What if your local bank manager’s “no” was actually the best thing that ever happened to your business dreams? Most Kiwis think the big four banks are the only game in town when they’re looking for a business loan for franchise purchase nz, but that’s often where the stress starts. It’s completely normal to feel a bit stuck when you’re trying to figure out how much deposit you really need or how to handle a complex franchise agreement that feels like it’s written in another language.

We know that you’re more than just a credit score on a screen; you’re someone ready to work hard for your future. This guide will show you how to secure the right finance to buy your dream franchise here in New Zealand, even if the mainstream banks have already turned you away. We’ll walk you through the world of 2nd tier lending, explain how to find better interest rates, and show you a clear path to getting the paperwork sorted. By the time you’ve finished reading, you’ll have the confidence to stop worrying about the “what ifs” and start focusing on opening your new doors.

Key Takeaways

- Learn why lenders view franchises differently and how this unique perspective impacts your chance of getting an approval.

- Find out how to secure a business loan for franchise purchase nz by looking beyond mainstream banks to more flexible 2nd tier lending options.

- Understand the “two-fold” assessment process where banks evaluate both your personal financial history and the reputation of the franchise system.

- Identify the essential items for your “Franchise Ready” checklist, from aligning your loan term with your agreement to creating a solid business plan.

- Discover how expert help can simplify the complex paperwork and give you a clear path to getting your new business up and running.

Buying a franchise in New Zealand: Why the right loan makes the difference

In 2026, many Kiwis are looking for more security and control over their working lives. Stepping into a business with a proven track record is a great way to do that, which is why the appeal of franchising remains so strong across New Zealand. However, the excitement of choosing the right brand can quickly turn to stress when you start looking for a business loan for franchise purchase nz. It’s not just about getting a “yes” from a lender; it’s about making sure the money you borrow is set up in a way that actually works for your specific situation.

A franchise loan is quite different from a standard small business loan. With a brand-new startup, a lender only has your personal history and a set of projections to look at. With a franchise, they can look at the history of the entire brand. This extra layer of data can be your biggest asset if you know how to use it. At Mortgage Suite Ltd, we view your business dream as a partnership. We want to make sure the finance structure you choose provides peace of mind, especially when it comes to protecting your family home from unnecessary risk.

The benefits of a proven system

Lenders are naturally cautious. When you present an application for a brand that already has dozens of successful locations across the country, you are speaking their language. You might be asking, what is franchising in the eyes of a bank? Essentially, it’s a way to share the risk. The franchisor provides the training, the marketing, and the operational support that acts as a safety net for your loan. Because the brand has a vested interest in your success, banks often feel more comfortable lending larger amounts or offering better terms than they would for a completely independent business.

Why you need a specialised strategy

The danger many new owners face is trying to use “off-the-shelf” bank products that don’t quite fit. A standard loan might not account for the specific costs of a franchise fit-out or the ongoing fees required by the head office. If you choose the wrong type of debt, you could find yourself struggling with cash flow in those critical first six months. Some people choose to use the equity in their existing homes to get things started. If you’re thinking about using your property as leverage, our guide on residential investment property loans NZ explains how to manage those assets wisely while you grow your business. Having a specialised plan ensures you aren’t just getting a business loan for franchise purchase nz, but a foundation for long-term growth.

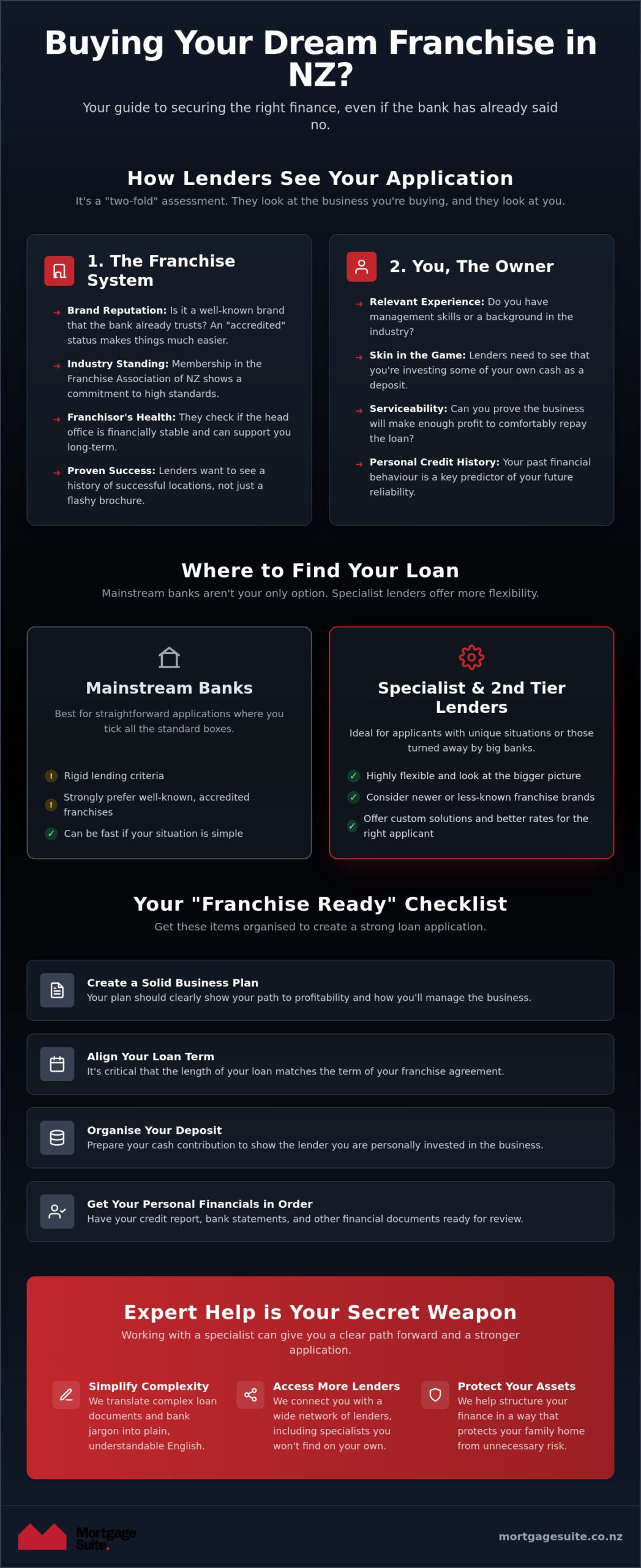

How lenders evaluate your franchise loan application

When you apply for a business loan for franchise purchase nz, the lender performs what we call a “two-fold” assessment. They aren’t just looking at your bank statements; they’re looking at the brand you’re joining. It’s a bit like a job interview where the company you’re going to work for also gets interviewed. The bank wants to be certain that you’re the right person to run the ship and that the ship itself is seaworthy.

Assessing the Franchise System

Lenders love brands they already know and trust. If a franchise is “accredited” with a bank, it means the bank has already vetted the business model, which can make your approval process much faster. They often look for brands that are members of the Franchise Association of New Zealand, as this shows a commitment to industry standards and best practices. For newer brands that haven’t been in the country long, the bank will dig deeper into the franchisor’s financial health to ensure they have the resources to support you over the long haul. They want to see a history of success, not just a flashy marketing brochure.

Assessing you as the owner

You are the engine of the business, and the lender needs to know you can handle the daily grind. They look for management experience or industry-specific skills that prove you can lead a team and manage a budget. They also look for “skin in the game,” which means you’ll need to put in some of your own cash as a deposit. A crucial part of this is serviceability, which is your ability to pay back the loan from business profits. Even though you’re starting a business, your personal credit history still carries weight. Lenders use your past behaviour with personal debt to predict how you’ll handle a business loan for franchise purchase nz.

One detail people often miss is the timeline of the loan. Your loan term usually cannot be longer than the length of your franchise agreement. If you have a five-year agreement with the brand, the bank won’t typically give you a ten-year loan. You’ll also need to decide between secured lending, where you use an asset like your home as a guarantee, and unsecured lending. While unsecured options don’t require your house as backup, they usually come with higher interest rates because the lender is taking on more risk. If you’re feeling a bit overwhelmed by these requirements, talking to a specialist can help you see which “box” you currently fit into and how to build a stronger case for your approval.

Comparing your options: Mainstream banks vs 2nd tier lenders

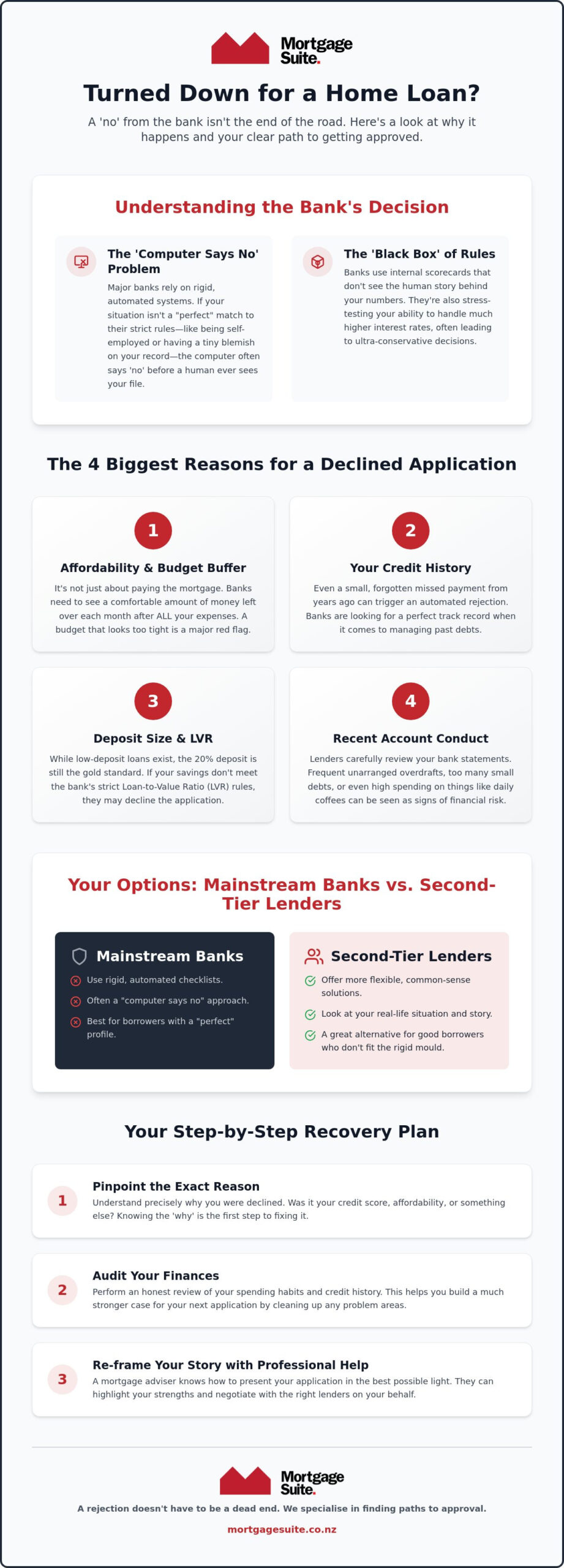

Most people’s first instinct when looking for a business loan for franchise purchase nz is to walk into the bank where they’ve had their mortgage for years. It makes sense, as you already have a relationship there. However, in 2026, big banks have become even more rigid with their checklists. If you don’t fit their exact “box,” the computer often just says no. This doesn’t mean your business idea is flawed; it just means it doesn’t fit that specific bank’s appetite for risk at this moment. Being declined by a major bank isn’t the end of the road, but it is a sign that you need a more flexible strategy.

When the big banks are a good fit

Traditional banks are excellent if you have a perfect credit history and plenty of equity in your home. They offer some of the lowest interest rates on the market for commercial mortgages. But there’s a trade-off. They almost always require 100% security against property, which means your family home is directly on the line. They’re also notoriously slow. When you’re becoming a franchisee in New Zealand, timing is often everything. Waiting six weeks for a bank to even look at your application can mean losing out on a prime location or a great existing territory.

The 2nd tier advantage for franchises

This is where alternative lenders come in. A 2nd tier lender is often more interested in what your business will do tomorrow than what it did two years ago. While a big bank might obsess over past tax returns, a 2nd tier lender looks at future cash flow and the strength of the franchise system. This is a massive advantage if you’re buying an existing franchise where the previous owner kept messy books or didn’t run the business to its full potential.

These lenders are more flexible with security too. They might accept the business assets themselves or a smaller deposit. If you want to understand more about how these options work for your personal situation, check out our guide on finding a 2nd tier lender New Zealand. At Mortgage Suite Ltd, we spend our days working across both of these worlds. We know which banks are currently open for business in specific industries and which alternative lenders offer the best terms for your specific business loan for franchise purchase nz. We handle the negotiation so you don’t have to face the “no” alone.

Your “Franchise Ready” checklist: What you need to organise

Walking into a meeting with a lender can feel like a high-stakes interview. Having your paperwork in order doesn’t just show you’re serious; it shows you’re ready to lead. The most important document in your pile will always be the Franchise Agreement. This isn’t just a contract between you and the brand; it’s the blueprint for how you’ll make money. Lenders will scrutinise this to see what you’re allowed to do and, more importantly, how long you’re allowed to do it. If the agreement is only for five years, don’t expect the bank to give you a seven-year loan.

You’ll also need a business plan that actually makes sense to a person who looks at numbers all day. Don’t just copy the franchisor’s template. You need to show you understand your local market and the specific “ramp-up” period where you might be spending more than you’re making. Realistic cash flow forecasts are vital. If you’re too optimistic, a seasoned lender will see right through it. They want to see that you’ve planned for those quiet first few months when you’re still building your customer base. This preparation is the key to securing a business loan for franchise purchase nz without the usual back-and-forth stress.

Financial documentation

If you’re buying an existing franchise, you’ll need at least two or three years of its actual financial history. Be careful with “pro-forma” accounts, which are basically “what if” scenarios provided by the seller. Lenders want to see the hard numbers of past performance, not just the potential. You’ll also need to prepare a Statement of Assets and Liabilities. This shows the lender your total personal position, including what you own and what you owe elsewhere. Many Kiwis don’t realise that their home equity is often the key to their business dream. If you’re moving funds around to make the numbers work, our guide on commercial property refinance NZ can show you how to unlock equity and find better rates for your deposit.

Operational details

Lenders want to see that the business has a solid foundation. They’ll ask for the lease agreement for your premises to ensure you have a secure location for the duration of your business loan for franchise purchase nz. It’s also a great idea to include your franchisor’s training certificate in your application. It proves to the bank that you’ve been professionally prepared to run the brand according to their proven system. If you’re feeling unsure about whether your documents are up to scratch, get in touch for a chat so we can review your position and help you present the strongest possible case.

Why working with Mortgage Suite Ltd is your secret weapon

You have the dream, the brand, and the checklist. Now you need someone who knows how to move the mountains of paperwork. Krish Krishna brings over 20 years of banking experience to your corner, which means we speak the language lenders use. We don’t just fill out forms; we understand the internal logic banks use to say yes or no. This deep institutional knowledge allows us to handle the heavy lifting of your application, leaving you free to focus on the exciting part: preparing to open your new business. When you are looking for a business loan for franchise purchase nz, having that level of experience on your side is the difference between a stressful “maybe” and a confident “yes.”

We also give you access to a wide range of lenders that you simply won’t find on the local high street. While your personal bank only has one set of rules, Mortgage Suite Ltd works with a vast network of 2nd tier lenders who offer the flexibility that franchises often need. This is especially helpful if your situation is a bit unique or if the big banks have already turned you down. Our service is personalised and continues long after the loan is settled. We stay in your corner as your business grows, ensuring your finance structure remains fit for purpose as the market changes.

The power of expert negotiation

A lot of automated lending apps promise fast funds, but they lack the human touch required for complex franchise deals. We “package” your application to highlight your strengths as an owner and address any potential weaknesses before the lender even sees them. It is about presenting your story in a way that makes sense to a credit manager. We also take on the task of negotiating interest rates and fee waivers on your behalf. Having a broker is like having a veteran mentor who has seen every possible scenario and knows exactly which levers to pull to get you a better deal on your business loan for franchise purchase nz.

A national service with local heart

Distance is never a barrier. Mortgage Suite Ltd helps Kiwis across the country buy into franchises, providing national coverage with a focus on personal connection. You won’t find any cold, corporate jargon here; we prefer straight talk about your money and your goals. Our process is designed to be inclusive and easy to follow, regardless of your financial background. If you are ready to take the next step, it starts with a free, no-obligation chat. We will look at your position, listen to your business goals, and give you an honest assessment of your funding options without any pressure.

Ready to open your new doors?

Buying a franchise is one of the biggest steps you’ll ever take. While the paperwork can feel heavy, the funding side doesn’t have to be a source of constant stress. We’ve seen that securing the right business loan for franchise purchase nz comes down to solid preparation and knowing which lender’s “box” you fit into. Whether it’s a traditional bank or a flexible 2nd tier option, there’s a path forward even if you’ve been turned away before. You now have the strategy to move from browsing to buying with confidence.

With over 20 years of banking experience, we are dedicated to helping Kiwis succeed by providing access to a wide range of mainstream and alternative lenders. We handle the hard negotiations so you can focus on your new business. If you’re ready to get your application moving, talk to Krish and the team about your franchise funding today. Your dream business is within reach, and we’re here to help you cross the finish line.

Frequently Asked Questions

Can I get a franchise loan with no experience in that industry?

Yes, you can certainly get funding without direct experience in that specific field. Lenders value transferable skills like staff management, budgeting, and customer service. They also feel more comfortable knowing the franchisor provides a full training program to get you up to speed before you open your doors.

How much deposit do I need to buy a franchise in NZ?

Most lenders in New Zealand look for a deposit of at least 30% to 50% of the total purchase price. If you’re buying into a well-known, accredited brand, some banks might be willing to lend a higher percentage because they trust the system’s track record of success. Your personal financial position will also play a big part in this decision.

Is it better to use my home equity or a business loan for a franchise?

It depends on how you want to manage your risk and your interest costs. Using home equity usually gives you access to lower interest rates, but a dedicated business loan for franchise purchase nz keeps your business debt separate from your family home. Many people choose a mix of both to balance the cost and their personal security.

What happens if my franchise loan application is declined by my bank?

If your local bank says no, don’t panic. Mainstream banks have very strict rules, but 2nd tier lenders often have more flexible criteria. We can help you re-package your application to highlight your strengths or find a lender who specialises in your specific industry and understands the potential of your chosen franchise.

How long does the approval process for a franchise loan usually take?

You should generally allow two to four weeks for a full approval. If the franchise brand is already accredited with the bank, the process can be much faster. However, if the lender needs to review a complex new agreement or request more financial history, it can take a bit longer to get everything across the line.

Do I need to provide a business plan for a franchise purchase?

Yes, every lender will require a detailed business plan. While the franchisor will provide you with a template and some data, you need to customise it to show you understand your local area. It must include realistic cash flow forecasts that show how you’ll manage the business during the initial start-up phase.

Can I get a loan to buy an existing franchise that is already trading?

Yes, and lenders often prefer this because there is a history of actual profits to review. You’ll need to provide at least two or three years of tax records and financial statements for that specific location. This data gives the bank more confidence that the business can easily cover the loan repayments.

What are the typical interest rates for franchise loans in NZ in 2026?

Lenders typically don’t publish a single fixed rate because every business is different. In July 2026, we’ve seen base rates around 6.04% p.a. from some major banks, though your actual business loan for franchise purchase nz rate will include a margin based on your risk profile. Rates for 2nd tier lenders are usually higher but offer much more flexibility.