You’ve likely spent months scrolling through floor plans and dream kitchen designs, but the most important blueprint for your new home isn’t the one drawn by an architect; it’s the one drafted by your lender. Buying land and building a house nz can feel like a mountain of paperwork and hidden “gotchas,” especially when you start hearing about development contributions or complex loan drawdowns. It’s completely normal to feel a bit overwhelmed by the fear of costs spiralling out of control or the worry that a mainstream bank might turn you down just because your situation doesn’t fit their standard box.

We believe you deserve more than just a loan; you need the peace of mind that comes from having a seasoned expert in your corner. At Mortgage Suite Ltd, we specialise in helping you navigate the 2026 landscape, from managing the latest building levy changes to mastering the stage-by-stage payment process. This guide is designed to strip away the confusion and show you exactly how to secure your section and unlock the specialised construction finance required to finally get the keys to a place you call home.

Key Takeaways

- Get your finance pre-approved before you start looking at sections so you can bid with the confidence of knowing your true spending limit.

- Understand the unique stages of buying land and building a house nz, including how “progressive drawdowns” keep your build moving from the slab to the final sign-off.

- Identify potential hidden expenses like council development contributions early on to ensure your budget remains realistic and stress-free.

- Explore how second-tier lenders can provide a vital lifeline for your project if the mainstream banks aren’t willing to help.

- Learn how an expert broker acts as your personal negotiator to streamline the complex communication between you, your builder, and the bank.

Is Buying Land and Building a House in NZ Right for You?

Deciding between an existing property and a fresh start is the first major hurdle you’ll face. While an older home offers the convenience of moving in next month, buying land and building a house nz provides a blank canvas to create a space that actually works for your family. It’s a choice between the “what you see is what you get” reality of the current market and the long-term satisfaction of a home designed specifically for your lifestyle. In 2026, this decision carries even more weight as building standards continue to evolve, making new homes significantly more efficient than those built even a decade ago.

Buying a section means engaging with New Zealand’s land registration system, a process that ensures your ownership is legally secure and clearly documented. However, the physical reality of that dirt is what really matters for your wallet. The slope of the land, the soil type, and how easily you can connect to water and power will dictate your entire build budget. We often see people fall in love with a view, only to realise later that the cost of the foundations will eat up half their kitchen budget. It’s about balancing your vision with the practicalities of the site.

The Pros of Starting from Scratch

The most obvious benefit is customisation. You aren’t trying to fit your life into someone else’s old floor plan; you’re building for the way you live now. Beyond the layout, a new build in 2026 means your home will be warmer, drier, and healthier. Modern building codes require high-performance insulation and double glazing that older Kiwi homes simply can’t match. You’ll also enjoy much lower maintenance costs in those first ten years. Most builders provide a Master Build guarantee, giving you a steady hand to rely on if any structural issues arise, which offers a level of peace of mind you won’t get with a 1970s bungalow.

The Challenges to Keep in Mind

Building isn’t without its hurdles, and timeline uncertainty is the biggest one. Weather delays, council consent hold-ups, and material supply shifts can push your move-in date out by months. Financially, it’s also more complex than a standard mortgage. You’ll likely be managing interest on your land loan while also preparing for progressive payments as the house goes up. This is why we always insist on a healthy contingency fund. We recommend setting aside at least 10% to 15% of your total build cost to cover those unexpected “site works” or price adjustments that often pop up once the diggers start moving dirt. Being prepared for these shifts makes the process a lot less stressful.

The 5 Essential Steps to Buying Land and Starting Your Build

While many people start their journey by driving through new subdivisions on a Sunday afternoon, the real work begins much earlier. To succeed when buying land and building a house nz, you need a logical plan that protects your bank account and your sanity. Following a structured path ensures you don’t fall in love with a section you can’t afford or a design that a lender simply won’t back. It starts with your budget and ends with the first shovel in the ground.

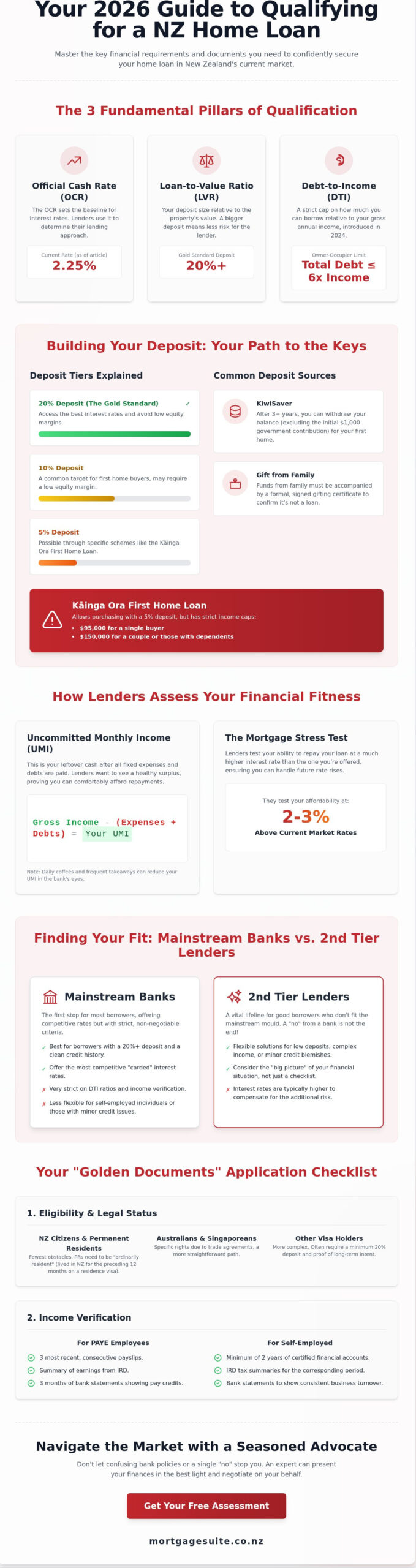

- Step 1: Get your finance sorted. Before looking at dirt, you must know your borrowing limit. Banks typically require a 20% deposit for urban land, but this can jump to 50% for rural blocks. Knowing these numbers early prevents heartbreak later.

- Step 2: Find the right section. Look beyond the view. Consider the sun’s path, the slope of the land, and how much “site work” will be needed before the slab can even be poured.

- Step 3: Perform due diligence. This is the investigation phase. You’ll need to check the title, the council files, and the physical state of the ground.

- Step 4: Select your partners. You need to find a qualified builder who understands your vision and, more importantly, your budget. A solid reputation is worth more than the lowest quote.

- Step 5: Finalise the loan. Once you have a fixed-price contract, your broker can secure the construction finance, allowing for the first drawdown to pay for the initial stages of work.

If the numbers feel a bit daunting, remember that you don’t have to crunch them alone. A quick chat to the team at Mortgage Suite Ltd to organise your pre-approval can clarify exactly where you stand before you sign any contracts.

Due Diligence: What to Check Before You Sign

In New Zealand, a Geotech report is a non-negotiable. Our varied landscape means one section might be solid rock while the neighbour’s is soft clay; this report tells your builder exactly how deep the foundations need to go. You should also examine the Land Title for easements, which are legal rights for others to use part of your land, or covenants that might restrict what colour you can paint your roof. Finally, check that services like water, power, and high-speed fibre are already at the boundary, as bringing these in from the street can cost a small fortune.

Choosing Your Build Method

You generally have two paths: a house and land package or a standalone build. Packages are often simpler because the developer has already handled the consents and basic design. However, if you’re building on your own bare land, you’ll likely need a fixed-price contract. Lenders in 2026 are very cautious about cost-plus arrangements where the price can float. They want to see exactly what the final bill will be before they agree to the loan, which protects you from nasty surprises halfway through the project.

Navigating Construction Loans and Financing Your Dream

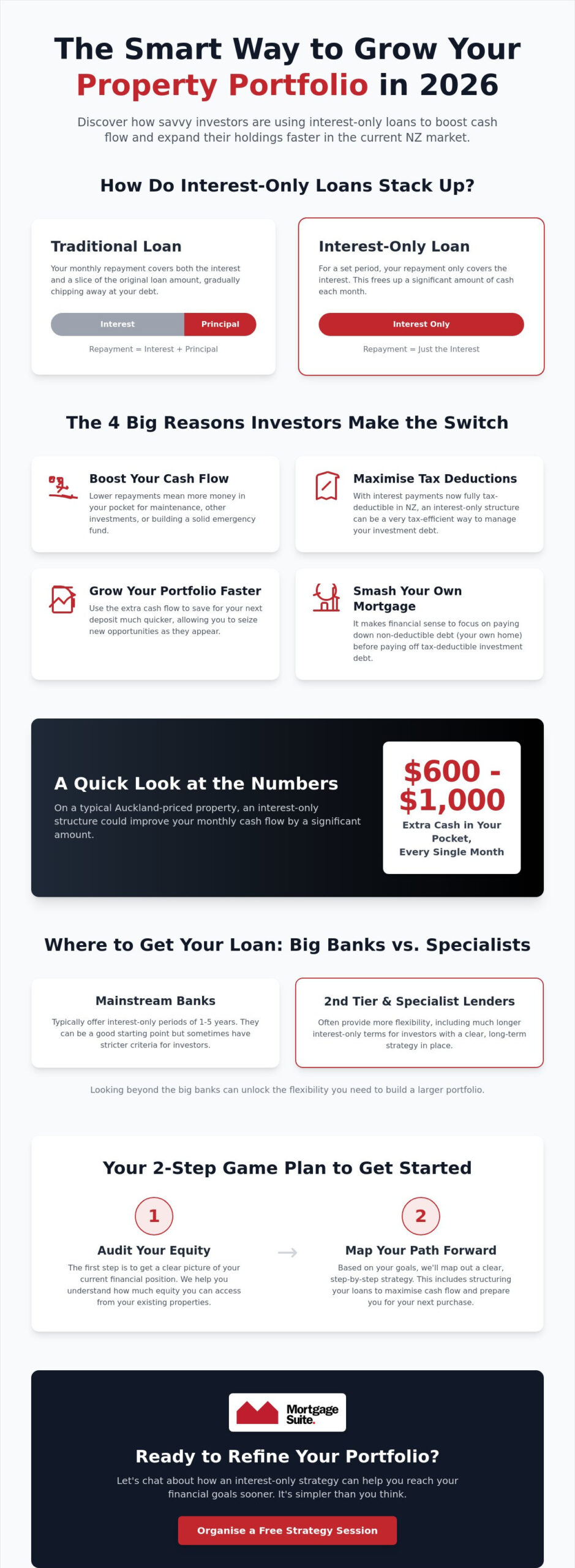

Buying a finished home is a lot like buying a car; you pay the price and drive it away. However, buying land and building a house nz is more like a subscription service where you pay as you go. A construction loan is fundamentally different from a standard mortgage because the bank doesn’t give you all the money at once. Instead, they release funds in chunks, known as “drawdowns,” only after specific milestones are reached on-site. This keeps the project on track and ensures the bank isn’t lending more than what the property is currently worth at any given moment.

The “progressive drawdown” process usually follows the natural rhythm of your build. You’ll start with an initial payment for the land, followed by stages like the floor slab, the wall framing, the roof, and the final interior fit-out. Before the bank pays out each stage, they’ll want to see an invoice from your builder. Sometimes, they’ll even send a valuer to the site to check that the house actually has a roof before they pay for one. This methodical approach might feel like extra paperwork, but it’s a safety net that ensures your builder is being paid for work actually completed. For more details on homeowner rights during this phase, the official government guide to building is a great resource to have on hand.

One of the best features of these loans is that they are typically interest-only during the construction phase. This is a lifesaver for your weekly budget. Since you’re likely still paying rent or a mortgage elsewhere while you wait for the keys, you only pay interest on the amount you’ve actually drawn down. If you’ve only used $100,000 for the land and the slab, you only pay interest on that $100,000, not the full $800,000 loan. This keeps your costs manageable until the day you finally move in and convert to a standard principal and interest mortgage.

Mainstream Banks vs 2nd Tier Lenders

If your local bank branch says “no” because your deposit is a bit light or your income is slightly unconventional, don’t pack up your tools just yet. Second-tier lenders often provide the flexibility that big banks lack. They are often more willing to look at the overall value of your project rather than just ticking boxes. These non-bank lenders can be the perfect bridge to get your project off the ground, especially for land purchases that don’t fit the standard criteria. You can find out more about these alternative options in our 2nd tier lender New Zealand guide.

Using Equity and KiwiSaver

You don’t always need a pile of cash sitting in a savings account to start. If you already own a property, you might be able to use the equity in that home to cover your new deposit. For those starting from scratch, KiwiSaver remains a powerful tool. In 2026, you can still withdraw your savings for a first home build, provided you’ve been a member for at least three years. We cover all the latest rules and tips in our home loans for first home buyers New Zealand guide to ensure you’re making the most of every dollar available to you.

Budgeting for Your Build: Hidden Costs and How to Avoid Them

When you’re buying land and building a house nz, the number at the bottom of your build contract is rarely the number you’ll see on your final bank statement. It’s easy to get swept up in the excitement of choosing tiles and tapware, but the real budget killers are the costs that never even make it onto the builder’s quote. Understanding these “invisible” expenses early is the difference between a smooth project and a stressful financial scramble halfway through the frame stage.

One of the most significant surprises for new builders is the development contribution. Councils charge these fees to fund the extra pressure your new home puts on local infrastructure like water pipes, sewerage, and roading. Depending on your region, this can add thousands to your total. You also need to account for professional fees before a single nail is driven. Architects, surveyors, and structural engineers all play a vital role in getting your plans approved, and their expertise is essential for navigating the complex soil conditions often found across New Zealand.

Don’t forget the “finishing” costs that many standard contracts leave out. It’s common for a build price to exclude the driveway, fencing, basic landscaping, and even your letterbox or clothesline. If you don’t budget for these from day one, you might find yourself living in a beautiful new home surrounded by a sea of mud. To get a realistic view of your borrowing capacity and account for these hidden fees, book a strategy session with our team today.

The Council and Consent Maze

You’ll need to navigate two main types of permission: resource consent and building consent. Resource consent deals with how your home affects the land and neighbours, while building consent ensures the structure itself is safe and up to code. In 2026, it’s vital to plan for council fee increases and the new combined building levies which aim to streamline the process. Your goal is the Code Compliance Certificate (CCC); this is the most important document you’ll ever own, as it proves the house is finished correctly and allows the bank to finalise your loan.

Managing Your Contingency Fund

Lenders almost always insist on a 10% to 15% contingency buffer before they approve a construction loan. This isn’t just “extra money” for the bank; it’s a safety net for “variations” that occur once work begins. Perhaps the diggers found unexpected rock underground, or you decided to upgrade the kitchen cabinetry at the last minute. A fixed-price contract is your best friend because it provides a legal shield against fluctuating material costs and ensures the bank has a clear figure to lend against. Having that buffer ready means these small changes won’t bring your entire build to a grinding halt.

Making It Happen: How an Expert Broker Simplifies the Build Process

Navigating the financial side of buying land and building a house nz is often the most stressful part of the entire project. While your builder focuses on the physical structure, you need someone who understands the inner workings of the banking world to ensure the money keeps flowing. This is where a specialist broker becomes your most valuable asset. We don’t just find you a loan; the team at Mortgage Suite Ltd acts as your dedicated negotiator, ensuring the bank’s requirements align with your builder’s timeline and your personal budget.

We bridge the gap between your vision and the bank’s rigid boxes. We manage the constant back and forth communication between you, your lender, and your construction team. This means when a drawdown is due or a variation occurs, you aren’t stuck in the middle trying to translate banking speak into builder speak. We organise the paperwork and the approvals so you can stay focused on the exciting parts of your new home without the administrative headache.

The Mortgage Suite Ltd Advantage

Our approach is built on Krish Krishna’s 20 plus years of deep banking experience. Having seen the process from inside the big banks, Krish knows exactly how to present your application to get a “yes” faster. We also offer a significant advantage by looking beyond the high street lenders. If your project doesn’t fit standard criteria, we can tap into our network of 2nd tier loans that offer more flexibility for unique builds or smaller deposits. We take pride in making these complex financial structures feel simple, conversational, and easy to follow.

Ready to Start Your Build Journey?

The first step is always the most important. We offer a personalised assessment to help you understand your true borrowing power before you sign any contracts. We’ll help you organise your documents and create a clear finance plan that covers everything from the initial land purchase to the final council sign-off. If you’re looking at larger scale builds or multi unit sites, you might also find our property development loans NZ guide particularly useful for understanding how to fund your next big project. Let’s get your build moving with confidence and a professional in your corner.

Ready to Turn Your Vision Into a Reality?

Building your own home is a massive undertaking, but it’s also one of the most rewarding ways to secure your future in New Zealand. We’ve explored how the right section dictates your budget and how to manage the unique “pay as you go” nature of construction loans. By staying ahead of hidden council fees and keeping a solid contingency buffer, you can avoid the common pitfalls that often trip up first-time builders.

Success when buying land and building a house nz comes down to having a steady hand to guide you through the banking maze. We bring over 20 years of industry experience to the table, specialising in 2nd tier lending for those who don’t fit the standard bank boxes. Our team is dedicated to providing personalised, jargon-free advice that makes your finance feel like the easiest part of the build.

You have the dream; now it’s time to build the foundation. Chat with Krish and the team at Mortgage Suite today to plan your build finance and take that first confident step toward your new front door. Your dream home is closer than you think.

Frequently Asked Questions

Can I use my KiwiSaver to buy land if I am not building immediately?

No, you generally cannot use your KiwiSaver funds just to hold onto a piece of land. To make a withdrawal, you must intend to build your first home on that section as your primary residence. Lenders and the government usually require a clear plan or a build contract to prove that construction will start within a reasonable timeframe after the land purchase is finalised.

How much deposit do I need to buy land and build in NZ in 2026?

Most New Zealand banks require a minimum 20% deposit for vacant residential land within urban boundaries. If you are looking at lifestyle blocks or rural land, this requirement often increases to between 30% and 50%. However, when buying land and building a house nz as part of a total package, some specific schemes may allow eligible buyers to start with as little as a 5% deposit.

What is a Master Build guarantee and why do lenders want to see it?

A Master Build guarantee is a 10-year protection plan that covers structural defects, workmanship issues, and builder insolvency. Lenders insist on seeing this because it significantly reduces their financial risk. It provides a safety net that ensures the project will be completed even if the builder runs into trouble, protecting both your investment and the bank’s security.

How do progress payments (drawdowns) work during a build?

Progress payments are released in stages as your builder hits specific milestones on the construction site. Instead of getting the full loan at the start, the bank pays out for completed work such as the floor slab, framing, and the roof. This methodical process ensures that the builder is paid fairly for work already done while keeping the project on a strict financial schedule.

Can I get a loan for a tiny house or a transportable home on bare land?

Yes, it is possible, but it is often more complex than a standard residential loan. Most mainstream banks require the home to be fixed to permanent foundations and connected to all essential services before they will consider it a mortgageable property. If the big banks aren’t comfortable with your project, we can often find more flexible options through our network of second-tier lenders.

What happens if my build goes over budget during construction?

If your build costs exceed the original estimate, you will typically use your 10% to 15% contingency fund first. If the costs climb even higher, you may need to apply for a loan top-up or contribute more of your own savings. This is why we always advocate for a fixed-price contract, as it provides a legal shield against unexpected price hikes for materials or labour.

Is interest-only the best way to pay for a construction loan?

Interest-only repayments are a popular choice during the build phase because they keep your weekly costs low while you might still be paying rent or another mortgage. You only pay interest on the amount of the loan you have actually used. Once the house is finished and you have your final council sign-off, the loan usually converts to a standard principal and interest mortgage.

How long does it take to get a construction loan approved in NZ?

You should generally allow between 5 and 10 working days for a construction loan approval, provided your paperwork is complete. The process can take a bit longer if the bank needs to review detailed build contracts, Geotech reports, or specific council consents. Having a broker organise your application upfront ensures the bank has everything they need to give you a faster answer.