What if the fee your bank calls a penalty is actually the price of admission to a much better financial future? When you’re considering breaking a fixed term mortgage nz, it’s easy to feel overwhelmed by technical talk and the fear of hidden costs. You might be watching the Reserve Bank’s July 2026 move to a 2.50% OCR and wondering if your current setup still serves your long-term goals. It’s a stressful spot to be in, especially when terms like “wholesale rates” feel like a mystery designed to keep you in the dark.

I understand that anxiety because I’ve seen how these calculations work from the inside for over two decades. This guide will help you understand those break fees so you can decide if restructuring is a smart tactical move or a costly mistake. We’ll look at the 2026 market trends, provide a clear framework for your decision, and show you how to align your home loan with your actual needs. You’ll walk away with a clear strategy that focuses on your cash flow rather than just the bank’s bottom line.

Key Takeaways

- Understand that ending your contract early isn’t just a penalty; it’s often a strategic move to secure a better rate or prepare for a property sale.

- Learn how banks use wholesale rates to calculate the cost of breaking a fixed term mortgage nz so you can avoid any nasty surprises.

- Discover a simple “yes or no” framework to help you decide if the long-term savings of a new loan outweigh the upfront break fee.

- Explore practical ways to lower your fees, such as using your annual repayment allowance to reduce your balance before you officially switch.

- See how a seasoned expert can do the heavy lifting for you, comparing different lenders to find a path that fits your unique situation.

What Does Breaking a Fixed Term Mortgage Actually Mean?

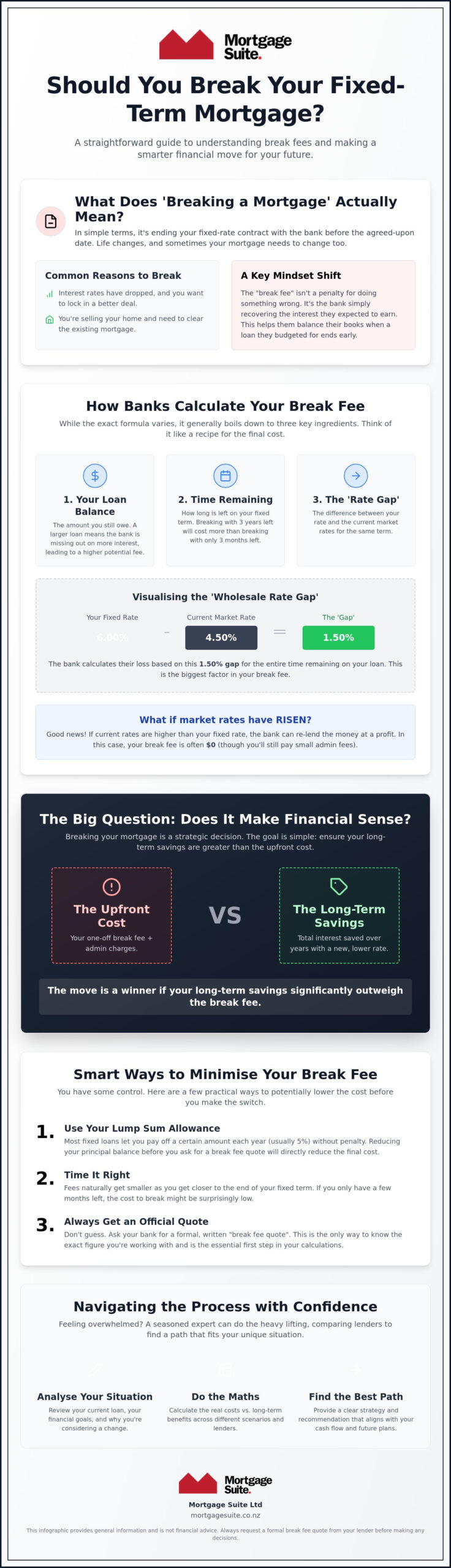

Breaking a mortgage is essentially ending your fixed-rate contract before the date you and the bank originally agreed upon. Most of us sign these deals for one, two, or even five years to get a bit of peace of mind. However, life doesn’t always stay in a straight line. You might see interest rates dropping and want to grab a better deal, or perhaps you’ve decided to sell your home and move on. When you pull the pin early, the bank charges you what is technically known as a prepayment cost or a break fee.

In the broader financial world, this is a type of early termination fee designed to protect the lender from losing out on a deal they’ve already budgeted for. Think of it this way: the break fee is simply the bank recovering the interest they expected to earn from you over the remaining life of your fixed term. It isn’t a “fine” for doing something wrong, but rather a way for the bank to balance their books when the contract they counted on suddenly disappears.

Fixed vs Floating: The Basics

Most Kiwis choose fixed rates because they provide a sense of certainty. You know exactly what your repayments will be every fortnight, which makes your family budgeting much easier. The downside is that these contracts are quite rigid. Floating rates, on the other hand, give you total freedom to pay off as much as you want whenever you like, but the rates are usually higher and can change at any time. Many homeowners find themselves feeling “stuck” in a fixed term when market rates start to fall, as they’re locked into yesterday’s higher prices while seeing better deals on the horizon.

Why Banks Charge You to Leave

It helps to understand that banks don’t just have a giant vault of cash sitting in the back room to lend out. To provide you with a mortgage, they often borrow money themselves on the wholesale market. When you decide on breaking a fixed term mortgage nz, the bank is left with that borrowed money and nowhere to put it. If current interest rates have dropped since you first signed your contract, the bank can’t lend that money to someone else for the same high return they were getting from you.

Legally, banks in New Zealand are only allowed to recover their actual losses. They aren’t supposed to use these fees to make an extra profit or punish you for leaving. They are simply trying to get back to the position they would have been in if you had stayed for the full term. Understanding this “wholesale” side of the fence is the first step in breaking a fixed term mortgage nz with confidence, as it takes the mystery out of why that final bill can sometimes look quite high.

How Banks Calculate Your Break Fee

Calculating the cost of breaking a fixed term mortgage nz often feels like trying to solve a puzzle where the bank holds all the pieces. While every lender has a slightly different formula, the total cost usually comes down to three main things: how much you owe, how much time is left on your deal, and what’s happening with interest rates in the background. It’s a bit like a see-saw; when market rates go down, your break fee typically goes up.

The scale of the fee is directly tied to your loan balance. A $800,000 mortgage will naturally attract a much higher fee than a $200,000 one because the bank’s loss is calculated on every dollar you owe. Similarly, if you have three years left on your term, you’re paying for three years of the bank’s missed interest. If you only have three months left, the fee is often small enough that it shouldn’t stop you from making a move.

The Wholesale Rate Gap

To understand the maths, you have to look at the bank’s “cost of goods.” Banks borrow money on the wholesale market to lend to you. If you locked in a rate of 6% and now market rates have dropped to 4%, the bank can’t just lend your money to someone else at that original 6%. They’ll ask you to cover that 2% gap for the rest of your term. It’s helpful to look at how mortgage rates nz are trending in 2026 to get a sense of this. Interestingly, with the Reserve Bank raising the OCR to 2.50% in July 2026, many homeowners who fixed when rates were at their lowest are finding their break fees are actually zero. This happens because the bank can now “sell” that money to a new customer at a higher rate than what you were paying.

Administrative and Discharge Fees

Don’t confuse the main break fee with the smaller administrative costs. When you leave, you’ll usually see a flat “discharge fee” to cover the legal paperwork and the bank’s time to process the exit. While the break fee can be thousands of dollars, these admin fees are usually a set amount, often around $150 to $400 depending on the lender. Always ask your bank for a formal “break fee quote” before making a final decision. These quotes are typically only valid for a couple of business days because the wholesale market moves so quickly. If you’re feeling unsure about the numbers the bank is giving you, it’s a good idea to have an expert review your quote to ensure you’re not paying more than you should.

Strategic Reasons to Break Your Fixed Rate Early

While the word “penalty” usually sounds negative, breaking a fixed term mortgage nz is often a calculated tactical move for your long-term wealth. It isn’t just about escaping a rate you’ve outgrown; it’s about positioning yourself for your next big financial step. For many homeowners, this means moving from a basic home loan into a more sophisticated structure. You might be looking to unlock equity to jump into the rental market with residential investment property loans NZ. By breaking your current deal, you can reset your finances to support a growing portfolio rather than just paying off the roof over your head.

Another common reason to pull the pin early is to improve your monthly cash flow. If you’re currently carrying high-interest debt like car loans or credit cards, folding those into a lower-interest mortgage can save you hundreds of dollars every month. Even after you account for the break fee, the total interest you pay across all your debts usually drops significantly. Of course, selling your home is the most common reason to break. In a moving market, you’ll often need to “break and re-fix” to align your new mortgage with your new property’s value and your updated budget.

Is the Maths Spot On? The Break-Even Point

Deciding to break comes down to a simple comparison. You need to look at the total interest you’ll pay if you stay versus the cost of the break fee plus the interest at the new, lower rate. We usually suggest looking at your savings over a 12-month and 24-month period. If the interest you save in the first year is more than the fee you paid to get there, you’ve reached your break-even point. There is also an “opportunity cost” to think about. If keeping your current rate prevents you from investing or clearing other expensive debt, that hidden cost might be much higher than the bank’s one-off fee.

Breaking for Flexibility

Life doesn’t always wait for your fixed term to end. Whether it’s a marriage, a new addition to the family, or a job offer in a different city, your mortgage needs to be as flexible as your life is. Sometimes, breaking a fixed term mortgage nz allows you to move a portion of your debt to a floating rate. This gives you the freedom to make large lump-sum repayments without further penalties whenever you have extra cash. It’s also the perfect time to check if a 2nd tier lender New Zealand might be a better fit. These lenders often provide more flexible terms for people whose situations don’t quite fit the rigid boxes of the major banks.

Ways to Minimise or Avoid Break Fees Altogether

Many homeowners assume that once they’ve signed on the dotted line, the break fee the bank quotes is final. However, there are several clever ways to chip away at that cost or even sidestep it entirely. When you’re considering breaking a fixed term mortgage nz, the goal is to be as tactical as possible. By understanding the small print in your contract, you can often turn a heavy financial blow into a manageable step toward a better deal.

Timing is perhaps your most powerful tool in 2026. Since the Reserve Bank raised the OCR to 2.50% in July, wholesale rates have been on the move. As we discussed earlier, if market rates are rising, the gap between your fixed rate and the current market rate shrinks. This can lead to a much lower fee, or sometimes no fee at all. Another strategy is to look for “cash-back” offers from a new lender. Many banks are currently offering thousands of dollars in cash incentives to win your business; these funds can be used to cover your exit costs from your old bank.

The 5% Rule and Partial Repayments

Most major New Zealand banks allow you to pay off a certain percentage of your loan balance every year without any penalty. This is often around 5% of your original loan amount. If you have some savings tucked away, making a lump sum payment just before you officially break the contract can significantly reduce the final fee. It’s all about timing. You need to check your “anniversary date” to see when your next allowance resets. If you’re close to that date, you might even be able to make two 5% payments in a short space of time, which makes a massive dent in the bank’s calculation.

Negotiating with Your Current Bank

It’s a common mistake to think that banks are rigid machines that never budge. In reality, they are businesses that want to keep reliable customers. While the actual break fee is usually tied to a strict formula, other costs like admin and discharge fees can sometimes be waived if you’re staying with the same bank but just restructuring. This is where having an advocate makes all the difference. We can often negotiate on your behalf to organise a better outcome and ensure the bank is exploring every option to keep your costs down. If you want to see if your current quote can be improved, reach out to us for a professional review of your mortgage strategy.

If you’re selling your home to buy another, don’t forget to ask about “porting.” This allows you to carry your current interest rate and fixed term over to your new property. It’s a fantastic way to avoid the whole “break and re-fix” process. It is especially useful if you’re already on a great rate that you don’t want to lose in the current market.

How Mortgage Suite Ltd Helps You Navigate the Break Process

When you’re faced with the prospect of breaking a fixed term mortgage nz, the paperwork and the numbers can feel like a mountain to climb. That’s where we step in to do the heavy lifting. We don’t just look at the fee the bank gives you; we calculate the real-world savings over the next few years to see if the move actually puts more money back in your pocket. Our founder, Krish Krishna, spent 20 years working within the banking system, which means Mortgage Suite Ltd knows exactly how the “big four” banks think and where they might be willing to budge.

Our approach at Mortgage Suite Ltd is built on a deep commitment to your long-term wealth. We aren’t interested in a quick, one-off transaction. Instead, we want to ensure your loan structure supports your future, whether that’s paying off your family home faster or building a property portfolio. If your current bank is making things difficult, we have the expertise to look beyond the mainstream options. We work with a range of alternative lenders who often provide a better path for people who don’t fit into a standard bank box.

Personalised Advice vs. Online Calculators

You’ve probably tried a few online calculators already. While they’re a good starting point, they are often quite blunt instruments. They don’t know about your specific tax requirements, your plans for a residential investment, or your career goals. Mortgage Suite Ltd provides a tailored plan that looks at your entire financial world. Our conversations are straightforward and conversational because we believe that complex finance shouldn’t be hidden behind confusing language. We’re here to be your steady hand and your advocate in a market that is constantly shifting.

Ready to Restructure?

Don’t let the fear of a hidden fee or the complexity of the process stop you from making a smart financial move. If your current mortgage isn’t working as hard as it should be, it’s time to take a closer look. Mortgage Suite Ltd can provide a fair dinkum assessment of your current situation and help you decide if breaking a fixed term mortgage nz is the right tactical play for you. It’s about giving you the confidence to move forward with a strategy that actually fits your life. If you’re ready to see where you stand, get in touch with Mortgage Suite Ltd for a mortgage review and let’s start the conversation.

Take Control of Your Mortgage Strategy

Deciding on breaking a fixed term mortgage nz is a significant financial choice, but it doesn’t have to be a stressful one. We’ve explored how these fees are calculated and why the 2026 market shifts might actually work in your favour. It’s important to remember that these costs are simply a calculation of interest, not a penalty for moving forward. With the right strategy, you can often transition into a loan that provides better cash flow or unlocks the equity you need for your next investment.

You don’t have to tackle the big banks on your own. With over 20 years of local banking expertise, Mortgage Suite Ltd specialises in finding paths that others might miss, particularly for 2nd tier and alternative loans. We provide national service for all New Zealanders, acting as your dedicated advocate to ensure you get a fair deal. Let’s look at your numbers together and see if we can put you in a much stronger position for the years ahead.

Ready to see what’s possible for your home loan? Talk to Mortgage Suite Ltd about breaking your fixed rate today. We’re here to help you make your next move with total confidence.

Frequently Asked Questions

How much does it cost to break a fixed-term mortgage in NZ?

The cost depends on how much you owe and how far market interest rates have dropped since you locked in your deal. Because banks are only legally allowed to recover their actual losses, the fee isn’t a fixed amount. If you have a large balance and a long time left on your term, the cost will naturally be higher than if you were just a few months away from finishing.

Can I avoid mortgage break fees if I sell my house?

You can often dodge these fees by “porting” your current loan to your new property or by timing your sale to coincide with the end of your fixed term. If you know a sale is coming up, switching to a floating rate early can also help you avoid breaking a fixed term mortgage nz penalties at the final settlement. It’s all about planning your exit strategy well before the “sold” sign goes up.

Is it worth breaking my mortgage to get a lower interest rate?

It is worth it if your total interest savings over the next year or two are greater than the upfront fee you pay to exit. You need to look at your “break-even” point to see how many months it takes for the lower rate to pay for the initial cost. If you’re planning to keep the property for a long time, even a small drop in interest can save you thousands in the long run.

How do I calculate my own mortgage break fee?

You cannot calculate the exact figure yourself because the formula relies on daily wholesale market movements that aren’t public. The only way to get a reliable number is to ask your bank for a formal “break fee quote.” These quotes are usually only valid for two or three days, so you need to be ready to make a decision quickly once the numbers land in your inbox.

What is the “wholesale rate” and why does it affect my fee?

The wholesale rate is essentially the “buy price” the bank pays for the money they lend to you. If that price has dropped since you fixed your loan, the bank stands to lose money when you leave early because they can’t lend your money out at the same high rate. The break fee is simply the way you cover that gap so the bank doesn’t take a loss on your contract.

Will a new bank pay my break fee if I switch to them?

New lenders won’t usually pay your fee directly, but they often provide a “cash-back” payment when you switch your mortgage to them. Depending on the size of your new loan, this cash payment can be enough to cover most or all of your exit costs. It’s a common way for Kiwis to move to a better deal without feeling the sting of the initial break cost.

Does a mortgage broker charge a fee to help me break my mortgage?

Most mortgage brokers are paid by the lender, so they usually won’t charge you a fee for a standard mortgage review. Their job is to act as your advocate, doing the math to see if a restructure actually makes sense for your wallet. It’s a great way to get a professional opinion on your strategy without having to pay for a consultation out of your own pocket.

Can I break my mortgage if I have a bad credit history?

Breaking your mortgage is always possible, but moving to a new bank depends on your current credit standing. If your history isn’t perfect, the mainstream banks might be hesitant to take on the loan. However, we specialise in finding paths with alternative lenders who look at the bigger picture, helping you restructure your debt even when breaking a fixed term mortgage nz feels like your only option.