% deposit, those almost always require two years of perfect financial statements, which is exactly what Alt Doc products help you avoid.

Do low doc home loans have higher interest rates?

Yes, you’ll generally find that interest rates are slightly higher than standard bank rates. For example, as of July 2026, some specialist floating rates start around 7.65% p.a., while prime Alt Doc options might start closer to 5.64% p.a. You’re essentially paying a small premium for the flexibility and speed that a non-bank lender provides when your paperwork isn’t ready for a traditional bank.

How long do I need to be self-employed before I can apply for an alt doc loan?

You typically need to have been trading and GST registered for at least six months. While traditional banks almost always demand a two-year history, many 2nd tier lenders are happy to look at your business once you’ve crossed that six-month mark. They’ll use your interim GST returns and bank statements to prove that your business is stable and growing.

Is a low doc loan the same as a bad credit loan?

No, they are two different things. A low doc loan is for business owners with a strong income who simply don’t have up-to-date tax returns. A bad credit, or non-conforming loan, is designed for people who have had defaults or missed payments in the past. It’s possible to have a loan that is both Alt Doc and non-conforming, but they solve two different problems for the borrower.

What documents replace a tax return in a low doc application?

Lenders usually look for three main things: six months of business bank statements, your most recent GST returns, and a signed declaration of your income. An accountant’s letter confirming your business is profitable and solvent is also a very powerful document that can speed up your approval. These pieces of evidence give the lender a real-time view of your actual cash flow.

Can I use a low doc loan to buy an investment property?

Yes, you can certainly use these loans for residential investment properties. The main difference is that the deposit requirements might be slightly higher than for a home you plan to live in. While 20% is standard for owner-occupiers, some lenders might ask for a 25% deposit for an investment property to offset the extra risk.

Will a low doc loan allow me to refinance later?

Refinancing is actually the goal for most of our self-employed clients. You can use an Alt Doc loan to get into your home now, and then once you have two years of clean tax returns, we can look at moving you to a mainstream bank. This “stepping stone” strategy allows you to stop paying rent and start building equity while you get your long-term paperwork in order.

Do I need an accountant to get a low doc home loan?

While it isn’t always a strict legal requirement, having an accountant makes the process much smoother. Many 2nd tier lenders will ask for an “Accountant’s Letter” to verify your earnings. If you don’t have an accountant, we can still work with your bank statements and GST filings, but a professional letter often provides the extra level of trust that secures a faster approval.