What if the size of your deposit isn’t actually the biggest hurdle to your next home loan anymore? It often feels like every time you get close to the finish line, the Reserve Bank shifts the goalposts; you’ve saved the deposit and found the house, only to worry that new regulations might stop you in your tracks. Understanding the debt to income ratio nz rules is now just as vital as having a solid credit score, especially as we navigate the 2026 property market.

We know how stressful it is to feel like your financial future is being decided by a complex spreadsheet. That’s why we’re here to clear up the confusion. You’ll learn exactly how these DTI limits affect your borrowing power and how to navigate them to secure your dream home or next investment. We’ll break down the specific maths behind the 6x and 7x thresholds, identify who qualifies for a “speed limit” exemption, and look at the path forward if your current bank says no. Whether you’re a first home buyer or a seasoned investor, there is always a way through the red tape when you have the right plan and a steady hand to guide you.

Key Takeaways

- Get a clear grip on how the debt to income ratio nz measures what you owe against what you earn, and why it’s now a top priority for lenders.

- Discover the specific 2026 borrowing limits for owner-occupiers and investors, so you know exactly where you stand before you start house hunting.

- Learn about the “speed limit” and new build exemptions that could help you secure a loan even if you don’t fit the standard RBNZ box.

- Find out how simple moves, like closing unused credit cards, can significantly improve your profile and increase your chances of a successful application.

- Explore why a rejection from a big bank doesn’t have to be the end of the road, especially when looking at 2nd tier options that offer more flexibility.

What is the Debt to Income (DTI) ratio in NZ?

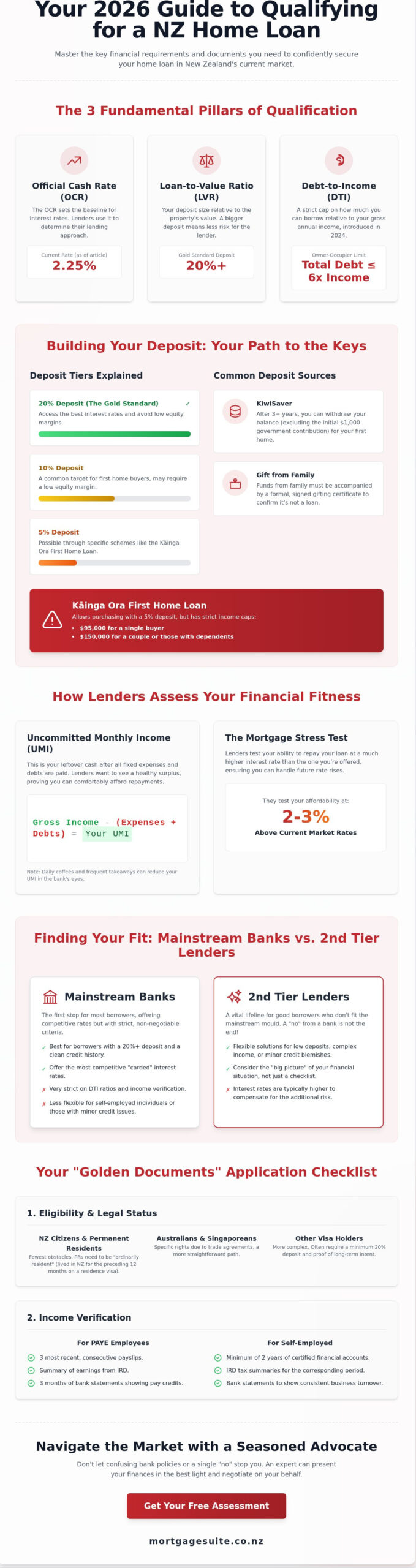

Think of the debt to income ratio nz as a financial health check that lenders use to see if you’re biting off more than you can chew. While we used to focus almost entirely on the size of your deposit, the rules have changed. Now, the banks are looking just as closely at the relationship between what you earn and what you owe. It isn’t just about your mortgage either. Lenders bundle in every bit of debt you have, from that credit card you keep for emergencies to the car loan you took out last year. If you’re curious about the global concept, you can read up on what the debt-to-income ratio is, but in the local context, it’s a strict guardrail designed to keep you and the economy safe.

In 2026, this ratio has become just as vital as your deposit size when you’re applying for a mortgage. It serves as a reality check for both you and the bank, making sure that your lifestyle isn’t entirely consumed by debt repayments. Living with a high ratio can be incredibly stressful, as it leaves very little room for error if your circumstances change. By understanding this number early on, you can take control of your financial story rather than letting the bank’s spreadsheet dictate your future. It’s about ensuring that you don’t end up taking on way too much debt, which can quickly turn the excitement of a new home into a constant worry about making ends meet.

The simple maths behind the ratio

Calculating this number is actually quite straightforward. To find your ratio, divide your total debt by your annual income before tax. For a practical example, let’s say your household brings in $100,000 a year before the taxman takes his share. If you’re looking to take on a $600,000 loan, your DTI would be 6. Banks prefer using your “gross” income, which is just the amount you earn before tax, because it provides a consistent starting point. It gives them a clear, standardised view of your total earning power before other expenses come into play.

Why the Reserve Bank brought these rules in

The Reserve Bank of New Zealand (RBNZ) introduced these limits to keep the housing market stable and prevent people from getting into too much hot water. By capping how much you can borrow relative to your income, they’re trying to stop the market from overheating and prevent people from getting in over their heads with repayments. These rules work alongside the existing Loan-to-Value (LVR) settings, which look at how much deposit you have. While LVR looks at your ownership stake, the DTI rules focus on your ability to actually live your life while paying back the debt. The ultimate goal is to make sure that even if interest rates wiggle or life throws you a surprise, you still have enough cash left over to keep the lights on and the fridge full. It’s about building a bit of a buffer so that a small change in your circumstances doesn’t become a massive financial headache. Understanding how the Reserve Bank sets its benchmark rate is equally important — our guide on OCR meaning and how the Official Cash Rate shapes your mortgage in 2026 explains exactly how these decisions flow through to your repayments.

The RBNZ rules: How much can you borrow in 2026?

The Reserve Bank doesn’t apply a one-size-fits-all approach to lending. Instead, they’ve set different benchmarks based on how you intend to use the property. If you’re looking for a place to call home, the standard debt to income ratio nz limit is 6. This means that for every dollar you earn before tax, the bank generally won’t let you borrow more than six dollars in total debt. It sounds strict, but it’s designed to ensure you aren’t stretched too thin when life happens.

For those looking to grow a portfolio, the rules are slightly more flexible. Investors generally have a DTI limit of 7. This extra wiggle room exists because rental income helps service the loan, providing a bit more security for the lender. However, even these limits aren’t set in stone. Banks have what we call “speed limits.” The Reserve Bank allows banks to allocate 20% of their new lending to borrowers who sit outside these standard ratios. If your case is strong, there’s still a chance to secure a “yes” even if the numbers are a bit tight.

Owner-occupier vs Investor limits

The gap between a DTI of 6 and 7 might seem small, but it makes a massive difference to your buying power. If you’re a first home buyer with a small deposit, you’ll likely need to stick closely to that 6x limit unless you qualify for a specific exemption. We’ve put together a quick guide to show how these limits translate into actual loan amounts based on your household income.

| Gross Annual Income | Max Loan (Owner-Occupier, DTI 6) | Max Loan (Investor, DTI 7) |

|---|---|---|

| $120,000 | $720,000 | $840,000 |

| $160,000 | $960,000 | $1,120,000 |

| $200,000 | $1,200,000 | $1,400,000 |

What counts as “Debt” in the eyes of a lender?

This is where many people get caught out. When a bank calculates your ratio, they don’t just look at the mortgage you’re asking for. They include everything. Your student loan, that car finance from last year, and even personal loans are added to the pile. One of the biggest traps is credit card limits. Even if you have a zero balance, the bank counts the entire limit as potential debt because you could spend it tomorrow. “Buy Now, Pay Later” commitments are also under the microscope now. These small weekly payments can bloat your ratio and eat into your borrowing power faster than you’d think. If you’re worried about how your current setup looks, it’s a great idea to chat with a professional who can help you tidy things up before you apply.

Exemptions and speed limits: When the rules don’t apply

It’s easy to feel a bit overwhelmed when you hear about new lending restrictions, but here is a bit of a silver lining: the debt to income ratio nz rules aren’t a brick wall for everyone. In fact, the Reserve Bank has deliberately left some doors open to ensure the housing market keeps moving and that people can still get into homes. One of the most important things to realise is that these strict RBNZ regulations primarily apply to registered banks. If you are looking at non-bank lenders or 2nd tier options, you might find a lot more flexibility than you’d get at a traditional high-street branch because they don’t always have to play by the same rigid rulebook.

Specific types of lending are also carved out of the rules to help the country grow. For example, if you are planning to build a new home, you’ll often find that the DTI limits are much more relaxed. The government wants to encourage more housing supply, so they don’t want to penalise people who are adding to the total number of houses in NZ. Similarly, if you are just looking at moving your mortgage to another bank without borrowing any extra cash, you usually won’t have to go through a fresh DTI check. Even those temporary loans to cover the gap between houses, which help you manage the time between selling one place and buying another, are treated as a special case to keep the process as smooth as possible.

First Home Loan exemptions

If you’re just starting out, there is a massive advantage available through Kāinga Ora. Loans supported under the First Home Loan scheme are officially exempt from these DTI restrictions. This is a total game-changer for young Kiwis who might have a smaller deposit or are just starting to climb the career ladder. Because these loans are designed to help people get onto the property ladder, they focus more on your potential and your ability to meet repayments rather than a rigid multiple of your current salary. For a deeper look at how to navigate your first purchase, check out our Home Loans for First Home Buyers in New Zealand: The 2026 Comprehensive Guide.

The “Speed Limit” loophole

Even for standard bank loans, there’s a bit of a safety valve known as the “speed limit.” The Reserve Bank allows banks to give 20% of their new mortgage money to people who sit outside the standard 6x or 7x limits discussed earlier. This is where having a professional in your corner really pays off. A mortgage broker knows how to present your case so you’re seen as a high-quality borrower who deserves to be part of that lucky 20%. Lenders don’t just look at the raw numbers; they look at your overall financial character, your spending habits, and your career path. If you’ve got a clean record and a solid plan, we can often help you find a way through the red tape.

How to tidy up your finances before you apply

If you’ve crunched the numbers and your debt to income ratio nz looks a bit higher than you’d like, don’t throw in the towel just yet. We see this all the time. The good news is that your current ratio isn’t a permanent mark; it is just a snapshot of where you are today. With a bit of a tidy-up and some smart moves, you can often shift those numbers into a much better position before you even sit down with a lender. It is all about presenting the cleanest possible version of your financial life to the bank.

One of the most effective ways to lower your ratio is by putting all your small, high-interest debts into one manageable payment. Those little store cards and personal loans might not seem like much on their own, but they add up quickly when a bank is looking at your profile. By combining these, you simplify your outgoings and show that you have a disciplined grip on your money. It is also worth looking at your income from a fresh perspective. Improving your ratio isn’t only about cutting what you owe; it’s also about making sure the bank sees every cent you earn. Once you’ve tidied up your debt profile, you’ll also want to think carefully about your loan structure — understanding whether a fixed rate mortgage or a floating rate suits your situation can make a significant difference to your monthly repayments and overall financial comfort.

The “Credit Card Cleanse”

Lenders don’t just care about what you’ve spent; they care about what you could spend. If you have a credit card with a $10,000 limit sitting in your drawer, the bank treats that as $10,000 of potential debt, even if you haven’t spent a cent. They have to assume you might go out and max it out tomorrow. Dropping that limit or closing the account entirely can give your borrowing power a massive boost. We usually recommend doing this at least three months before you apply. This gives the credit reporting systems plenty of time to update and ensures the bank sees a nice, clean slate when they run their checks.

Boosting your income figure

When we talk about income, we’re looking at more than just your base salary. If you’ve been consistently earning overtime, bonuses, or commissions, we can often work with the bank to include these in your total figure. For those looking to grow their portfolio, the bank will also factor in the potential rental income from the property you’re buying. You can see how these numbers stack up by using our Investment Property Mortgage Calculator NZ. Don’t forget about boarder income either. If you plan to have a flatmate in your new home, many lenders will let us add a portion of that expected rent to your total income, which can make a huge difference to your final ratio. If you’re unsure which debts to tackle first or how to best show off your income, reach out to our team for a bit of a strategy session.

How Mortgage Suite Ltd navigates the DTI maze for you

We reckon that getting a “no” from a main bank is often just the start of the conversation, not the final word. It’s easy to feel like the goalposts have moved permanently when you’re faced with the current debt to income ratio nz rules. However, our job at Mortgage Suite Ltd is to act as your dedicated negotiator, looking past the rigid spreadsheets of institutional banking to find a path that works for your unique situation. We don’t just see a ratio; we see your potential and your hard work.

With over two decades of industry experience, our founder Krish Krishna has seen every market cycle and regulatory shift imaginable. This deep institutional knowledge means we don’t just guess which lenders might say yes. We know exactly how to present your case to the right people. We take the weight off your shoulders by handling the complex discussions with lenders, ensuring your application highlights your financial strengths and addresses any debt concerns head-on. We focus on building a partnership with you, making sure you feel supported rather than just processed by a system.

Beyond the Big Four: The power of 2nd Tier lending

One of the biggest advantages of working with our team is our access to 2nd tier loans. These non-bank lenders are often more flexible because they don’t always have to follow the same RBNZ bank rules that restrict the major players. If your DTI ratio is a bit high for a traditional bank, an alternative lender might be the perfect solution. We often use these loans as a strategic “stepping stone.” They get you into your dream home or investment property now, and as your equity grows or your income increases, we can help you transition back to a traditional mortgage later. We take the time to match your unique profile to the lender that offers the best fit for your long-term goals.

Expert negotiation for complex cases

With 20 years in the game, we know which lenders are currently under their DTI speed limits and are looking for quality borrowers. This isn’t just about filling out forms; it’s about expert packaging. We know how to frame your application to mitigate concerns about existing debt while shining a light on your career trajectory and overall stability. Our goal is to take the anxiety out of the process, giving you the confidence to focus on finding the right property while we handle the red tape. When you partner with Mortgage Suite Ltd, you’re not just getting a loan; you’re getting a steady hand to guide you through a fluctuating market. We’re committed to removing the obstacles that stand between you and your dream home.

Securing your future in a changing market

The 2026 lending landscape might feel more restrictive, but it is certainly not impossible to navigate. While the debt to income ratio nz rules have changed how banks view your borrowing power, you now have a clear roadmap to move forward. By tidying up your existing debts and understanding how to maximise your gross income, you put yourself in the best possible position for a “yes”. Remember, the big banks are only one part of the story; flexibility often lies with alternative lenders who value your overall potential.

With over 20 years of banking and brokerage experience, we specialise in finding those 2nd tier and non-bank solutions that mainstream lenders might miss. We provide national coverage across all of New Zealand, ensuring that no matter where you are looking to buy, you have a steady hand to guide you. If you’re ready to take the next step without the stress of rigid spreadsheets, we’re here to help. Book a chat with our expert team today to see how we can help you beat the DTI blues. Your dream home is still within reach; you just need the right plan to get there.

Common Questions About the 2026 DTI Rules

Does the DTI ratio apply to new builds in 2026?

No, construction loans for new builds are officially exempt from the RBNZ’s DTI restrictions. This is a deliberate move by the government to encourage more housing supply across New Zealand. If you’re building from scratch or buying a home off the plans, you won’t have to worry about the standard 6x or 7x limits. This gives you significantly more flexibility when planning your project and choosing your finishes.

Will my student loan affect my debt to income ratio?

Yes, your student loan is absolutely included when the bank calculates your debt to income ratio nz. Lenders look at your total debt obligations, which includes student loans, car finance, and personal loans. Even though your repayments are automatically deducted from your pay, the total balance still sits on the “debt” side of the ledger. It’s a good idea to factor this in early when working out your borrowing power.

Can I get a mortgage if my DTI is over 6?

Yes, you can still secure a mortgage even if your ratio sits above the standard limit of 6 for owner-occupiers. Banks are allowed a “speed limit” where 20% of their new lending can go to borrowers with higher ratios. Alternatively, we can look at 2nd tier lenders who don’t have to follow these specific Reserve Bank rules. This provides a clear path forward even when a big bank’s spreadsheet says no.

Do non-bank lenders have to follow the RBNZ DTI rules?

No, the Reserve Bank’s DTI restrictions primarily apply to registered banks. Non-bank or 2nd tier lenders often have their own internal criteria and aren’t bound by the same 6x or 7x caps. This makes them an excellent option if your income doesn’t quite stretch far enough for a traditional bank’s requirements but you have a solid plan and the ability to manage your repayments comfortably.

How is rental income counted towards my DTI ratio?

Rental income is added to your total gross annual income, though banks usually “shade” it by about 20% to account for vacancies and maintenance costs. This boosted income figure is what allows investors to have a higher debt to income ratio nz limit of 7. It’s a vital part of the calculation that helps reflect the true servicing power of an investment property and your ability to grow a portfolio.

What is the difference between DTI and LVR?

While they work together, they measure two different things. LVR (Loan-to-Value Ratio) looks at the size of your deposit compared to the property’s value. DTI (Debt-to-Income) looks at your total debt compared to what you earn before tax. Think of LVR as your “entry ticket” to get the loan and DTI as the bank’s way of checking you have enough left over each month to live your life.

Can I use boarder income to improve my DTI ratio?

Yes, many lenders will let us include a portion of your expected boarder income to boost your total earnings figure. This can be a real lifesaver for first home buyers trying to stay under the 6x limit. We’ll just need to show the bank that the property has enough space and that the income is realistic for your area. It’s a simple way to make the numbers work in your favour.

What happens to my DTI if interest rates go up?

Your actual DTI ratio won’t change just because interest rates move, as it’s based on the total debt amount rather than the interest cost. However, the bank’s “test rates” usually get tougher when market rates rise. This means that while you might technically fit the DTI box, the bank will look even closer at your ability to manage higher weekly repayments. Choosing the right loan structure — for example, deciding between a fixed rate mortgage versus a floating rate — becomes especially important in this environment, as locking in a rate can provide certainty around your repayments. It’s all about ensuring you have a safe financial buffer. Keeping a close eye on what the OCR means for your mortgage rate will help you time these decisions wisely and protect your repayment budget.