What if the bank’s “no” isn’t actually a reflection of your business’s health, but simply because you’re playing by the wrong set of rules? When you’re ready to buy commercial property loan NZ requirements can often feel like a massive hurdle, especially when you’re met with rigid criteria and deposit demands that look nothing like a standard home mortgage. You’ve worked hard to grow your company, and the last thing you need is a confusing process or worries about personal liability standing in the way of owning your own premises.

We know that the shift from a residential mindset to a commercial one can feel like learning a new language overnight. It’s a different world where mainstream banks look for specific interest cover ratios and seismic ratings before they’ll even consider an application. This guide will show you exactly how to navigate the lending landscape in 2026 without the jargon. We’ll explore whether a big bank or a flexible 2nd tier lender is your best fit, providing a clear roadmap to help you secure a permanent home for your business to thrive.

Key Takeaways

- Understand why your home loan experience won’t prepare you for the commercial world and how to shift your mindset to business-zoned finance.

- Discover the specific numbers lenders look for, including why you’ll likely need a 35% deposit when you buy commercial property loan NZ wide.

- Find out how to choose between the “Big Four” banks and flexible 2nd tier lenders based on your business’s unique needs.

- Get a clear checklist for organising your financial story, including why a professional valuation is different from a standard home appraisal.

- Learn how a seasoned advocate can use their “bank-to-broker” experience to negotiate a “yes” even when mainstream criteria feel too rigid.

What is a Commercial Property Loan and Why is it Different?

Think of a commercial loan as the business version of a mortgage. If you have ever bought a house, you probably feel like you understand how the lending process works. However, when you decide to What is a Commercial Property Loan exactly? Essentially, it is finance specifically for buildings zoned for business use rather than living in. This includes anything from a small retail shop in the city centre to a massive warehouse in an industrial park or a professional office suite. Most Kiwis look into these loans for two main reasons. They either want the stability of owning their own business premises to stop paying rent, or they are looking for the higher rental returns that commercial properties often provide compared to residential rentals.

The biggest shock for most people is that your previous home loan experience won’t prepare you for this world. Banks view these properties as higher risk than a standard family home. Because of that, the rules of the game change completely. You aren’t just a homeowner anymore; you are a business operator or a commercial investor in the eyes of the lender. This shift in perspective changes everything from how much you can borrow to how quickly you need to pay it back.

The Core Differences: Residential vs. Commercial

One of the first things you will notice is the deposit requirement. While you might get a house with a 20% deposit, a buy commercial property loan NZ wide typically requires at least 35%. This 65% Loan-to-Value Ratio (LVR) is the standard for most mainstream lenders in 2026. Another major shift is the loan term. You won’t find 30-year terms here; most commercial loans are structured over 15 to 20 years. Lenders also focus heavily on whether the building can “pay for itself” through rent or business profit. They use a calculation called an interest cover ratio to ensure your income comfortably exceeds the loan repayments.

Who is a Commercial Loan For?

Most of our clients fall into two camps. The owner-occupier is a business owner who wants to secure their future. Instead of being at the mercy of a landlord, they buy their own building to give their company a permanent base and build equity. Then there is the investor. These people are looking for yield and long-term growth by leasing the space to other businesses. In both cases, the bank cares deeply about your business history. Your GST returns and profit/loss statements carry more weight than your personal credit card limit. They want to see a track record of success that proves you can handle the repayments even if the market fluctuates.

Understanding the Numbers: How Lenders Decide to Say Yes

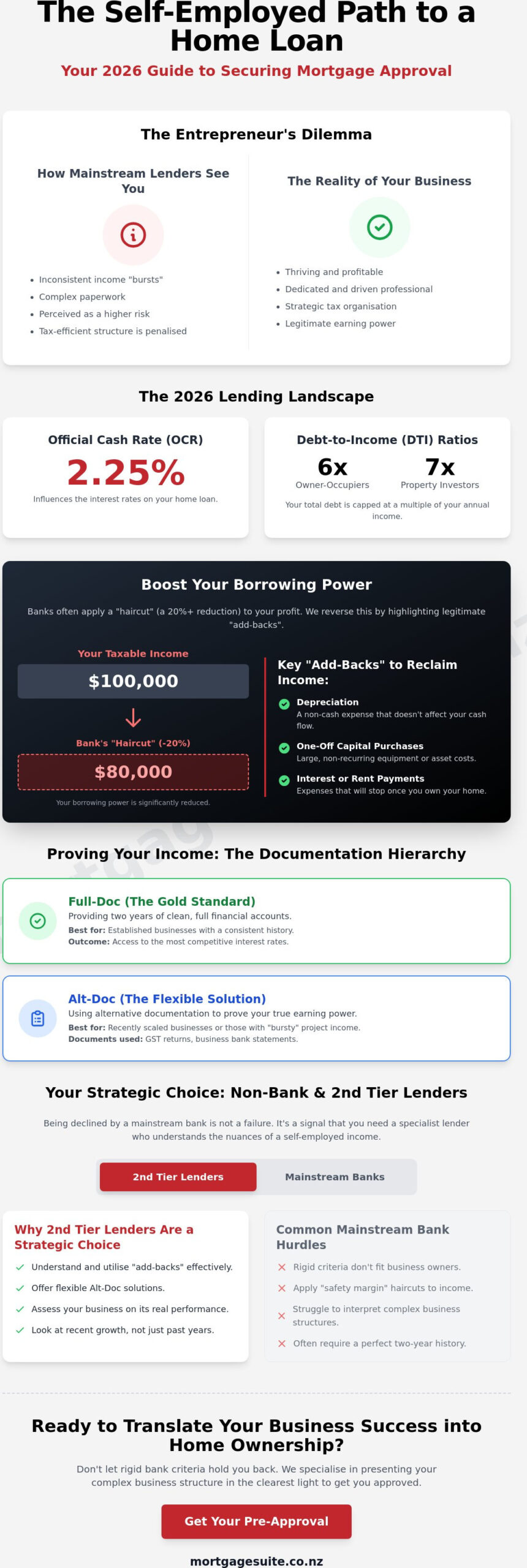

Numbers might feel cold and clinical, but to a bank, they tell the story of how safe their money is. When you look to buy commercial property loan NZ lenders will scrutinise your “interest cover” before anything else. This is a simple calculation to see if your business profit or rental income can comfortably handle the interest payments. In 2026, most mainstream banks want to see a ratio of at least 1.50x to 1.75x. This means for every dollar of interest you owe, they want to see at least $1.50 in reliable income coming through the door. It is their way of ensuring you have a safety net if things get a bit tight.

In the 2026 market, the Loan-to-Value Ratio (LVR) is simply the percentage of the property’s total value that the bank is willing to lend you, which for commercial buildings usually tops out at 65%. This “65% Rule” is why you generally need a 35% deposit, a significant jump from the 20% often seen in the residential world. If you find these calculations a bit daunting, getting some professional mortgage advice early on can help you see exactly where you stand before you start making offers.

Deposit and Equity Requirements

You don’t always need a pile of cash sitting in a savings account to meet that 35% requirement. Many Kiwi business owners use the “lazy equity” in their own homes to bridge the gap. By securing part of the commercial loan against your residential property, you can often fund the entire purchase without touching your cash flow. However, the type of building matters immensely. A standard warehouse or office is easy for a bank to value. On the other hand, specialised buildings like car washes, gyms, or cold-storage facilities often face stricter rules because they are harder to sell or repurpose if the business closes.

The Lease: Your Secret Weapon for Approval

If you are buying an investment property, the lease is your most valuable asset. Lenders love a “strong” lease, which usually means a well-known tenant with several years left on their contract. They look closely at the Weighted Average Lease Expiry (WALE). Think of this as the “time left on the clock” across all tenants in the building. A longer WALE gives the bank confidence that the mortgage will be paid.

- Long-term tenants: These are like gold to a lender and can sometimes help you secure better interest rates.

- Vacant buildings: These are much harder to finance. Banks see a building with no tenant as a 100% risk, often requiring you to prove you have enough cash reserves to cover the mortgage for a year or more while you find a tenant.

- Tenant quality: A lease to a government department or a national brand is viewed far more favourably than a lease to a brand-new startup.

Mainstream Banks vs. 2nd Tier Lenders: Choosing Your Path

Choosing the right lender is about more than just finding the lowest number on a page. When you decide to buy commercial property loan NZ options generally fall into two categories: the household name banks and the specialised alternative lenders. Many business owners feel a sense of loyalty to their current bank, but in the commercial world, that loyalty isn’t always rewarded with an easy approval. The reality of the 2026 market is that the “Big Four” have become increasingly selective about who they take on, often leaving small to medium businesses searching for a more flexible partner.

A “no” from your local branch manager isn’t the end of the road; it’s often just a sign that you’re knocking on the wrong door. Different lenders have different appetites for risk. One bank might have reached its limit for retail properties in your specific suburb, while a non-bank lender might be actively looking to grow their portfolio in that exact sector. Understanding these nuances is the key to getting your finance across the line without unnecessary stress.

When the Bank is the Right Choice

The major banks in New Zealand are an excellent choice if you fit into a very specific “perfect” box. They look for clean financial records, several years of steady profit, and properties with long-term, reliable tenants. If you meet these strict requirements, a commercial mortgage New Zealand banks offer will likely provide the most competitive interest rates. However, be prepared for a slower pace. Mainstream institutions are known for their lengthy “committee” approval processes, which can be a major disadvantage if you need to move quickly on a property before a competitor beats you to it.

The Power of Non-Bank and 2nd Tier Lending

If your business has seasonal income or you’ve only been trading for a couple of years, a 2nd tier lender New Zealand wide might be a better fit. These lenders are built for speed and flexibility. They often look at the “big picture” of your business potential rather than just a computer-generated credit score. While interest rates can be higher, with some non-bank providers starting from 6.95% and others ranging up to 20.95% for higher-risk scenarios, they offer solutions that mainstream banks simply won’t consider. This path is particularly useful for business owners who need to secure a building quickly and plan to refinance to a major bank once they have a longer track record of success. When you buy commercial property loan NZ requirements vary wildly, so having access to these alternative paths ensures you aren’t left stranded by a single bank’s rigid policy.

5 Steps to Getting Your Commercial Loan Sorted

Getting the green light for your finance involves a bit more than a quick chat and a handshake. When you’re looking to buy commercial property loan NZ lenders will expect a methodical approach. It’s about building a case that proves your business is a safe bet. Following a structured path ensures you don’t get caught out by unexpected requests halfway through the process. It’s a steady journey from your initial idea to finally holding the keys to your own premises.

Preparing Your Paperwork

Your first task is to organise your financial “story”. This isn’t just about handing over a few bank statements; it’s about showing the bank your trajectory. You’ll need at least two years of GST returns and up-to-date profit and loss statements ready to go. If you’re an owner-occupier, a solid business plan is vital. It shows the lender how owning this building will help your company grow and improve your long-term stability. Sometimes, a small business loan NZ lenders provide can work alongside your property finance to cover fit-out costs or new equipment for your new space.

The Valuation and Due Diligence

Once the paperwork is in, you’ll need a professional valuation. Unlike a house appraisal, a commercial valuation is a deep dive into the building’s income potential and structural health. Lenders will only accept reports from their own approved panel of valuers, so don’t jump the gun and hire someone yourself. They’ll also look at environmental risks and whether the building complies with the Building Act, especially concerning seismic ratings. A low earthquake rating can drastically change your loan terms, so it’s best to get a professional loan assessment before you sign any unconditional contracts.

Step 3 involves choosing your lender path with an expert who knows the current appetite of the market. Based on the scenarios we discussed earlier, you’ll decide whether a mainstream bank or a flexible 2nd tier lender is the right home for your loan. Once you’ve selected a lender, you’ll move to Step 4: navigating the “Conditional Approval” phase. This is the stage where you satisfy the lender’s final checks, such as proof of insurance or verifying lease details. Finally, Step 5 is settlement and beyond. This is where the final paperwork is organised, funds are transferred, and you officially take ownership of your new business asset.

How Mortgage Suite Negotiates the Best Deal for You

Finding the right building is a massive milestone for any company, but the finance phase is where things often get tricky. This is where we step in. Our team brings years of “bank-to-broker” experience to your side of the table. Because we have spent years working inside major New Zealand banks, we understand the hidden boxes that need to be ticked to get an approval. We know how to frame your financial story so it doesn’t just meet the criteria but actually stands out to the people making the decisions.

We act as your personal advocate. When you want to buy commercial property loan NZ lenders can sometimes be incredibly rigid, especially if your business doesn’t fit a standard template. We don’t just pass on a message; we negotiate. If one lender says “no” because of a specific internal policy, we know which alternative lender will see the value in your proposal. You get a single point of contact who manages the entire journey, from that first conversation to the day you move in.

Taking the stress out of the paperwork is our priority. You should be focused on running your business and planning your growth, not chasing bank managers for updates or worrying about fine print. We handle the heavy lifting, ensuring every document is in its right place so there are no last-minute surprises at settlement. We’re here to make sure you get a fair go and the best possible terms the market has to offer.

A Personal Approach to Complex Finance

We treat your business like our own. We aren’t interested in just a one-off transaction; we want to build a long-term partnership that supports your success for years to come. That means looking at how your property fits into your wider goals. As the market shifts and your equity grows, we can also help with a Commercial Property Refinance NZ down the track. This allows you to unlock capital for further expansion or move to better interest rates as your business track record strengthens.

Ready to Secure Your Business Future?

If you’re ready to stop paying rent and start building your own business asset, the first step is a simple conversation. We’ll give you a quick, honest assessment of your borrowing power based on the 2026 lending environment. Our focus is always on your specific goals first, followed by the numbers. We’ll help you understand exactly what’s possible so you can bid with confidence and secure the premises your business deserves.

Get in touch with the Mortgage Suite team today to get your commercial loan sorted. Let’s find the right “home” for your business finance together.

Secure Your Business’s Future Today

Owning your own premises is more than just a financial move; it is a commitment to the longevity of your business. We have covered why the 65% deposit rule matters and how the right lease can act as your secret weapon when you apply for a buy commercial property loan NZ wide. Whether you fit the strict criteria of a major bank or need the flexibility of a 2nd tier lender, the key is having a roadmap that avoids the usual jargon and delays.

With over 20 years of banking and brokerage experience, we specialise in finding solutions for “non-standard” situations that others might find too complex. We pride ourselves on a personalised service that treats you like a partner, not just a number on a spreadsheet. If you are ready to stop paying rent and start building equity, we are here to guide you through every step of the negotiation and paperwork.

Book a conversational chat with Krish Krishna to discuss your commercial goals and get a clear picture of your borrowing power today. Your business deserves a permanent home, and we have the expertise to help you get there.

Frequently Asked Questions

How much deposit do I need to buy a commercial property in NZ?

You typically need a 35% deposit for a standard commercial purchase in New Zealand. While residential buyers are used to 20%, commercial lenders usually cap their lending at 65% of the property’s value. Some non-bank lenders might offer slightly more flexibility, sometimes allowing for a 30% deposit if the business case and the building’s location are particularly strong.

Can I use my house as security for a commercial property loan?

Yes, you can certainly use the equity in your home to secure a buy commercial property loan NZ wide. This is a popular strategy for business owners who don’t want to tie up their working capital in a cash deposit. By using your residential property as additional security, you can often fund the entire purchase and keep your cash for growing the business.

What is the current interest rate for commercial loans in New Zealand?

Interest rates vary significantly depending on whether you choose a mainstream bank or a 2nd tier lender. With the Official Cash Rate sitting at 2.25% in July 2026, mainstream banks offer competitive but tailored rates. Non-bank lenders often start their rates around 6.95%, though these can reach up to 20.95% for higher-risk or short-term “bridge” loans that prioritise speed over cost.

How long does it take to get a commercial loan approved?

Approval times depend entirely on the lender you choose. Mainstream banks are thorough and can take several weeks or even months to move through their internal committees. If you are in a rush to settle, a 2nd tier lender can often provide an answer and get the deal sorted in a matter of days because they have more streamlined processes and direct decision-making.

What happens if my business hasn’t been trading for two years yet?

You can still secure a loan even if your business is relatively new. While mainstream banks generally prefer at least two years of solid trading history, alternative lenders are often willing to look at your professional experience and future projections. They focus more on the “big picture” and the value of the property itself rather than just relying on your past tax returns.

Is it harder to get a commercial loan than a residential one?

It is generally more difficult because lenders view commercial assets as higher risk than family homes. The criteria are stricter, requiring higher deposits and proof that the building’s income can comfortably cover the interest. You also have to navigate specific checks like seismic ratings and environmental reports that simply don’t apply to standard residential houses in the city centre.

Can I get a commercial loan if I’ve been declined by a bank?

Being declined by a bank is not the end of the road. Many of our clients come to us after a “no” from their local branch manager. Because 2nd tier lenders have different appetites for risk and more flexible rules, we can often find a path to approval by matching your specific scenario with the right alternative lender who understands your industry.

Do I need a personal guarantee for a commercial mortgage?

Most lenders will require a personal guarantee, especially if you are borrowing through a company structure. This gives the bank an extra layer of security, ensuring that the directors are personally committed to the loan. It is a standard part of the process for small to medium businesses in New Zealand, though the specific terms can sometimes be negotiated depending on your equity.