Does it feel like the New Zealand property market has a “couples only” sign hanging on the front gate? If you’ve been scrolling through listings and feeling like the dream of home ownership is out of reach, you aren’t alone. Many people believe that buying a house on a single income nz is impossible in 2026, especially with the national median house price sitting at $770,000. It’s exhausting to deal with strict rules at big banks about how much you owe compared to what you earn, but your journey doesn’t have to end at a “no” from a mainstream lender.

We understand how frustrating it is to be told you don’t fit the box when you’re ready to settle down. This guide is here to change that narrative. You’ll discover how to navigate the current market and secure a home loan on your own; we’ll show you the paths that the big banks often fail to mention. We are going to provide a clear roadmap to ownership, explaining friendly ways to borrow money and giving you the confidence to start your application with a steady hand guiding you through the process.

Key Takeaways

- Learn why solo home ownership is still a realistic goal in 2026 and how to move past the common hurdles that big banks often put in your way.

- Discover practical ways to boost your borrowing power, ensuring that buying a house on a single income nz remains a realistic and achievable goal.

- Find out why non-bank and 2nd tier lenders are often the best choice for solo buyers who don’t fit the strict criteria of mainstream institutions.

- Follow a clear, five-step roadmap to organise your finances and maximise your deposit using tools like your KiwiSaver savings.

- Understand the value of having a dedicated expert act as your personal negotiator to open doors to loan options that aren’t usually available to the general public.

Can You Really Buy a House on a Single Income in NZ?

Let’s be honest about the situation. If you’ve spent any time looking at the history of Housing in New Zealand, you’ve probably felt that sinking feeling that the system isn’t built for you. Banks often view a solo applicant as a “single point of failure.” They worry that if you lose your job or get sick, there isn’t a second person to pick up the financial slack. But here is the good news: buying a house on a single income nz is absolutely achievable in 2026 if you have the right strategy and a bit of expert advocacy on your side.

You actually have a secret weapon that couples often lack; total financial control. When you’re on your own, you don’t have to negotiate lifestyle choices or manage a partner’s hidden debts. You decide exactly how much goes into your savings and how much is allocated to your future mortgage. This level of discipline is incredibly attractive to lenders. It shows you’re a responsible borrower who can manage a tight budget without the complications of a second person’s spending habits. By proving you can live comfortably on your own terms, you demonstrate a level of stability that many dual-income households struggle to maintain.

The Reality of the 2026 NZ Property Market

The market right now is showing some interesting shifts that favour the patient buyer. The national median house price was $770,000 in June 2026, which represents a 1.3% drop from the previous month. While major banks like ANZ and ASB increased their floating rates by 0.25% to reach 6.04% in July, fixed rates have remained more competitive for those with a solid deposit. For a solo buyer, a “softer” market in cities like Auckland and Wellington means you have more room to breathe. You aren’t being outbid at every auction by frantic couples, which makes this a unique window to secure an entry-level home while prices are relatively flat.

Breaking the “Double Income” Myth

You don’t need a partner’s salary to prove you’re a safe bet for a home loan. Lenders are increasingly focused on your “character” as a borrower. If you have stable employment and a clean credit history, you’re already ahead of the pack. Banks want to see that you’ve been consistent with your savings and that you’ve minimised your personal debts like credit cards or car loans. It’s not just about the total figure on your payslip; it’s about how much of that income is left over once your weekly bills are paid. Showing a clear, disciplined track record of living within your means is the best way to prove that you can handle the responsibility of a mortgage alone.

Maximising Your Borrowing Power as a Solo Buyer

When you’re the only one signing on the dotted line, every dollar of your income needs to work twice as hard. Banks aren’t just looking at your total salary; they’re obsessed with your spare cash after bills. This is the money left over after you’ve paid for your groceries, your gym membership, and your Friday night takeaways. If you want to succeed at buying a house on a single income nz, you need to show the bank that you have plenty of breathing room in your budget. It’s about presenting a polished financial version of yourself that says you’re a low-risk, high-reliability borrower who isn’t living paycheque to paycheque.

One of the fastest ways to boost your borrowing limit is to clear away small debts. You might think a $2,000 credit card limit or a small Buy Now Pay Later balance isn’t a big deal, but lenders see it differently. They often calculate your borrowing power as if those credit limits are fully spent, which can slash tens of thousands off your maximum loan amount. Closing these accounts six months before you apply can make a massive difference to your application’s strength. You can find more detail on preparing your finances in the New Zealand Government’s guide to buying a house, which outlines the standard steps for any buyer.

Using KiwiSaver and Government Schemes

Your KiwiSaver is likely your biggest asset right now. If you’ve been a member for at least three years, you can usually access a KiwiSaver first home withdrawal NZ to put towards your deposit. While the First Home Grant was discontinued in May 2024, you should still check your First Home Grant NZ eligibility only to confirm that you should instead be looking at the First Home Loan scheme. This scheme is a lifesaver for solo buyers in 2026, allowing you to buy with just a 5% deposit if your income is $95,000 or less (or $150,000 if you have dependents). This significantly lowers the barrier to entry for those who are saving on their own.

The Balance Between Your Debt and Earnings

In 2026, banks are keeping a very close eye on the balance between your debt and earnings. This is a simple sum where the lender compares your total debt to your gross yearly income. Most mainstream banks have a limit on how high this can go, which can be a hurdle for single earners with even moderate personal debt. To improve your position, focus on reducing any existing car loans or personal debts before you approach a bank. If the big banks’ rules are too tight for your specific situation, working with an expert at Mortgage Suite Ltd can help you find alternative lenders who offer more flexibility for your specific income level and financial goals.

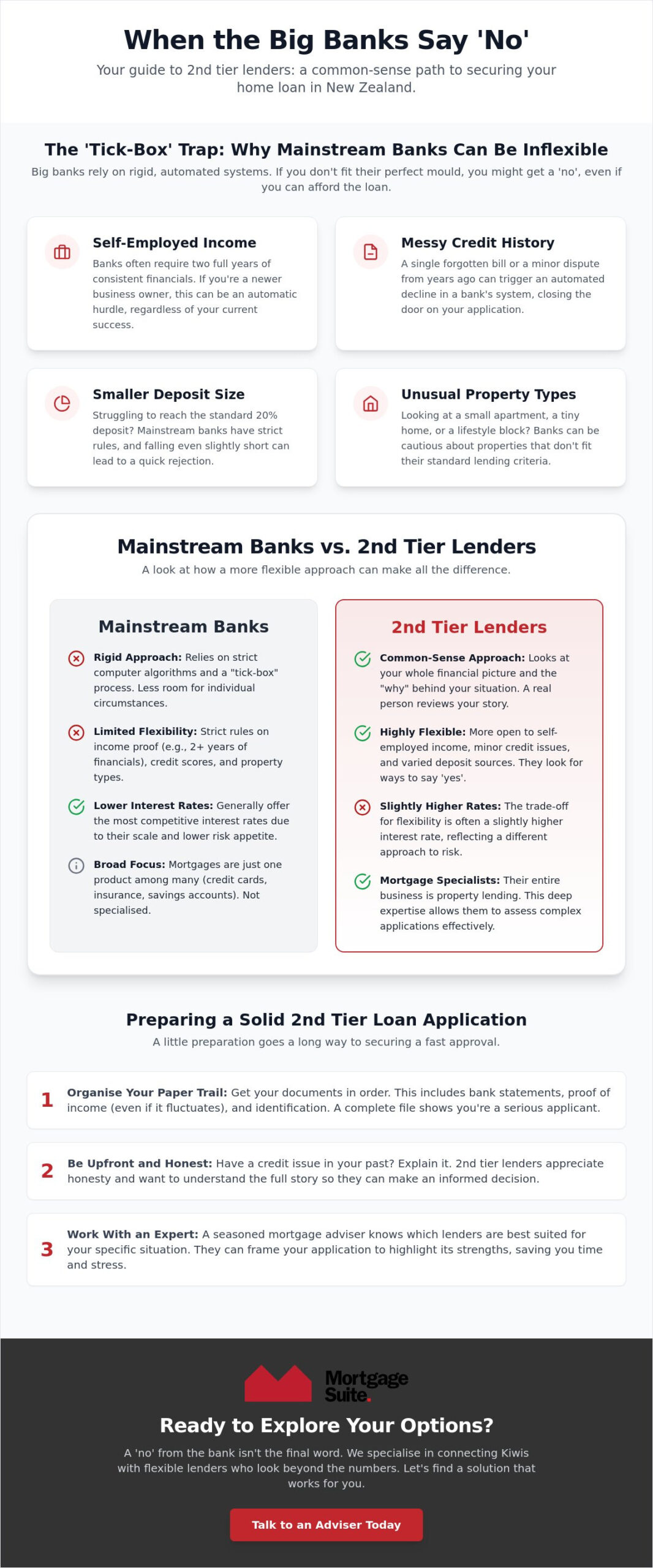

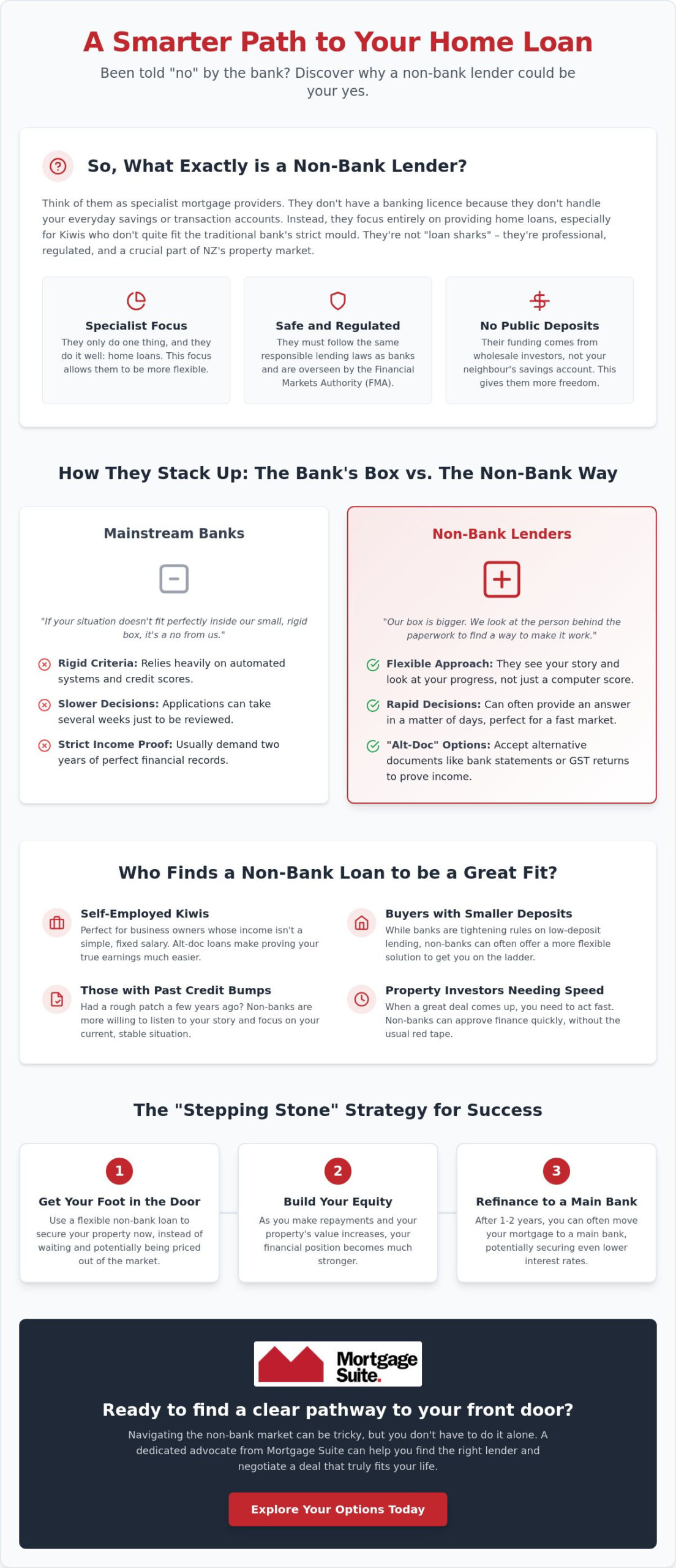

Finding the Right Mortgage: Bank vs. Non-Bank Options

Most of us feel a sense of loyalty to the bank where we opened our first savings account as a kid. It’s a common trap. When you’re focused on buying a house on a single income nz, that loyalty isn’t always returned. Mainstream banks are massive institutions with rigid rules. They use computer models to decide if you’re a safe bet, and these models are often skewed toward dual-income couples. If your situation doesn’t fit their perfect little box, the computer simply says no. This is why looking beyond the “Big Four” is often the smartest move a solo buyer can make.

Alternative lenders, often called non-banks, operate differently. They don’t just look at a spreadsheet; they look at the person behind the application. While a mainstream bank might see your single salary as a risk, a non-bank lender often sees a disciplined professional with a clear financial history. They are willing to be more flexible because they aren’t bound by the same internal red tape as the major banks. You might find that while their interest rates are slightly different, the “yes” they provide is the key that finally opens your front door.

When the Big Banks Say No

It’s incredibly disheartening to be declined by your own bank. Usually, they’ll cite those strict rules about debt balances we talked about earlier, or they might be worried about your ability to pay back the loan on a single cheque. Don’t let one rejection stop you. A “no” from a big bank is often just an invitation to find a more innovative partner. This is where a 2nd tier lender New Zealand becomes your greatest asset. These lenders specialise in situations that mainstream banks find too “complex,” providing a vital lifeline for solo buyers who have a solid deposit but don’t meet the standard bank criteria.

The Flexibility of Non-Bank Lenders

Non-bank lenders are particularly helpful if you’re self-employed or have a non-standard income like commissions or bonuses. They are more likely to recognise the true value of your earnings. They also offer more wiggle room for buyers with a smaller deposit, which is a frequent hurdle when buying a house on a single income nz. You can find independent advice on how these different lending structures work at Settled.govt.nz. Remember, a 2nd tier loan doesn’t have to be forever. Many of our clients use these loans as a stepping stone, getting into their home now and then moving back to a mainstream bank once they’ve built up more equity in a few years.

Your 5-Step Roadmap to Solo Home Ownership

If you’re serious about buying a house on a single income nz, you need a plan that doesn’t rely on luck. It’s easy to feel overwhelmed by the process, but breaking it down into manageable steps turns a massive goal into a series of small wins. You aren’t just looking for a house; you’re building a foundation for your future, and that requires a methodical approach that big banks will respect. Here is the path we recommend for our solo clients to ensure they stay on track and avoid common pitfalls.

- Step 1: Get a clear picture of your financial health. Beyond just your bank balance, look at your “surplus” income. Lenders want to see exactly what’s left over after your life is paid for each week.

- Step 2: Maximise your deposit. This involves consolidating your savings and ensuring your KiwiSaver is ready for withdrawal. Every extra thousand dollars in your deposit reduces the risk the bank perceives.

- Step 3: Organise a pre-approval. Knowing your true budget before you start visiting open homes is a superpower. It stops you from falling in love with a property you can’t actually afford.

- Step 4: Target properties that fit your solo lifestyle. Focus on homes that offer low maintenance and high security, which are often easier for a single person to manage and insure.

- Step 5: Work with a broker to negotiate. A broker acts as your advocate, presenting your case to lenders in the best possible light and finding terms that a standard bank manager might overlook.

Getting Your Paperwork in Order

Lenders are going to look at your life through a magnifying glass. As a single applicant, you’ll need to provide at least three to six months of “clean” bank statements. This means avoiding excessive Buy Now Pay Later transactions or large, unexplained cash withdrawals. You’ll also need your latest payslips and a letter from your employer confirming your permanent status. Proving your “serviceability” is about showing that your income is stable and that you’re a disciplined manager of your own money. If you can show a consistent history of living within your means, you’re halfway to a “yes.”

Shopping for the Right Property

When you’re the sole decision-maker, “buying for now” is a brilliant strategy. You don’t necessarily need a four-bedroom family home right away. Modern townhouses or well-located apartments are often more affordable and require far less weekend maintenance. This gets your foot in the door of the property market sooner, allowing you to build equity while living in a space that actually suits your current life. Always prioritise a professional building report. Since you won’t have a partner to help spot potential issues, having an expert’s eyes on the property’s structure is essential for protecting your investment. If you’re ready to see what’s possible for your specific budget, getting professional home loan advice is the best next step you can take.

Why a Mortgage Broker is a Solo Buyer’s Best Friend

Buying a home on your own is a massive milestone, but it’s often a lonely road. When you don’t have a partner to share the paperwork or the stress, a mortgage broker becomes your most valuable ally. For those buying a house on a single income nz, we act as the bridge between your personal goals and the rigid requirements of the banking system. We aren’t just looking for a loan; we are looking for the right fit for your specific life. Finding a path to buying a house on a single income nz is much easier when you have a seasoned negotiator fighting your corner.

Our approach at Mortgage Suite is built on over twenty years of direct banking experience. We’ve seen the industry from both sides of the desk, which gives us a unique perspective on how to get results. This background means we know exactly how to present your story to a lender to get a “yes.” We also have access to “wholesale” products and non-public loan options that aren’t available to the general public. This gives you a significant advantage in a competitive market where every detail counts.

Expert Negotiation for Unique Situations

We specialise in “packaging” applications to highlight your financial discipline. If a big bank sees a single income as a risk, we show them a borrower with total control over their budget. We handle the negotiation and the fine print, removing the obstacles that usually slow people down. Most importantly, our service is typically free for you; the lender pays us for the work we do in setting up the loan. This means you get professional advocacy without adding another cost to your house-hunting budget.

Long-Term Support Beyond the Settlement

Getting the keys is just the beginning of your journey. We stay in your corner to help you manage your debt and review your mortgage rates NZ whenever the market changes. Whether it’s planning for future renovations or using your growing equity to build wealth, we’re here for the long haul. We aim to be your partner in property for the next twenty years, providing the steady hand you need in an ever-changing market. You don’t have to do this alone when you have an expert mentor by your side.

Your Future Home is Within Reach

The dream of owning your own place doesn’t have to wait for a partner or a second salary. By focusing on your uncommitted income, exploring flexible non-bank lenders, and following a disciplined roadmap, the path to ownership becomes clear. It’s about looking past the standard bank rejection and finding a partner that values your individual financial strength and stability over a rigid checklist.

Successfully buying a house on a single income nz requires more than just a good deposit; it needs a dedicated advocate who knows how the system works from the inside. With over 20 years of banking expertise, we are specialists in 2nd tier lending solutions that help you move forward when the big banks aren’t an option. Talk to Krish and the team at Mortgage Suite today to start your solo home journey. We are here to act as your mentor and negotiator, ensuring you have the expert support needed to finally secure your own front door keys. You already have the drive and the financial control; now let’s work together to get you the home you deserve.

Frequently Asked Questions

How much deposit do I need to buy a house on a single income in NZ?

You generally need a 20% deposit for most standard bank loans, but you can secure a home with as little as 5% through the First Home Loan scheme. This is a massive help for anyone buying a house on a single income nz because saving $154,000 alone, which is 20% of the $770,000 national median price, is a huge mountain to climb. Low-deposit options make the dream much more accessible for solo buyers.

Can I use my KiwiSaver if I am buying a house by myself?

Yes, you can withdraw your KiwiSaver savings to put toward your first home as long as you’ve been a member for at least three years. You’ll need to leave at least $1,000 in your account; however, the rest of your contributions, employer contributions, and government top-ups can all go toward your deposit. It’s often the biggest financial boost a solo buyer has when starting out.

What is the First Home Grant and am I eligible as a single person?

The First Home Grant was officially discontinued on 22 May 2024, so it is no longer available for new applications. Instead, you should focus on the First Home Loan scheme, which remains active in 2026. This scheme helps solo buyers with an income of $95,000 or less get into the market with a 5% deposit, provided they meet the standard lending criteria.

Will a bank decline my mortgage if I have a student loan?

A student loan won’t automatically lead to a decline, but it does reduce your “take-home” pay, which banks use to calculate how much you can afford. Because a portion of your salary goes toward repayments, the lender will see you have less uncommitted income to put toward a mortgage each month. It’s just one factor they’ll consider when looking at your overall debt-to-income ratio.

Is it better to buy a new build or an existing home on a single income?

New builds are often easier for solo buyers because they are exempt from standard LVR restrictions, meaning you might only need a 5% or 10% deposit. Banks are often more willing to lend higher amounts for new properties. Existing homes usually require a larger upfront deposit, but they might offer a lower purchase price depending on the location and the condition of the property.

How do lenders calculate how much I can borrow on one salary?

Lenders look at your gross annual income and then subtract your fixed costs, like student loans, car payments, and living expenses. They use a “test rate” higher than the actual interest rate to make sure you can still pay if rates go up. This is why buying a house on a single income nz requires such a clean budget; every dollar of your salary needs to be accounted for.

What happens if I lose my job and I have a solo mortgage?

If you lose your job, the first step is to talk to your lender immediately to discuss hardship options or a temporary change to your payment schedule. Having a solid emergency fund is vital for solo owners, as you don’t have a second salary to fall back on. Banks are usually willing to work with you if you’re proactive and honest about your situation.

Can a family member help me with my deposit (gifted deposit)?

Yes, family members can certainly help by providing a gifted deposit to boost your equity. Most lenders will require a signed “gift letter” stating that the money doesn’t need to be paid back and that the family member has no claim on the property. This is a very common way for solo buyers to bridge the gap and reach that 20% equity mark sooner.