What if the bank’s “no” isn’t actually the end of your home-buying journey, but just a sign you’re looking in the wrong place? It is incredibly disheartening to feel like a mere tick-box on a spreadsheet, especially when a slightly messy credit history or self-employed income makes you “too hard” for traditional lenders. Finding a 2nd tier lender New Zealand wide can be the breakthrough you need, offering a common-sense approach that looks at your whole financial picture rather than just a computer-generated score.

We understand the anxiety that comes with being turned away, but these alternative options are designed for people who need a partner, not just a processor. This guide explores how to secure a flexible home loan that respects your unique situation, providing a fair go when the big banks won’t budge. You will discover exactly how these lenders operate in 2026, the specific benefits they offer for non-standard financial profiles, and how to create a clear strategy for eventually refinancing back to a mainstream bank once your circumstances settle.

Key Takeaways

- Understand that 2nd tier lenders are professional, legitimate institutions that offer a genuine alternative when big banks won’t help.

- Discover how a 2nd tier lender New Zealand wide uses a common-sense approach to look at your whole financial picture rather than just ticking boxes.

- Learn why flexibility often comes with a slightly higher interest rate and how the speed of these lenders can save your property deal.

- Find out how to organise a professional paper trail and why being upfront about your history helps secure a faster approval.

- Explore how seasoned expertise can bridge the gap between rigid banking rules and your personal goal of home ownership.

What is a 2nd Tier Lender in New Zealand?

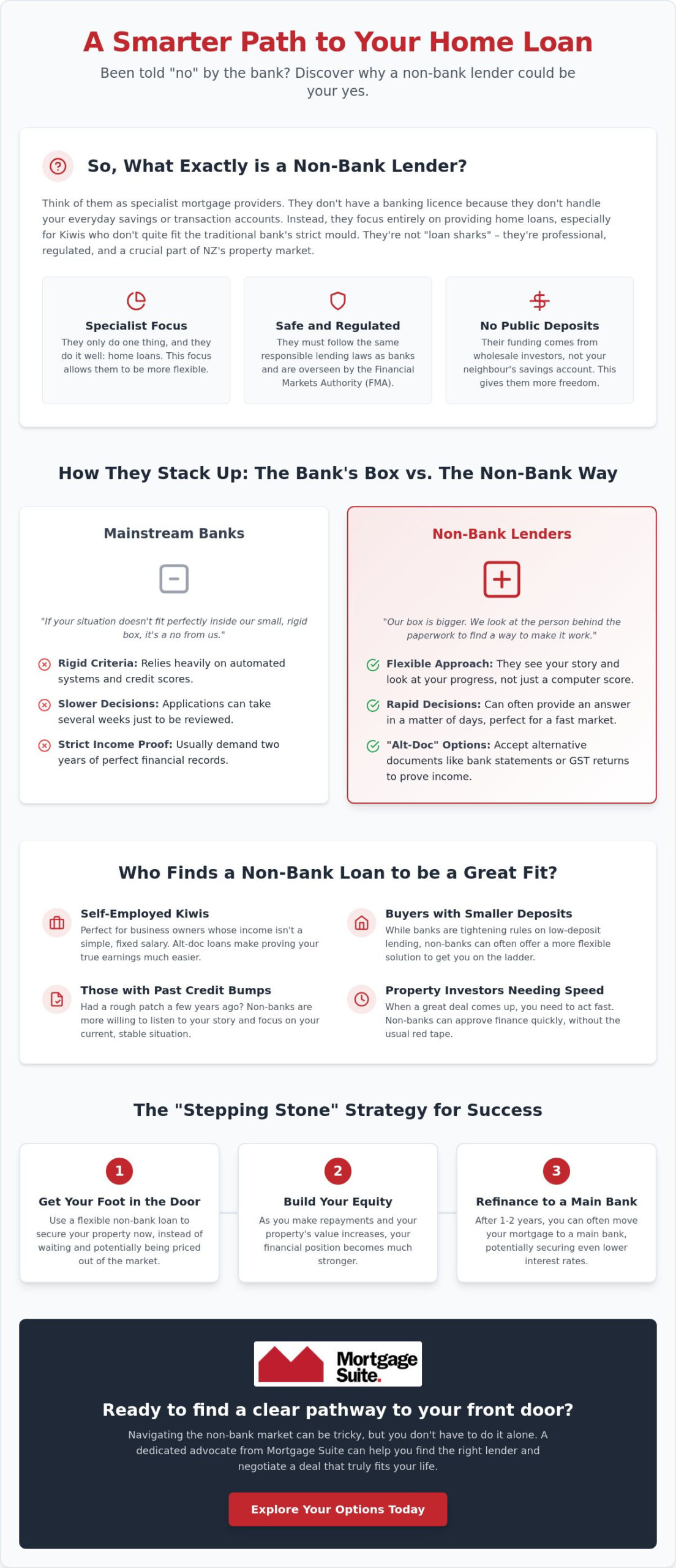

Think of a 2nd tier lender as a specialised financial institution that focuses purely on helping people secure property. Unlike the big banks you see on every street corner, these organisations don’t offer everyday savings accounts, credit cards, or travel insurance. They aren’t “retail banks” in the traditional sense; instead, they are professional lenders who use their own capital or institutional funds to provide mortgages. This narrow focus is actually their greatest strength because it allows them to be far more flexible than a bank that’s trying to be everything to everyone.

The main difference you’ll notice is the way they look at your application. While big banks often rely on rigid computer algorithms that spit out a “yes” or “no” based on strict “tick-box” criteria, a 2nd tier lender New Zealand homeowners use often applies a common-sense approach. They’re interested in the “why” behind your financial situation. If you’re self-employed and your income fluctuates, or if you had a minor credit hiccup a few years ago, these lenders are more likely to look at the big picture rather than just the numbers on a screen. They provide a vital alternative for Kiwis who have the ability to pay a mortgage but don’t quite fit the narrow mould of mainstream banking.

Non-Bank vs. 2nd Tier: Is there a difference?

No worries if you’re a bit confused by the different names; they basically mean the same thing in our local market. “Non-bank” describes their legal structure, meaning they are a non-bank financial institution that doesn’t hold a full banking licence from the Reserve Bank. “2nd tier” describes their position as a secondary option to the “Big Four” banks. Whether you call them non-banks or 2nd tier, the result is the same: a professional lender that offers a different path to home ownership.

Why they are a safe bet for Kiwis

Some people worry that stepping away from a big bank means less protection, but that isn’t the case. Every 2nd tier lender New Zealand has must follow the Credit Contracts and Consumer Finance Act (CCCFA). This means they are legally required to be responsible lenders, just like the household names. These institutions have been a solid part of our property market for decades. Many are backed by massive global investment firms or well-known local institutions, ensuring they have the stability and reputation to support your long-term goals. They aren’t “last resorts” but rather strategic partners for those who need a more personalised touch.

Why the Mainstream Banks Might Say ‘No’

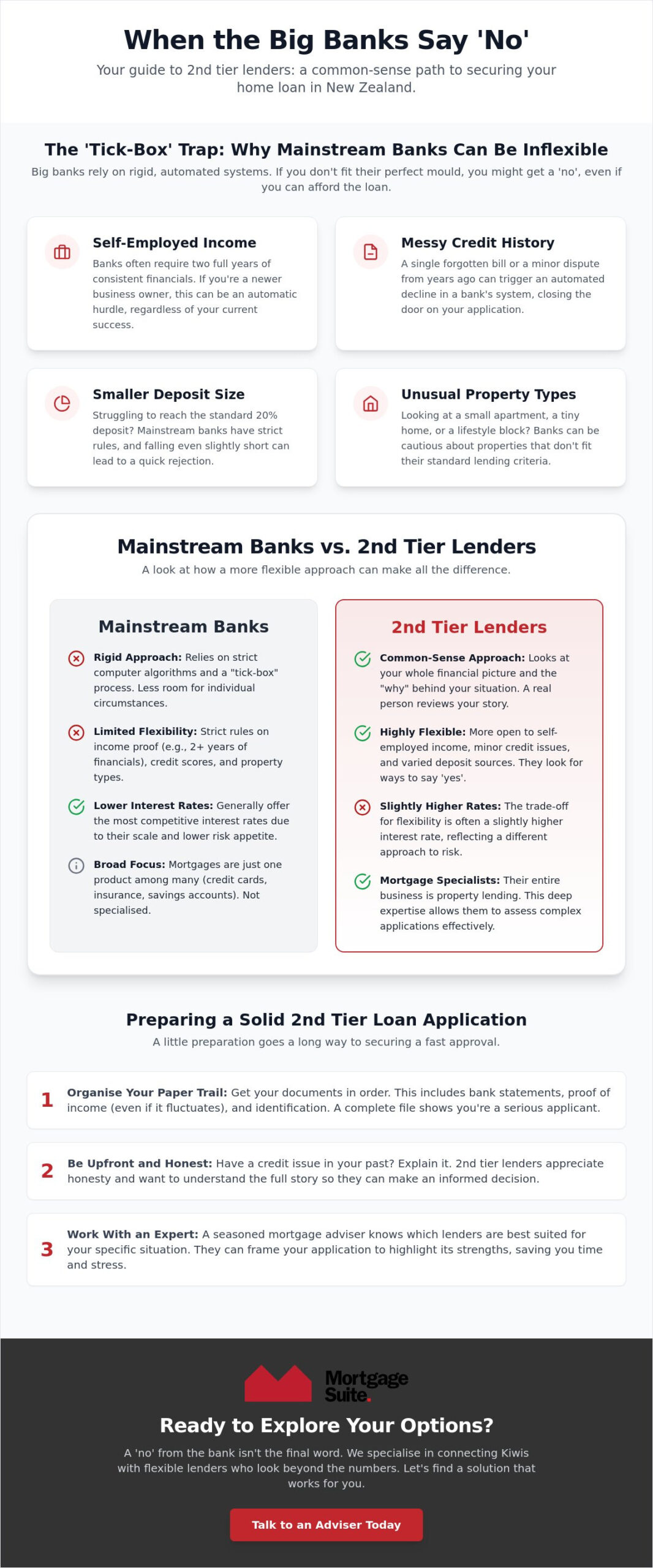

It’s a sinking feeling when you’ve done everything right, saved your deposit, and found the perfect home, only to have a bank manager shake their head. The reality is that the Big Four banks are massive machines built for speed and volume. To keep things moving, they rely on rigid, one-size-fits-all rules. If your financial situation has even a tiny bit of “colour” or complexity, you often fall outside their very narrow appetite for risk. A “no” from a mainstream lender usually isn’t a reflection of your ability to pay; it’s simply a sign that you don’t fit their specific, pre-programmed mould.

This is where a 2nd tier lender New Zealand wide provides a much-needed alternative. While banks look for reasons to say no to protect their high-volume systems, 2nd tier lenders look for reasons to say yes. They take the time to understand the story behind the numbers. They recognise that modern lives are rarely tidy, and they’re willing to look at the big picture of your financial health rather than just a computer-generated score.

Common hurdles for the ‘Big Four’

There are several reasons why a perfectly capable borrower might get a “thanks, but no thanks” from a traditional bank. These hurdles are often non-negotiable for mainstream lenders:

- Self-employed income: Banks usually demand two full years of perfect financial records. If you’ve been in business for 12 months and are doing well, a bank might still decline you simply because you haven’t reached that two-year mark.

- Deposit size: With government rules often requiring a 20% deposit for owner-occupiers, many Kiwis find themselves just a few thousand dollars short.

- Credit history: A forgotten power bill from three years ago or a minor credit card dispute can stay on your file and trigger an automatic decline in a bank’s system.

- Property types: Banks are often wary of apartments under a certain size, tiny homes, or lifestyle blocks with unusual titles.

The ‘Tick-Box’ trap

Modern banking relies heavily on automated software. When you submit an application, an algorithm scans for specific data points. If one “box” isn’t ticked, the system can auto-decline the application before a person even looks at it. In contrast, the 2nd tier space relies on a human-led decision-making process. These are experienced professionals who can see that a past credit hiccup was a one-off event or that your self-employment income is stable and growing. This approach is the foundation for non-conforming loans, which are specialised products designed specifically for “out-of-the-box” situations that don’t meet standard bank criteria. If you’re feeling stuck in this tick-box trap, it might be time to talk to an expert who knows how to present your case to the right people.

Comparing 2nd Tier Lenders vs. Mainstream Banks

Choosing between a big bank and a 2nd tier option isn’t about finding a “better” lender, but rather the right lender for your current situation. Mainstream banks are great for people who fit a very specific profile and want the lowest possible interest rate. However, that low rate often comes with a lack of flexibility and a slow, complicated process. If you need a lender who can look past a messy bank statement or move quickly to secure a property, a 2nd tier lender New Zealand wide offers a level of service the big banks simply aren’t built to provide.

One of the biggest advantages is the personalised approach. You won’t find yourself stuck in a massive call centre queue or waiting weeks for a computer to process your paperwork. Instead, you’re working with people who understand that every borrower has a unique story. They can be far more creative with loan structures, such as offering longer periods where you only pay the interest. This can help with your cash flow while you’re getting established or finishing a renovation. It’s about finding a solution that fits your life, not forcing your life to fit their rules. For property investors in particular, this flexibility extends to residential investment property loans NZ borrowers use to grow their portfolios when mainstream banks won’t budge on LVR restrictions.

Interest rates and fees: The real story

Let’s be upfront about the trade-offs. Because these lenders take on more complex cases, their interest rates are generally higher than the “special” rates advertised by the Big Four. For many Kiwis, the slightly higher cost is a small price to pay for the value of actually getting the keys to their home. It’s often a short-term strategy to get into the market now rather than waiting years to save a larger deposit. To help with the initial costs, many of these lenders allow you to add the setup fees to your total loan balance, meaning you don’t need even more cash upfront to get the deal across the line.

Flexibility and Speed

Speed is where these lenders truly shine. While a big bank might take weeks to give you a definitive answer, a 2nd tier lender can often organise a conditional approval in as little as 48 hours. This is a game-changer if you’re trying to secure a property at auction or need a short-term loan to cover the gap between selling one home and buying another. They are experts in providing non-conforming home loans New Zealand families use to navigate tricky transitions. Whether it’s a short-term fix or a long-term plan, their ability to move fast ensures you don’t miss out on the right opportunity just because a bank’s internal rules changed overnight. This same speed and flexibility makes them a natural fit for those seeking property development loans NZ wide, where tight project timelines and complex income structures often rule out the big banks entirely.

How to Prepare a Solid 2nd Tier Loan Application

Getting your ducks in a row before you talk to a lender makes a world of difference. When you apply with a 2nd tier lender New Zealand wide, you aren’t just submitting a pile of numbers; you’re telling a story. These lenders are looking for a reason to say yes, but they need to see that you’re professional and organised. Gathering a clear paper trail is the first step to proving you’re a reliable partner who takes their finances seriously. It shows you’ve moved past the “too hard” basket and are ready to take control of your property journey.

Honesty is your best policy here. We always tell our clients that lenders hate surprises but they love honesty. If you have a bit of a colourful credit history or a period of low income, it’s much better to be upfront about it. When you explain the “why” behind a past mistake, it allows the lender to focus on your current ability to afford the repayments. They want to see that you have a stable income now and a clear plan for the future. This is where a mortgage broker becomes your best mate. We know exactly which lenders are comfortable with your specific situation and how to present your case so it stands out for the right reasons.

The ‘Exit Strategy’: Planning your return to the bank

Think of this loan as a bridge, not a destination. You don’t necessarily need a 2nd tier loan for a full 30-year term. Instead, many Kiwis use these products for 12 to 24 months to “clean up” their financial profile. During this time, you can prove a stable income or wait for old credit marks to fall off your record. Once your situation has settled, Mortgage Suite Ltd can help you refinance back to a mainstream bank with a lower rate. You can learn more about how this transition works in our guide to non-bank lenders nz.

The documentation you’ll need

To give yourself the best chance of a fast approval, you’ll need to have your paperwork ready to go. Lenders will look closely at your recent bank statements to check how you manage your bank accounts. They want to see that you’re handling your money well, without unarranged overdrafts or missed payments. You’ll also need to prepare:

- Proof of deposit: This could be your savings, a gift from family, or equity you’ve built up in another property.

- Income verification: For those who work for themselves, this might include recent sets of accounts or GST returns to show your business is healthy.

- A written explanation: A short, honest note explaining any past credit issues helps you get ahead of the lender’s questions and shows you’re proactive.

If you’re ready to stop guessing and start moving forward with a plan tailored to you, the best next step is to get in touch for a personalised chat about your options.

How Mortgage Suite Ltd Connects You to Alternative Funding

At Mortgage Suite Ltd, we believe everyone deserves a fair go at owning a home. Our founder, Krish Krishna, brings more than 20 years of deep banking experience to your side of the table. This isn’t just a number on a CV; it’s your secret weapon. Because Krish has spent two decades understanding the inner workings of the financial world, he knows exactly how to navigate the systems that often feel like a maze to everyday Kiwis. He has seen the process from both sides and knows what it takes to get a deal across the line.

Our role is to act as a bridge between you and the right 2nd tier lender New Zealand has available. We take your complex situation, whether you’re self-employed, have a non-standard income, or a few credit marks, and ‘translate’ it into a language that lenders understand and respect. We don’t just pass on your paperwork. Mortgage Suite Ltd builds a professional case for you, highlighting your strengths and providing clear context for any past hurdles. This hands-on approach often makes the difference between a quick decline and a solid approval. Our process is built on several key advantages:

- Direct access to a wide range of lenders you won’t find on the high street.

- Deep knowledge of “hidden” lending criteria that changes from month to month.

- A proactive attitude toward overcoming obstacles that stop big banks in their tracks.

- A long-term commitment to your financial success, not just a one-off transaction.

Expert negotiation on your behalf

We don’t just stop at the first “yes” we receive. Our goal is to fight for the best possible terms for your specific needs. Because Mortgage Suite Ltd has established relationships with a huge range of lenders across the country, we have access to options that the general public cannot reach directly. Every lender has its own unique appetite for risk at any given time. We know which ones are looking for your type of deal right now. From the top of the North Island to the bottom of the South, we provide national reach for all types of property loans, including residential investment property loans NZ investors need to unlock equity and grow their portfolios in 2026, ensuring you get a solution that works for your long-term goals.

Ready for a fair go?

If you’ve been turned away by your bank, please remember that it’s just a detour, not the end of the road. We invite you to reach out for a confidential, judgment-free chat about your situation. Mortgage Suite Ltd has seen every possible scenario and we know how to find a path forward. Our commitment is to partner with you for your long-term financial success, helping you get into your home now while planning for your eventual return to a mainstream bank. When you’re ready to explore what’s possible, you can book a consultation with our team. Let’s get to work on making your home ownership goals a reality.

Your Path to Home Ownership Starts Here

Securing a mortgage doesn’t have to be a stressful battle against a bank’s rigid computer system. Alternative options provide the flexibility and common-sense approach that modern Kiwis need to move forward. Whether you’re navigating self-employment income or a non-standard credit history, finding the right 2nd tier lender New Zealand wide can be the bridge that gets you into your home sooner rather than later. By focusing on a clear exit strategy and preparing a professional application, you can turn a bank’s decline into a successful new beginning.

With over 20 years of banking and mortgage expertise, Mortgage Suite Ltd specialises in these complex, non-conforming loans. Our founder-led service ensures you receive personalised attention from someone who truly knows how to negotiate with alternative lenders to get the best possible result for your situation. You don’t have to figure this out on your own. Chat with Mortgage Suite Ltd about your 2nd tier loan options today and let us help you find a fair go in the property market. Your dream home is still within reach, and we’re here to help you secure it.

Frequently Asked Questions

Is a 2nd tier lender safe to use in New Zealand?

Yes, they are completely safe and professional organisations. Every 2nd tier lender New Zealand has must comply with the Credit Contracts and Consumer Finance Act (CCCFA). This ensures they follow strict responsible lending rules just like the big banks. Many are backed by large investment firms; providing a secure and regulated environment for your home loan. You can feel confident that your rights are protected under New Zealand law.

Will my interest rate be much higher with a 2nd tier lender?

Generally, yes, the interest rates are slightly higher than those offered by mainstream banks. This reflects the extra flexibility they provide and the higher risk they take on. However, for many people, the small increase in cost is a fair trade for actually getting into a home. It is often a short-term solution while you work toward qualifying for a standard bank rate in the future.

Can I move back to a mainstream bank later on?

Absolutely, and for most clients, this is the ultimate goal. We often set up these loans with a 12 to 24 month plan in mind. Once you have built up more equity or cleaned up your credit history, we can help you refinance back to a mainstream bank. This “exit strategy” ensures you aren’t paying a higher rate for any longer than you actually need to.

Do 2nd tier lenders require a bigger deposit?

Not necessarily. In some cases, a 2nd tier lender New Zealand wide might actually be more flexible with deposit sizes than a big bank. While banks are often restricted by tight government rules on low-deposit lending, alternative lenders have more freedom to look at your individual situation. They focus more on your ability to make the repayments rather than just the cash you have upfront.

How long does it take to get a 2nd tier loan approved?

These lenders are typically much faster than traditional banks. You can often get a conditional approval within 48 hours, whereas a big bank might take two weeks or more. Because they are smaller and more focused, they don’t have the same layers of bureaucracy. This speed is a huge advantage if you are trying to buy a property at auction or have a tight deadline.

Can I get a 2nd tier loan if I’m self-employed?

Yes, they are often the best option for business owners and contractors. Banks often demand two years of perfect financial records, which many self-employed Kiwis don’t have. Alternative lenders are happy to look at other proof of income, such as GST returns or recent bank statements. They understand how business income works and won’t penalise you for having a complex financial structure.

What happens if I have bad credit history?

They take a common-sense approach to your past. Instead of an automatic “no” from a computer, a human will look at why the credit issue happened and what has changed since then. If you can show that you are back on track and can afford the loan now, they are often willing to help. It’s about your current character and ability to pay, not just a past mistake.

Are 2nd tier lenders the same as ‘payday’ lenders?

No, they are completely different. Payday lenders offer very small, high-interest loans for a few weeks. In contrast, 2nd tier lenders provide long-term property finance and mortgages. They are professional financial institutions that offer competitive alternatives to the big banks. They are a legitimate part of the New Zealand property market and help thousands of families secure their own homes every year.