What if the “standard” 20% deposit isn’t actually the only way to secure your first home in the city? When you are looking at buying an apartment deposit nz rules can often feel like they are written in a different language, especially when banks start talking about floor sizes and leasehold titles. It is a common frustration to feel like the goalposts keep moving just as you get close to your savings target. You might even worry that because apartments are viewed differently than houses, you are stuck in the rental cycle forever.

We understand that the path to ownership should be clear, not confusing. That is why we have put together this guide to show you exactly how much you need to save in 2026 and the clever strategies we use to help clients get their foot in the door, even with a smaller stash. We will break down the specific deposit percentages required for different property types, explain the “size trap” that catches many buyers out, and outline a clear plan to get you mortgage-ready. You will discover which government grants actually apply to apartments and how to avoid the common pitfalls that trip up even the most diligent savers.

Key Takeaways

- Learn why the floor area of your apartment is just as important as your savings and how the 40 to 50 square metre mark affects your bank’s decision.

- Discover the specific government grants and schemes that can help you secure your home with as little as a 5% or 10% deposit.

- Understand the unique criteria for buying an apartment deposit nz and why banks view these properties differently than a standard house.

- Find out how to work with non-bank lenders if you have fallen in love with a “quirky” or smaller property that doesn’t fit the usual rules.

- Get a clear, step-by-step plan for 2026 to ensure your Body Corporate and building checks are sorted before you sign any contracts.

Buying an Apartment? Why Your NZ Deposit Might Be Different to a House

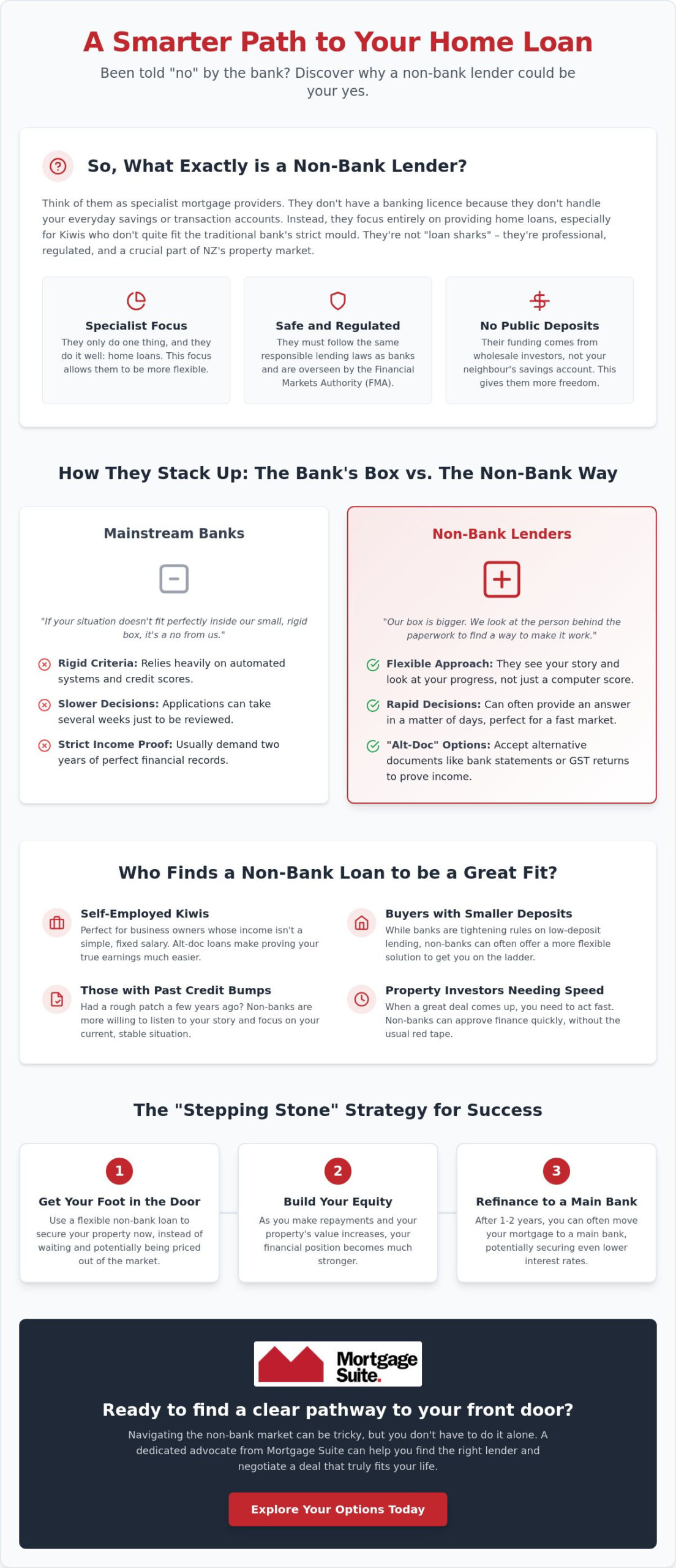

You might have heard that you need a massive pile of cash to buy property, but when you’re looking at buying an apartment deposit nz requirements aren’t always a one-size-fits-all deal. Many people think the 20% rule is a strict law. It isn’t. It is more of a benchmark that banks use to decide how much they’re willing to lend. In the current 2026 market, with a significant increase in apartment supply and stabilising rents, banks are looking at these properties with a fresh pair of eyes. However, they still treat them differently than a standard house on a quarter-acre block.

The main reason for this difference is risk. A bank sees a standalone house as a safe bet because the land usually holds its value over time. With an apartment, you’re buying into a shared building. This means the bank has to consider things like the health of the building’s structure and how well the complex is managed. It is a trade-off. You might get a much lower purchase price than a house, but you might need a higher percentage of that price upfront to satisfy the lender’s nerves.

The Standard Bank Perspective

Banks love it when you have a decent amount of your own money in the deal. They look at the size of the loan compared to what the property is worth to measure their risk. If you buy a $500,000 apartment with a $100,000 deposit, your loan is 80% of the value. This is the “sweet spot” where you get the best interest rates. If you have less than 20%, you aren’t necessarily out of the race. You might just have to pay a small extra fee to cover the bank’s risk. In New Zealand’s housing market, the Reserve Bank currently allows a certain percentage of bank lending to go to people with smaller deposits, so there is definitely room to move if your income is steady.

Apartment vs House: The Deposit Divergence

Why does a bank care if you’re buying a studio in the city or a house in the suburbs? It often comes down to how easy it is to sell the place later. If things go wrong and you can’t pay the mortgage, the bank wants to know they can sell the property quickly to get their money back. High-density living can be more volatile in terms of price. They also look closely at your “borrowing power” after you’ve paid your building management fees. These annual costs cover insurance and maintenance, but they also eat into your weekly budget. A bank will factor these costs into your application, which is why buying an apartment deposit nz can sometimes feel like a more complex puzzle than buying a traditional house.

Ultimately, 2026 is a unique time to buy. With more choice on the market, you have more leverage as a buyer, provided you understand these banking quirks before you start your search.

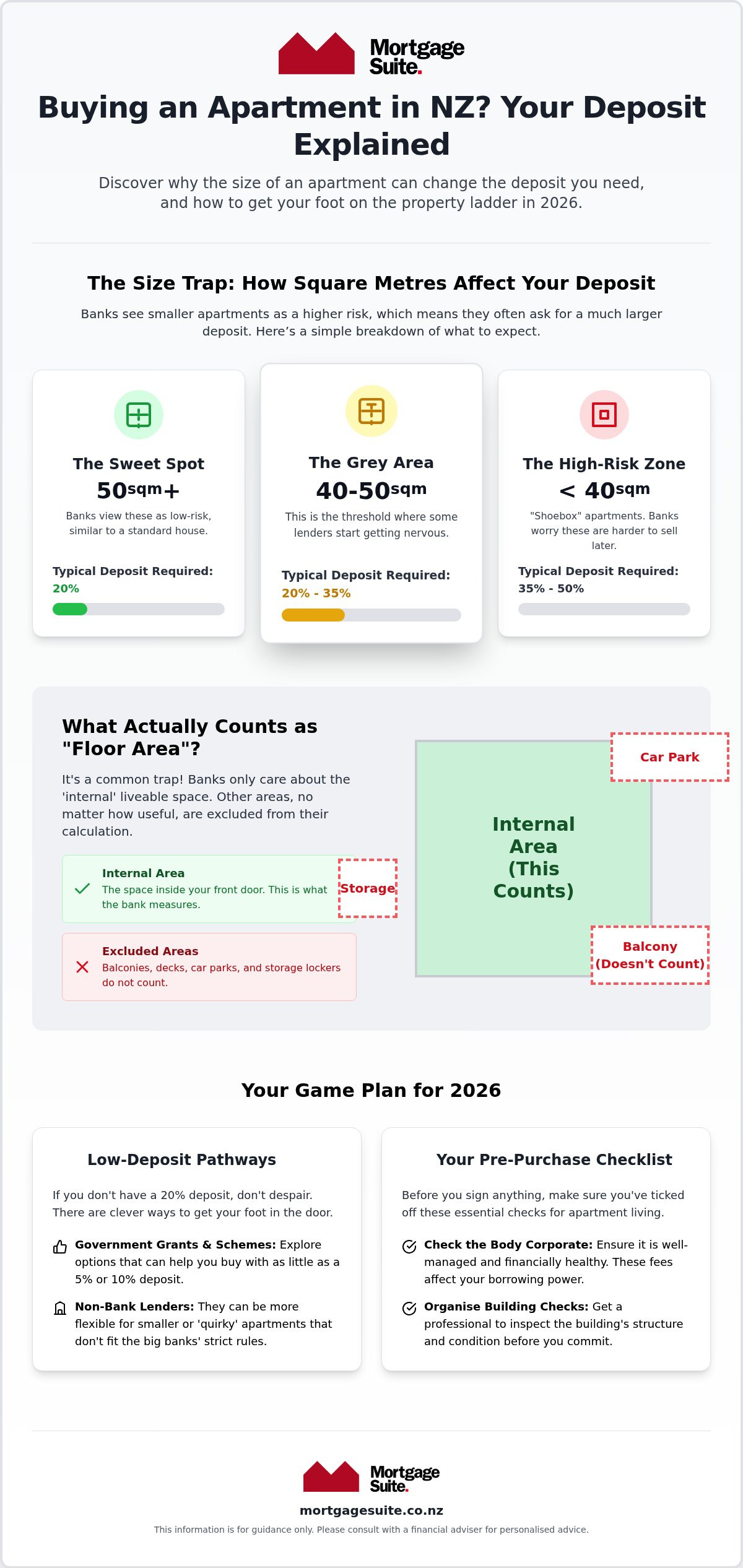

The Size Trap: How Square Metres Change Your Deposit Requirements

Size matters in the apartment world. You might find a sleek studio in the city centre that fits your budget perfectly, but your bank might see things differently. Most lenders have a specific set of criteria they use to judge whether a property is “liveable” or “bankable”. The Small Apartment Rule used by most NZ banks dictates that any unit with an internal floor area below a specific threshold, usually 40 to 50 square metres, is classified as a high-risk security and requires a much larger deposit.

When you are looking at buying an apartment deposit nz lenders will look at the “internal area” of the property. This is a crucial distinction. Your internal area includes the space inside your front door, but it strictly excludes your balcony, any storage lockers, and your car park. If your apartment is 42 square metres inside but has a massive 15 square metre deck, the bank still treats it as a 42 square metre property. If that number falls below their magic threshold, your required deposit could suddenly jump from 20% to as much as 50%.

The Studio Struggle

Banks are often nervous about tiny homes and “shoebox” apartments because they view them as a niche market. They worry that if the market takes a dip, these smaller units will be the hardest to sell. For properties under 40 square metres, expect the bank to ask for a deposit of at least 35%. In some cases, they might even demand 50% upfront. There are exceptions, of course. If a small apartment is in a premium building with high demand or if it’s a new build with a high-spec finish, some lenders might be more flexible. If you are struggling to get a traditional bank to look at a smaller unit, it helps to talk to a specialist about 2nd tier loans that are designed for these non-standard properties.

Freehold vs Leasehold: The Title Trouble

What you actually own can be just as important as the size of the rooms. Most New Zealand apartments are “Unit Titles”, which are a form of freehold ownership. You own your unit and a share of the common areas. However, leasehold apartments are a different story. In a leasehold arrangement, you own the building but not the land it sits on. You have to pay “ground rent” to the landowner, which can increase significantly every few years. Because of this ongoing cost and the risk of the land lease expiring, lenders often require a much larger deposit, sometimes 30% to 50%, to protect themselves from the potential drop in the property’s value.

Low-Deposit Options: Getting Your Foot in the Door with 5% or 10%

Saving a full 20% can feel like an impossible mountain to climb, especially when property prices are on the move. The good news is that you don’t always have to reach that peak before you start looking at properties. For many people buying an apartment deposit nz, the solution lies in a mix of personal savings, government help, and clever lending structures. While big banks might lead with their strictest rules, there are several pathways that let you start your ownership journey with much less cash upfront.

One of the most common ways to bridge the gap is by looking at new builds. Buying “off the plans” often comes with a significant advantage because these properties are frequently exempt from standard lending restrictions. This means many banks are happy to accept a 10% deposit for a brand-new apartment. If you’re still coming up short, a “Family Springboard” might be an option. This isn’t about your parents giving you a suitcase of cash; instead, they use the equity in their own home to guarantee a portion of your loan. It is a powerful way to get into the market years earlier than you otherwise could.

KiwiSaver Mechanics for Apartments

Your KiwiSaver is often the biggest piece of the puzzle. You can generally withdraw almost all your funds, including your employer contributions and investment returns, provided you’ve been a member for at least three years. In 2026, the First Home Grant remains a vital boost for those buying within specific price caps. Timing is everything here. You need to get your withdrawal paperwork started well before you attend an auction or sign a sale and purchase agreement. The funds need to be ready for the settlement date, and leaving it to the last minute can cause unnecessary stress during the final stages of the purchase.

The 5% Deposit Path

The First Home Loan scheme, backed by Kāinga Ora, is a genuine game-changer if you only have a 5% deposit. To qualify in 2026, your before-tax income over the last 12 months must be $95,000 or less for a single buyer, or $150,000 for a couple or single buyer with dependents. However, remember the “size trap” we mentioned earlier. For a First Home Loan, the apartment must usually be at least 45 square metres. Not every bank plays ball with this scheme, so it is crucial to work with a specialist who knows which lenders are currently participating and how to package your application for success. You can find more detail in our guide to Home Loans for First Home Buyers in New Zealand.

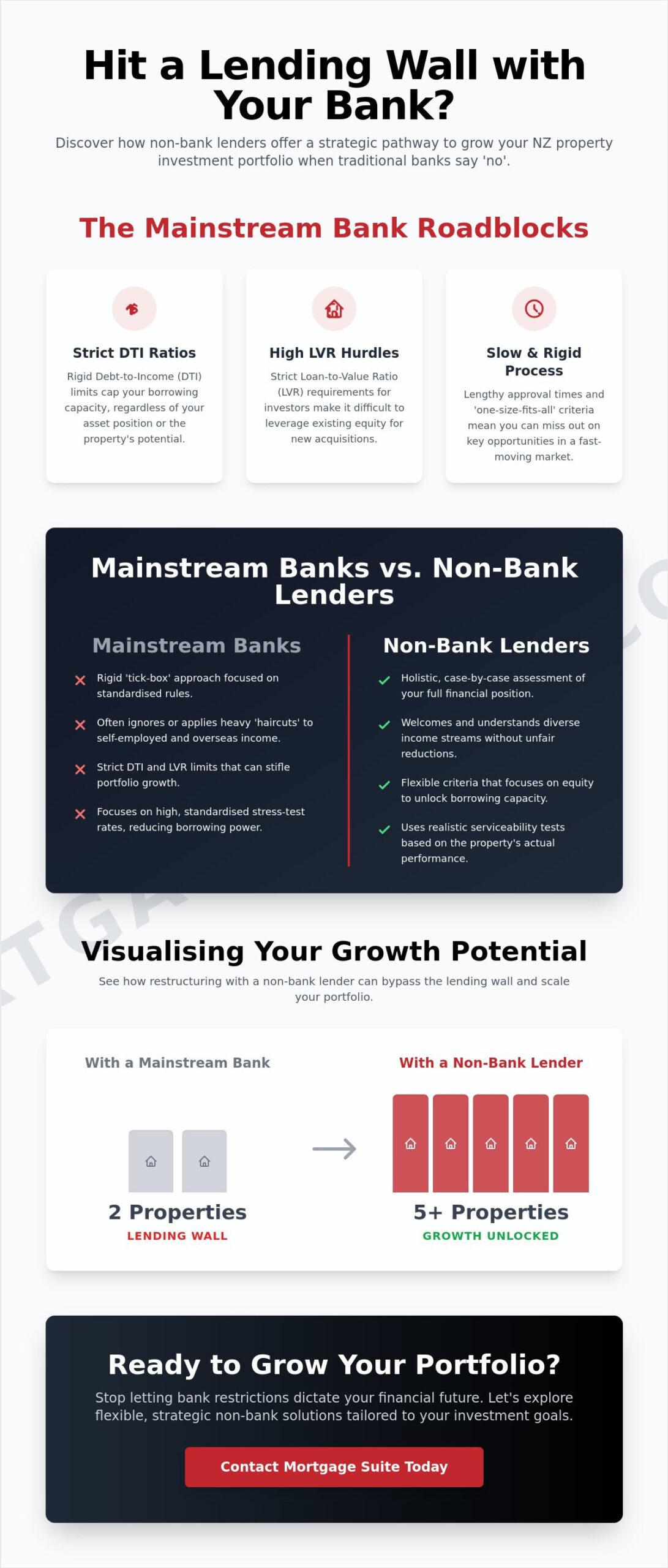

When the Bank Says No: Alternative Funding for Non-Standard Apartments

It is a gut-wrenching feeling when you find the perfect city pad, only for your bank to decline the loan because the place is a few square metres too small or the building is “too old”. This is where many buyers give up, thinking their dream of owning is over. But the truth is that mainstream banks have very narrow boxes they need you to fit into. If your property is considered one of those properties that don’t fit the standard rules, you simply need a different kind of lender who sees the value that the big banks miss.

Alternative lenders are the hidden engine of the New Zealand property market. They don’t have the same rigid rules as the big four banks. When you are looking at buying an apartment deposit nz, these lenders are often more interested in your ability to pay the mortgage than the exact dimensions of your balcony. Yes, there is a trade-off. You might pay a slightly higher interest rate initially, but many buyers use these loans as a stepping stone. Once you have built up some equity or the market shifts, you can often move your mortgage back to a mainstream bank at a lower rate.

The Alternative Lender Advantage

Alternative lenders often look at the person behind the application rather than just a checklist of property stats. If you have a solid career and a clear plan, they are far more likely to approve a loan for a studio or a quirky heritage conversion that a traditional bank would reject. These lenders provide a vital path for those who don’t fit the standard mould. You can learn more about how these flexible options work in our 2nd Tier Lender New Zealand guide.

Self-Employed or “Difficult” Income

Being self-employed while trying to buy an apartment can feel like a double-whammy. Big banks often demand years of perfect, predictable tax returns, which doesn’t always reflect the reality of running a successful business. When you combine that with a property that doesn’t fit the standard rules, the computer says “no” almost instantly. This is where having an advocate makes all the difference. Krish Krishna uses 20 years of banking experience to negotiate directly with lenders, proving your financial strength through other means. We know how to present your case so that lenders see your actual success, not just a spreadsheet.

If you’ve been told your dream apartment is “unbankable” by the big banks, don’t walk away just yet. Contact Mortgage Suite Ltd today to see which alternative funding options can help you secure your property in 2026.

Your Game Plan: Organising Your Deposit and Getting Sorted for 2026

Ready to stop scrolling through listings and actually start signing? You have already seen how property size and different types of lenders play a massive role in your journey. Now, it is time to put that knowledge into a practical plan for 2026. When you are buying an apartment deposit nz savings are only the first hurdle. You need a solid game plan to ensure you are “offer-ready” and protected from any hidden surprises that could trip up your application at the last minute.

At Mortgage Suite Ltd, we believe the final stretch should be the most exciting part of the process, not the most stressful. We take the lead on the mountains of paperwork, from coordinating with your solicitor to making sure your KiwiSaver funds are ready for settlement day. Our goal is to make the entire process feel like a helpful dialogue rather than a complex lecture, ensuring you understand every step before you commit your hard-earned savings.

The Pre-Approval Power Move

Before you fall in love with a city view, you need a pre-approval that actually fits your specific goal. It is a common trap to assume a standard house pre-approval works for an apartment. In reality, banks often approve you as a borrower but keep the property itself “subject to bank approval”. They will want to vet the specific building, its insurance status, and its maintenance history before they give the final nod. This is also the best time to look at our Mortgage Rates NZ guide to see how current interest levels will impact your weekly budget. Knowing these numbers early prevents you from overextending yourself.

Hidden Costs to Budget For

Your deposit isn’t the only cash you will need to have ready in your accounts. There are several “entry costs” that can catch you off guard if you haven’t planned for them. To ensure you don’t buy a “lemon”, you need to budget for the following essentials:

- Valuation fees: Because apartments carry unique risks, banks almost always require a professional valuer to check the property before they release the funds.

- Solicitor fees: Your lawyer will need to spend extra time checking the building management rules and disclosure statements to ensure the complex is financially healthy.

- Council property report: This essential check (often known as a LIM) tells you everything the local council knows about the building’s history and any past issues.

- Moving costs and levies: You will need cash for the move itself and often the first instalment of your building management fees upon settlement.

By organising these details early and working with a veteran broker, you ensure that you are making a secure investment in your future city lifestyle.

Take the First Step Toward Your City Lifestyle

Securing your own slice of the city is an achievable goal, even in a shifting market. Throughout this guide, we have explored how the 2026 landscape offers unique opportunities for those who understand the specific rules around property size, titles, and lending criteria. The process of buying an apartment deposit nz doesn’t have to be a source of stress when you have a clear plan and the right expertise to guide you through the “size traps” and banking hurdles we have discussed.

Krish Krishna offers over 20 years of banking experience, providing the seasoned professionalism needed to navigate both mainstream and alternative lending paths. As specialists in 2nd tier loans and non-standard properties, we offer a personalised service that focuses on your individual success rather than just a rigid set of criteria. Ready to get sorted? Chat with Krish at Mortgage Suite Ltd today for a no-obligation chat about your apartment goals. We are here to act as your advocate and steady hand, helping you move into your new home with total confidence.

Frequently Asked Questions

Can I buy an apartment with a 5% deposit in NZ?

Yes, you can buy an apartment with a 5% deposit through the Kāinga Ora First Home Loan scheme. To qualify in 2026, you must meet specific income caps and the apartment must usually be at least 45 square metres in size. Not every lender participates in this program, so it is important to check which banks are currently accepting these low-deposit applications for high-density properties.

What is the minimum size for an apartment to get a bank loan?

Most New Zealand banks prefer a minimum internal floor area of 40 to 50 square metres to approve a standard mortgage. If the unit is smaller than this, it is often classified as a “shoebox” or a small studio. While you can still get finance for smaller spaces, you will likely need a much larger deposit, often between 35% and 50% of the purchase price.

Can I use my KiwiSaver for an apartment deposit?

You can certainly use your KiwiSaver savings to help with buying an apartment deposit nz. As long as you have been a member for at least three years, you can typically withdraw your own contributions, your employer’s contributions, and any investment returns. You just need to leave a minimum of $1,000 in your account to keep the fund open for the future.

Why do banks ask for a bigger deposit on some apartments?

Banks ask for a larger deposit when they believe a property carries a higher risk for resale. This is common with very small studios, leasehold titles, or buildings that have a history of maintenance issues. By requiring 30% or 40% upfront, the lender protects themselves against potential price drops or a limited pool of buyers if they ever need to sell the property.

What are Body Corporate levies and do they affect my loan?

Body Corporate levies are annual fees that cover the building’s insurance, shared utilities, and long-term maintenance funds. These costs do affect your loan because banks subtract the levy amount from your disposable income when calculating your “borrowing power”. If the annual levies are particularly high, it could slightly reduce the total amount the bank is willing to lend you for your mortgage.

Is it harder to get a mortgage for a leasehold apartment?

It is generally more difficult to secure a mortgage for a leasehold apartment because you do not own the land beneath the building. Lenders are often wary of ground rent increases and the uncertainty of what happens when the land lease expires. Because of these factors, most mainstream banks will demand a significantly higher deposit and may impose stricter repayment terms on the loan.

Do I need a lawyer before I pay my deposit?

You should always have a lawyer review the sale and purchase agreement and the Body Corporate documents before you pay a deposit. Apartment contracts include specific disclosure statements that outline the building’s financial health and any planned repairs. A lawyer ensures you aren’t signing up for a property with hidden legal issues or a massive bill for upcoming building maintenance.

How long does it take to get an apartment loan approved?

You should allow between five and ten working days for an apartment loan to be fully approved. While your personal financial check happens quickly, the bank also needs time to review the building’s specific details and a professional valuation report. Because the bank is lending on a shared building rather than just land, the process involves a few extra steps compared to a standard house.