What if the traditional 20% deposit isn’t the immovable barrier you’ve been led to believe? For many Kiwis, the path to home ownership feels like a maze of shifting interest rates and rigid bank policies that often seem designed to keep you out. It’s frustrating to watch your savings grow while the goalposts move, especially when you’re trying to secure home loans for first home buyers New Zealand in a market that demands both precision and persistence. We understand that the fear of being declined by a mainstream bank is real, and the confusion surrounding KiwiSaver rules only adds to the pressure.

You deserve a clear, professional roadmap that turns that uncertainty into a concrete plan. This guide provides the seasoned expertise you need to navigate the 2026 lending landscape with confidence. We’ll break down the current income caps for the First Home Loan scheme, explain the mid-2026 KiwiSaver legislation changes, and show you how alternative lenders can offer the flexibility that big banks often lack. By the end of this article, you’ll have a thorough understanding of the support schemes available and the strategic steps required to finally unlock your own front door.

Key Takeaways

- Gain a professional perspective on the 2026 property market to help alleviate anxiety and approach your purchase with seasoned confidence.

- Navigate the updated 2026 criteria for KiwiSaver withdrawals and government-backed home loans for first home buyers New Zealand to maximise your available deposit.

- Explore the benefits of 2nd tier lenders as a viable, flexible alternative to the rigid lending criteria often found at mainstream banks.

- Learn how to accurately calculate your uncommitted monthly income and organise your financial history to present the strongest possible case to lenders.

- Understand the value of having a dedicated negotiator with deep institutional knowledge to advocate for your success and remove common obstacles.

Navigating the New Zealand Property Market as a First-Home Buyer

Entering the 2026 property market requires a steady hand and a clear head. It’s perfectly natural to feel a sense of “ladder anxiety” when you see interest rates like ANZ’s 4.79% for a one-year fixed term or Kiwibank’s 4.49% for six months. While the market has shifted significantly since 2024, the fundamental challenge remains the same: finding a way in. Navigating the New Zealand Property Market involves understanding that the headlines don’t always tell the full story of your personal borrowing potential. You aren’t just a number in a spreadsheet. You’re a future homeowner who needs a partner to translate complex banking jargon into a successful application. The standard bank path is often narrow, but it isn’t the only route available to you.

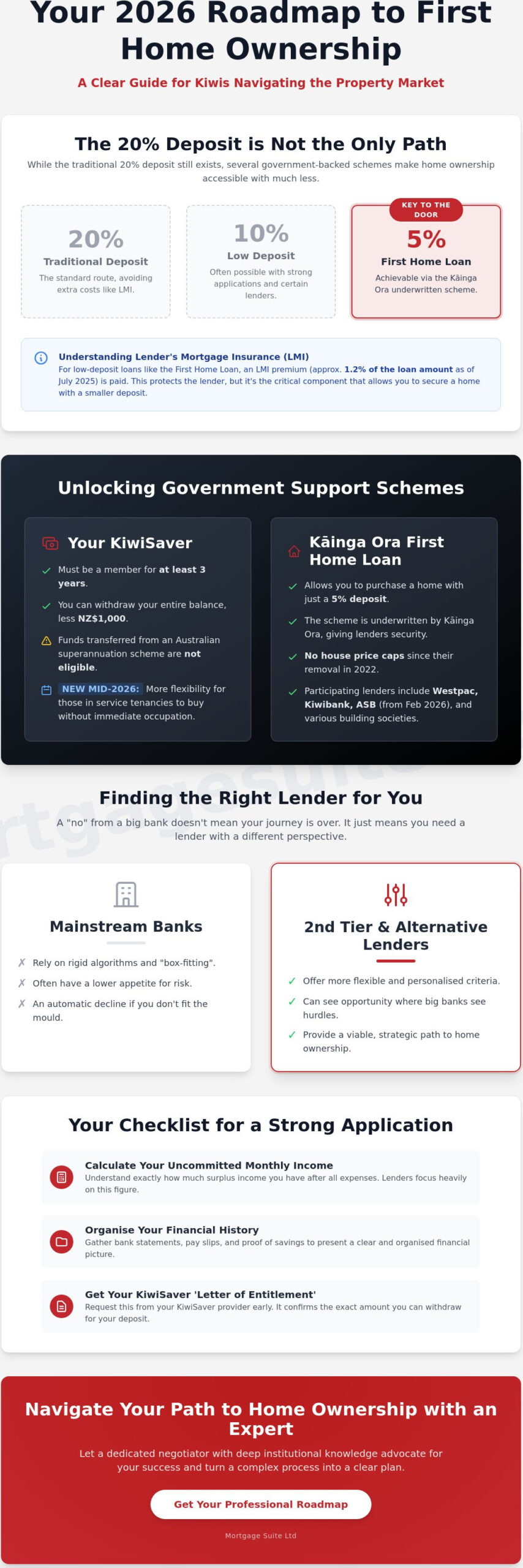

The Reality of Deposits in 2026

The old rule of a 20% deposit still exists, but it isn’t the only gatekeeper. Many buyers now aim for 10% or even 5% through specific schemes. If you’re looking at home loans for first home buyers New Zealand, you need to account for the Lender’s Mortgage Insurance (LMI). As of July 2025, the premium for the First Home Loan scheme sits at 1.2% of the loan amount. This is a cost for the lender’s security, but it’s often the key that unlocks the door when you haven’t yet built up massive equity. Equity is simply the difference between what your home is worth and what you owe the bank. Starting from scratch is hard, but it’s achievable with the right structure.

Why a “No” from a Mainstream Bank Isn’t the End

Mainstream banks rely on rigid algorithms. If your profile doesn’t fit their specific “box” for risk appetite, their system triggers an automatic decline. This doesn’t mean you’re a bad borrower. It just means that particular institution isn’t the right fit for your current financial snapshot. Different lenders have different appetites for risk. Where a big bank might see a hurdle in your deposit structure or employment history, a 2nd tier lender might see a viable opportunity. We specialise in finding these openings, acting as a bridge between the institutional “no” and your eventual “yes.” Specialised financing can often provide the necessary bridge to get you into your first home when the traditional path feels blocked.

Maximising Government Assistance: KiwiSaver and First Home Loans

While the landscape for government support shifted when the First Home Grant closed in May 2024, several powerful tools remain available to help you bridge the gap. Understanding these first home buyer assistance schemes is vital for anyone looking to secure home loans for first home buyers New Zealand. We see many clients who feel discouraged by the loss of direct grants, but the reality is that your own savings and government-backed lending criteria can still provide a significant advantage if managed correctly. It’s about knowing which levers to pull and when to pull them to ensure your application is as strong as possible.

KiwiSaver: Your Secret Weapon

Your KiwiSaver is likely your most substantial asset in this journey. To utilise it for a withdrawal, you must have been a member for at least three years. You’re permitted to withdraw almost your entire balance, provided you leave a minimum of NZ$1,000 in your account. It’s a common misconception that you can take everything; the “kickstart” or its equivalent must stay behind. Additionally, funds transferred from an Australian superannuation scheme aren’t eligible for withdrawal. Mid-2026 brings even more flexibility, with new legislation allowing those in service tenancies to buy their first home without the immediate requirement to occupy it. This is a game-changer for workers in employer-provided housing. Getting a “letter of entitlement” from your provider early in the process ensures you know exactly what you’re working with before you start making offers.

The Kāinga Ora First Home Loan Advantage

The First Home Loan scheme remains a cornerstone for those with a smaller deposit. Underwritten by Kāinga Ora, it allows eligible buyers to purchase with just a 5% deposit. While some major institutions don’t participate, the options have expanded significantly. ASB joined the programme in February 2026, joining Westpac, Kiwibank, and several building societies. This scheme is particularly effective because house price caps were removed back in 2022, meaning you aren’t restricted by the price of the property, only by your ability to service the debt. However, income caps do apply:

- Single buyers without dependents: NZ$95,000 or less (before tax) over the last 12 months.

- Single buyers with dependents: NZ$150,000 or less.

- Two or more buyers: A combined income of NZ$150,000 or less.

For those looking to build on Māori land, the Kāinga Whenua Loan provides a specific pathway that doesn’t require a traditional land mortgage, acknowledging the unique legal structures involved. Navigating these requirements can feel like a full-time job, but you don’t have to do it alone. If you’re feeling overwhelmed by the criteria, reaching out to the team at Mortgage Suite Ltd can help you determine exactly which scheme fits your financial profile.

Mainstream Banks vs. 2nd Tier Lenders: Finding Your Best Fit

In the New Zealand mortgage market, the “Big Four” often dominate the conversation. However, for many seeking home loans for first home buyers New Zealand, these institutions aren’t always the most accommodating partners. This is where 2nd tier lenders come in. These are non-bank financial institutions that provide residential loans but don’t hold a full banking license. They operate with different funding structures and, crucially, different sets of rules. While a mainstream bank might rely on a rigid “black or white” credit score, a 2nd tier lender often takes a more holistic view of your financial situation.

The core difference lies in flexibility. Mainstream banks are built for volume and speed, which means they use automated systems to filter out anything that looks slightly unusual. If you don’t fit their pre-defined box, you’re out. 2nd tier lenders are generally more human-centric. They’re willing to listen to the story behind a credit blemish or look at the potential of a property that a bank might deem too small or too unique. It’s a partnership based on individual merit rather than a cold algorithm.

When Mainstream Banks Make Sense

Mainstream banks are ideal if you have a “clean” application. This usually means a 20% deposit, stable PAYE income, and a flawless credit history. They offer the most competitive interest rates, such as ANZ’s 4.79% one-year fixed rate as of June 2026. You’ll also find enticing cash-back offers that can assist with moving costs or legal fees. If you fit their narrow criteria, the convenience of having your everyday accounts and mortgage in one place is a significant drawcard.

When to Consider a 2nd Tier Lender

If you’re self-employed with only a year of accounts, or if you’re looking at a small apartment, 2nd tier lenders are often your only path forward. They are also a lifeline for those with a minor credit blemish that triggers a “no” from mainstream institutions. While the interest rate might be higher than the 4.49% to 4.79% range currently offered by major banks, the trade-off is property ownership. We often view these loans as a strategic, short-term move. You pay a slightly higher rate for 12 to 24 months to get into the market, build equity, and then we execute a “pathway back to mainstream” strategy. Once your equity reaches the 20% threshold mentioned earlier, we can look to refinance you back to a bank for long-term savings.

Preparing Your Application: A Step-by-Step Guide to Approval

Securing a mortgage isn’t just about having the money; it’s about proving to a lender that you’re a safe bet. In the current 2026 environment, where banks are scrutinising every dollar, your preparation needs to be flawless. We often see eager buyers rush into open homes before they’ve even looked at their own bank statements through a lender’s eyes. This leads to heartbreak when a “dream home” is snatched away because the finance wasn’t ready. To avoid this, you need a methodical approach that addresses the five pillars of a successful application.

- Step 1: Organise your financial history. Lenders typically require three to six months of bank statements. They’re looking for consistent savings and “clean” spending habits.

- Step 2: Calculate your true uncommitted monthly income. This is the surplus cash you have left after all fixed expenses, tax, and living costs are deducted from your pay.

- Step 3: Understand the DTI (Debt-to-Income) ratios. By June 2026, DTI limits have become a standard tool for the Reserve Bank to manage risk. If your total debt is too high relative to your gross income, even a large deposit might not save the deal.

- Step 4: Get your “Pre-Approval” sorted. This is your license to hunt. It tells real estate agents you’re a serious buyer with the backing of a lender.

- Step 5: Engage a negotiator. Don’t just walk into your local branch. A professional negotiator presents your case to multiple lenders simultaneously to find the best fit for your goals.

The “Paperwork” Heavy Lifting

Clean spending habits for at least 90 days are non-negotiable. Banks look for red flags like excessive “Buy Now Pay Later” (BNPL) transactions or unarranged overdrafts. Even if you pay your Afterpay off on time, the total credit limit is often viewed as a potential debt by the bank’s algorithm. If you’re a contractor or business owner, the burden of proof is higher. You’ll need at least two years of certified accounts or tax summaries to prove your income is stable. Disclosing all credit card limits, even those with a zero balance, is essential because the bank calculates your borrowing power based on the limit, not what you currently owe.

Understanding Your Borrowing Power

Your borrowing power isn’t determined by the current interest rates you see advertised, such as ANZ’s 4.69% six-month special. Instead, banks use a “stress test” rate, which is often 2% to 3% higher than the market rate. This ensures you can still afford the property if rates rise in the future. Dependants also play a massive role; the bank allocates a fixed “cost per child” that reduces your uncommitted income. Remember, the cheapest rate isn’t always the best loan for your goals. A slightly higher rate with a lender who allows for a smaller deposit or offers more flexible terms might be the strategic choice that actually gets you the keys. If you’re ready to see how your profile stacks up against current criteria, the experts at Mortgage Suite Ltd can review your position before you talk to the banks.

How Mortgage Suite Negotiates Your Way into a First Home

Negotiation is the often-overlooked stage of the mortgage process. While many buyers assume their application is simply a matter of data entry, the way your financial story is presented to a lender matters immensely. Krish Krishna brings more than 20 years of seasoned banking experience to every negotiation, acting as a bridge between your personal goals and the rigid requirements of institutional lending. We don’t just process paperwork; we advocate for your success by speaking the “banker’s language” to credit managers who are looking for reasons to say no. Having an expert who knows the internal credit policies of various institutions is essential when you’re searching for home loans for first home buyers New Zealand.

This level of advocacy is particularly vital for “out of the box” clients. If you’re self-employed, have a non-standard income stream, or are working with a smaller deposit, a standard application might trigger an automatic decline. We specialise in identifying the strengths in your profile that an algorithm might miss. Our reputation for tenacity and industry knowledge allows us to secure home loans for first home buyers New Zealand even when the path seems blocked. Wherever you are in New Zealand, our national service scope ensures every Kiwi has access to high-level negotiation expertise.

A Personalised Approach to Lending

We’ve moved away from the cold, transactional nature of modern banking to a relationship-based model. Every application we handle is structured to highlight your specific financial strengths. This might involve explaining a temporary dip in income or detailing the growth potential of your business. The Mortgage Suite Ltd difference is built on a foundation of reliability and trust; we treat your first home purchase with the same priority and passion as if it were our own. We understand that this isn’t just a loan; it’s the foundation of your future.

Your Long-Term Property Partner

Our commitment to you doesn’t end when you get the keys to your first home. We view ourselves as your long-term property partner. As your equity grows and market conditions shift, we provide ongoing support to help you manage interest rate changes or plan for your first residential investment property. We’re here to ensure your mortgage remains a tool for wealth creation rather than just a monthly expense. If you’re ready to move beyond automated calculators and experience a professional, hands-on approach, Speak with Krish and the team about your first home today and let us start the negotiation for you.

Taking the First Step Toward Your New Front Door

Owning your first home in 2026 is an achievable reality when you have the right strategy and a seasoned advocate in your corner. We’ve explored how to leverage KiwiSaver, navigate updated income caps, and use 2nd tier lenders as a vital bridge to property ownership. Success in this market isn’t just about finding the lowest interest rate; it’s about professional preparation and expert negotiation that speaks the language of the banks. By organising your financial history and understanding your true borrowing power, you position yourself as a priority candidate for lenders.

With over two decades of banking and negotiation experience, our team specialises in finding solutions for “out of the box” profiles and navigating the complex world of non-bank lending. We provide a dedicated, national service that supports Kiwis across all of New Zealand, ensuring you’re never just a number in a system. If you’re ready to move past the automated calculators and secure a partnership built on trust and results, it’s time to act. Secure your first home loan with Mortgage Suite and let us help you find the right home loans for first home buyers New Zealand. Your journey to home ownership starts with a single, confident conversation.

Frequently Asked Questions

How much deposit do I really need for a first home in New Zealand in 2026?

You need as little as a 5% deposit if you qualify for the First Home Loan scheme underwritten by Kāinga Ora. While mainstream banks typically prefer a 20% deposit to avoid low equity margins, many buyers successfully enter the market with 10% by using a 2nd tier lender. If you have less than 20%, you should account for the Lender’s Mortgage Insurance (LMI) premium, which currently sits at 1.2% for government-backed loans.

Can I use my KiwiSaver for a deposit if I have owned a home before?

Yes, you can potentially use your KiwiSaver as a “previous home owner” if Kāinga Ora determines you are in a similar financial position to a first-home buyer. You must still meet the standard withdrawal criteria, such as being a member for at least three years and leaving a minimum balance of NZ$1,000 in your account. This is a vital pathway for those looking to re-enter the market after a significant life change or financial setback.

What is the difference between a bank and a 2nd tier lender?

A mainstream bank is a large institution with rigid, automated criteria, whereas a 2nd tier lender is a non-bank provider that often offers more human-centric flexibility. 2nd tier lenders are a strategic choice for self-employed Kiwis or those with “non-standard” income who don’t fit the narrow algorithms of the major banks. They provide an essential alternative when securing home loans for first home buyers New Zealand in a tight credit environment.

How does the First Home Grant work and am I eligible?

The First Home Grant is no longer available as the government closed the scheme to new applicants in May 2024. Instead, you should focus on the First Home Loan scheme, which still provides a pathway to ownership with a 5% deposit for eligible buyers. We recommend focusing on your KiwiSaver withdrawal and exploring alternative lending structures to bridge any remaining gap in your deposit requirements.

What happens if the bank declines my home loan application?

A decline from a mainstream bank is simply a sign that your profile didn’t fit their specific risk “box,” not the end of your home-owning dreams. We often review these declined applications and find solutions through 2nd tier lenders who take a more holistic view of your financial situation. It’s about finding a lender whose appetite for risk matches your current profile and restructuring your debt to meet modern DTI requirements.

Is it better to have a fixed or floating interest rate as a first-home buyer?

Most first-home buyers opt for a fixed rate to gain certainty over their repayments, especially with 2026 rates like ANZ’s 4.79% for a one-year term. Floating rates are currently higher, often around 5.79%, but they offer the flexibility to make unlimited extra repayments without penalty. Many of our clients choose a “split” mortgage, fixing the bulk of the loan for stability while keeping a small portion floating to pay down faster.

Do I need to pay for the services of a lending expert?

In the majority of standard residential applications, the lender pays a commission to the expert for presenting a high-quality application, meaning there is no direct cost to you. If your situation is particularly complex or requires a specialised 2nd tier lending structure that involves a fee, this will always be discussed with total transparency upfront. Our goal is to act as your advocate and ensure the process is as cost-effective as possible.

How long does the pre-approval process usually take in NZ?

A standard pre-approval usually takes between three to five working days once your full documentation is submitted to the lender. This timeframe can stretch slightly longer for complex applications involving self-employment or 2nd tier lenders that require manual assessment by a credit manager. Having your financial history and income proof organised before you start the process is the most effective way to secure home loans for first home buyers New Zealand quickly.