What if your most valuable asset was currently working harder for the bank than it was for your own business growth? Most Kiwi business owners feel the sting of a “no” from traditional lenders, especially when they’re told their venture is too new or their paperwork doesn’t fit a rigid, pre-defined box. It’s incredibly frustrating to sit on significant equity while your expansion plans gather dust because of slow approvals. This is where property backed business loans nz come into play, offering a way to bypass the red tape and confusing financial jargon that usually makes borrowing feel like an impossible hurdle.

With the Official Cash Rate sitting at 2.50% and the market showing signs of a steady recovery, now’s the time to use what you already own. You deserve a partner who sees the potential in your property rather than just the risks on a balance sheet. This guide will show you how to turn your equity into fast, flexible capital without the usual bank-induced headaches. We’ll explore how much you can realistically borrow in the 2026 market, the simple path to securing funds, and why 2nd tier lending is the smart solution for those who don’t fit the standard mould.

Key Takeaways

- Access significantly larger amounts of funding than a standard overdraft by using your property equity as security for your business growth.

- Discover how property backed business loans nz provide a more affordable path to capital through lower interest rates compared to unsecured finance options.

- Learn why flexible 2nd tier lenders are often the best choice when mainstream banks decline your application due to rigid “standard” criteria.

- Follow a straightforward guide to calculating your usable equity and defining your business purpose to ensure a fast and simple approval process.

- Leverage over twenty years of insider banking expertise to bypass traditional headaches and secure the funding your business needs to thrive in 2026.

What exactly are property backed business loans in NZ?

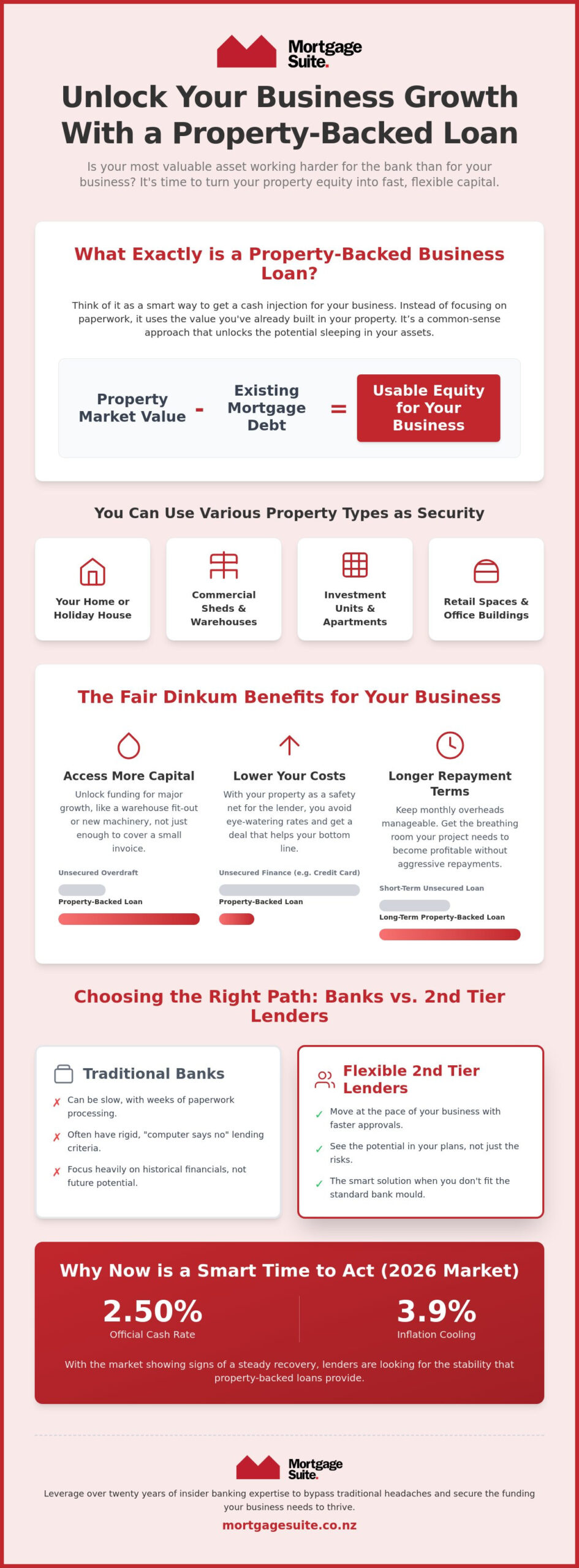

Think of a property backed business loan as a way to unlock the value currently sleeping in your physical assets. It is essentially a cash injection where your “bricks and mortar” do the heavy lifting for you. Unlike a standard personal loan or a credit card, which rely almost entirely on your personal income or a high credit score, property backed business loans nz focus on the equity you’ve built over time. It’s a practical, common-sense approach to funding that recognizes the real-world value of what you own.

Your borrowing power is directly tied to your equity. This is the difference between the current market value of your property and any debt you still owe on it. In the current 2026 climate, with the Official Cash Rate sitting at 2.50% and inflation showing signs of cooling at 3.9%, lenders are looking for stability. Having a tangible asset as security makes you a far more attractive prospect than someone walking in with nothing but a business plan. You can use various property types to secure this funding, including:

- Your primary residential home or a holiday house.

- Commercial sheds, warehouses, or workshops.

- Residential investment units or apartment blocks.

- Retail spaces and office buildings.

The difference between secured and unsecured funding

The concept of Asset-based lending is built on the idea of security. When a loan is “secured” against property, it gives the lender a safety net; this confidence usually translates into much lower interest rates for your business. Unsecured funding, like a business credit card, often comes with eye-watering rates because the lender has nothing to fall back on if things go south. The trade-off is straightforward: you use your asset as a guarantee to access significantly more capital at a price that doesn’t cripple your monthly cash flow.

Why Kiwi business owners are choosing asset lending in 2026

The financial world has changed. We’ve seen a clear shift away from rigid, “computer says no” bank managers toward more flexible, 2nd tier lenders. These providers are often more interested in your future potential than your past mistakes. Speed is a massive factor here. While a traditional bank might take weeks to process a stack of paperwork, property-backed solutions can often be sorted in a fraction of the time. This provides a vital lifeline when cash flow is lumpy or an unexpected opportunity requires an immediate response. It’s about moving at the pace of your business, not the pace of a bank’s head office.

The fair dinkum benefits of using your property for business growth

Using your own property as a springboard for your business is one of the smartest moves a Kiwi entrepreneur can make. It’s about more than just getting a “yes” from a lender. It’s about getting a deal that actually works for your bottom line. When you look at property backed business loans nz, the most obvious win is the sheer scale of funding available. While an unsecured overdraft might give you enough to cover a small invoice or two, using your equity can unlock the kind of capital needed for a major warehouse fit-out, new machinery, or a full-scale marketing push that actually moves the needle.

It’s not just about the amount, though. It’s about the cost. Because the lender has the “safety net” of your property, they’re not taking as much of a gamble on your daily cash flow. This means you’re not stuck paying the double-digit interest rates typically found with business credit cards or those “quick cash” lenders that advertise on the radio. You get access to professional rates that reflect the stability of your asset. Plus, you can often secure longer repayment terms. This is a game-changer for keeping your monthly overheads manageable, giving your new project the breathing room it needs to become profitable before you have to worry about aggressive repayments of the actual amount borrowed.

Lowering your cost of capital

Your interest rate isn’t just a random number plucked from thin air. It often reflects the quality and location of the property you’re putting forward as security. To get the best possible deal, it pays to organise your finances and show a clear plan for the funds. By moving away from high-interest debt and onto a property-backed structure, you’re essentially giving your business a pay rise by reducing your monthly interest bill. It’s a way to make your existing assets work harder so you can focus on the work that actually generates revenue.

Flexibility for non-standard situations

One of the biggest hurdles for small businesses is the “three-year rule” many banks insist on. If you’re self-employed or running a fresh start-up, you might not have years of perfect tax returns to show. Asset-based lending focuses on what you have now rather than where you were three years ago. If you already have a portfolio, you can even use residential investment property loans NZ as a source of equity to fuel your business dreams. This flexibility makes property backed business loans nz a primary choice for those who don’t fit the standard bank box but have the drive and the assets to succeed. If you want to see what’s possible for your specific situation, it’s always a good idea to talk to an expert about your options.

Banks vs. 2nd Tier Lenders: Choosing the right path

Most business owners start their search for property backed business loans nz at their local bank branch. It makes sense because that is where your accounts are and where you likely have your home mortgage. However, in 2026, the gap between what a mainstream bank wants and what a growing business actually needs has become quite wide. While banks offer attractive interest rates, they often come with a level of rigidity that can stall your progress just when you need to move quickly.

The big banks typically demand “perfect” paperwork. This usually means three years of audited accounts, a spotless credit history, and a business model that fits into a very specific, low-risk category. If you are a builder, a developer, or a new start-up, you might find that the bank is hesitant to help, regardless of how much equity you have. This is the hidden cost of a “cheap” bank loan. The slow approvals and rigid terms can end up costing you more in lost opportunities than you save in interest.

This is where a 2nd tier lender New Zealand business owners rely on becomes a strategic partner. These lenders are specialists in saying “yes” when the mainstream banks say “no”. They aren’t just a backup plan; they are often the primary choice for entrepreneurs who value speed and flexibility over bank-mandated red tape. They look at the current value of your assets and the potential of your business rather than just your past tax returns.

When the bank says no: alternative solutions

Banks often decline applications for minor credit blips from years ago or because they’ve decided to pull back on lending to your specific industry. Alternative lenders take a broader view. They focus on the big picture, especially the value of your property. Having a veteran negotiator like Krish on your side is vital here. With over twenty years of experience, he knows exactly how to present your case to these lenders to ensure they see the strength of your position, effectively bridging the gap between rigid institutional rules and your personal funding needs.

Speed of funding: a critical factor

In the business world, timing is everything. A typical bank timeline can stretch for weeks as your application moves through various committees. Asset-based loans through 2nd tier providers are built for speed. When you have your property details ready to go, these lenders can often move through the approval process in a matter of days. This fast-track approach is a game-changer when you need to secure a new contract, buy stock at a discount, or manage a sudden cash flow dip. It is about getting the capital you need without the usual administrative headaches.

How to qualify for a property backed business loan

Qualifying for a loan shouldn’t feel like sitting a university exam. While the big banks often make you jump through hoops, the process for property backed business loans nz is designed to be much more straightforward. The focus shifts from your historical paperwork to the actual value of your asset. If you have equity in a house, an office, or a warehouse, you’re already halfway there. You don’t need to have a perfect credit score or a decade of trading history to get a seat at the table.

To get things moving, you can follow these simple steps:

- Step 1: Calculate your usable equity. Take the current market value of your property and subtract what you still owe on your mortgage. This is your “pot of gold” for business funding.

- Step 2: Define your business purpose. Whether you’re buying new equipment, hiring staff, or just need a cash flow buffer, having a clear goal helps lenders understand the “why” behind the loan.

- Step 3: Gather your paperwork. We don’t need years of audited accounts. Even if you don’t use specific software like MYOB or Xero, we can work with bank statements or basic profit and loss summaries.

- Step 4: Speak with a specialist. This is where you get a lender match that fits your specific needs rather than a “one size fits all” bank product.

- Step 5: Get a valuation. A professional valuer will confirm the property’s worth, and you’ll receive your formal offer.

Understanding the loan-to-value ratio (LVR)

LVR is just a fancy way of saying “how much can I borrow against the house?” In the current 2026 market, a standard LVR for commercial properties is around 65%. This means you’ll typically need a 35% deposit or existing equity in the property. For residential security, that percentage can often be higher. If you want to get a better interest rate, having a lower LVR is a great way to show the lender that their investment is extra safe.

Preparing your “business story”

Lenders are people too, and they want to feel confident in your plan. You don’t need a 50-page business plan, but you should be able to explain how the funds will help you grow. When you can show that the capital will lead to more revenue or better efficiency, it builds trust. This clear plan makes the whole approval process move much faster. If you’re ready to see how much equity you can unlock, you can start your application process today and get a clear answer without the usual bank delays.

Why Mortgage Suite is your best partner for business finance

Choosing the right partner for your business finance is a decision that can shape your company’s future for years to come. You need more than just a broker; you need someone who knows the financial system from the inside out. At Mortgage Suite, we bring over twenty years of banking experience to the table, but there’s one major difference: we don’t work for the big banks. We work for you. We’ve spent decades seeing how rigid mainstream lenders can be, and we’ve made it our mission to bridge that gap. We specialise in property backed business loans nz that don’t fit into a standard, pre-defined box.

Our approach is deeply personal and consultative. We don’t just process applications or tick boxes; we listen to your business story and find the path that makes the most sense for your specific goals. While some providers only focus on their local area, we have a national reach that covers every corner of New Zealand. Whether you’re a tradesperson in Southland or a tech start-up in Auckland, we can help you unlock the equity in your assets. We pride ourselves on being a steady hand in a fluctuating market, providing the reliability and trust you need for significant financial moves.

The Mortgage Suite difference: your dedicated negotiator

When you work with us, you gain the advantage of a dedicated negotiator who knows how to speak the language of lenders. Krish Krishna uses his two decades of industry reputation to secure deals that you simply won’t find by going direct. We understand the “inside” of the banking world, which gives us a massive head start for cutting through red tape and overcoming obstacles. You’ll also benefit from having a single point of contact for all your needs, including specialised services like commercial property refinance NZ. This streamlined approach saves you time and ensures your entire financial strategy is working in harmony.

Getting started today

We know you’re busy running a business, so we’ve made our process as simple as possible. There are no complicated forms or endless phone trees here. We start with a straight talk about your goals and what you need to achieve them. We take the stress out of the application process by handling the heavy lifting, from the initial assessment right through to the final approval. Our goal is to make property backed business loans nz feel like a natural, easy extension of your business growth. If you’re ready to take the next step without the usual bank-induced headaches, let’s get your business funding sorted today and give your venture the capital it deserves.

Take the next step toward your business expansion

Your property is more than just a place to live or work; it’s a powerful financial tool that can fuel your next big move. By choosing property backed business loans nz, you’re opting for a faster, more flexible path to capital that respects the reality of running a business in 2026. You don’t have to settle for the slow approvals or rigid terms of traditional banks when alternative solutions are right here at your fingertips.

As a family-owned brokerage with over 20 years of industry experience, we specialise in finding 2nd tier lending options for those who don’t fit the standard bank mould. We take the stress out of the process with a personalised, consultative approach that puts your success first. Whether you’re looking to buy new equipment, manage cash flow, or fund a major development, we have the expertise to make it happen. You deserve a partner who advocates for you and understands the “inside” of the banking world. Talk to Krish about your business funding goals today and let’s get your expansion plans moving. Your business has incredible potential, and we’re here to help you unlock it.

Frequently Asked Questions

Can I use my family home to fund my business startup?

You can certainly use your family home to kickstart your new venture. Many Kiwi entrepreneurs find that using residential equity is the most effective way to secure funding when a business doesn’t have a long trading history. Because the property acts as a solid guarantee, lenders are often more willing to support a fresh startup that a traditional bank might view as too risky.

What happens if I already have a mortgage on the property?

You can still use your property for a loan even if you haven’t paid off your mortgage yet. We focus on your “usable equity,” which is the current market value of your home or building minus what you still owe the bank. If there is enough value left over, a second tier lender can often provide a property backed business loan nz by taking a second mortgage or a caveat over the title.

How fast can I get the money from a property backed loan?

You can often access your funds in a matter of days once the initial paperwork and valuation are sorted. This is significantly faster than the weeks or months typically required by mainstream banks. Because the loan is based on the value of your asset, the approval process is streamlined, making it an ideal solution when you need to move quickly on a business opportunity.

Do I need to have a perfect credit score for asset lending?

You don’t need a spotless credit history to qualify for this type of funding. Since the loan is secured against your “bricks and mortar,” lenders are much more flexible regarding past credit blips or a lack of traditional financial records. They are far more interested in the current value of your property and your plan for the future than a computer-generated credit score.

Is the interest rate fixed or floating for business loans?

Both fixed and floating interest rates are available, and the choice usually depends on your specific business goals. Many owners prefer a floating rate because it often allows for more flexibility to pay back the loan early without facing large penalties. However, if you prefer the certainty of knowing exactly what your repayments will be each month, a fixed rate can be organised to help with your long-term budgeting.

Can I use a commercial property instead of a residential one?

You can absolutely use a commercial building, such as a warehouse, office, or retail shop, to secure your business finance. Commercial assets are excellent forms of security and can often unlock significant amounts of capital. While the percentage you can borrow against a commercial property might differ slightly from a residential home, it remains a very popular way to fund business growth while keeping personal assets separate.

What are the fees involved in setting up a property backed loan?

You will typically encounter a few standard costs when setting up your property backed business loans nz. These generally include a lender’s establishment fee, the cost of a professional valuation from an approved valuer, and legal fees for registering the mortgage or caveat. We always ensure you have a clear understanding of these costs upfront so you can make an informed decision without any hidden surprises.

How long can I borrow the money for?

The term of your loan can be tailored to match your specific business requirements. Some owners only need a short-term “bridge” for six to twelve months to cover a specific project, while others prefer a longer term of several years to keep their monthly overheads as low as possible. We work with you to structure the repayment timeframe so it aligns perfectly with your expected cash flow and growth plans.